Publication - Research and analysis

Scottish economic bulletin: March 2024

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Consumer Activity

Consumer sentiment improved in January but remains negative overall.

Consumer Sentiment

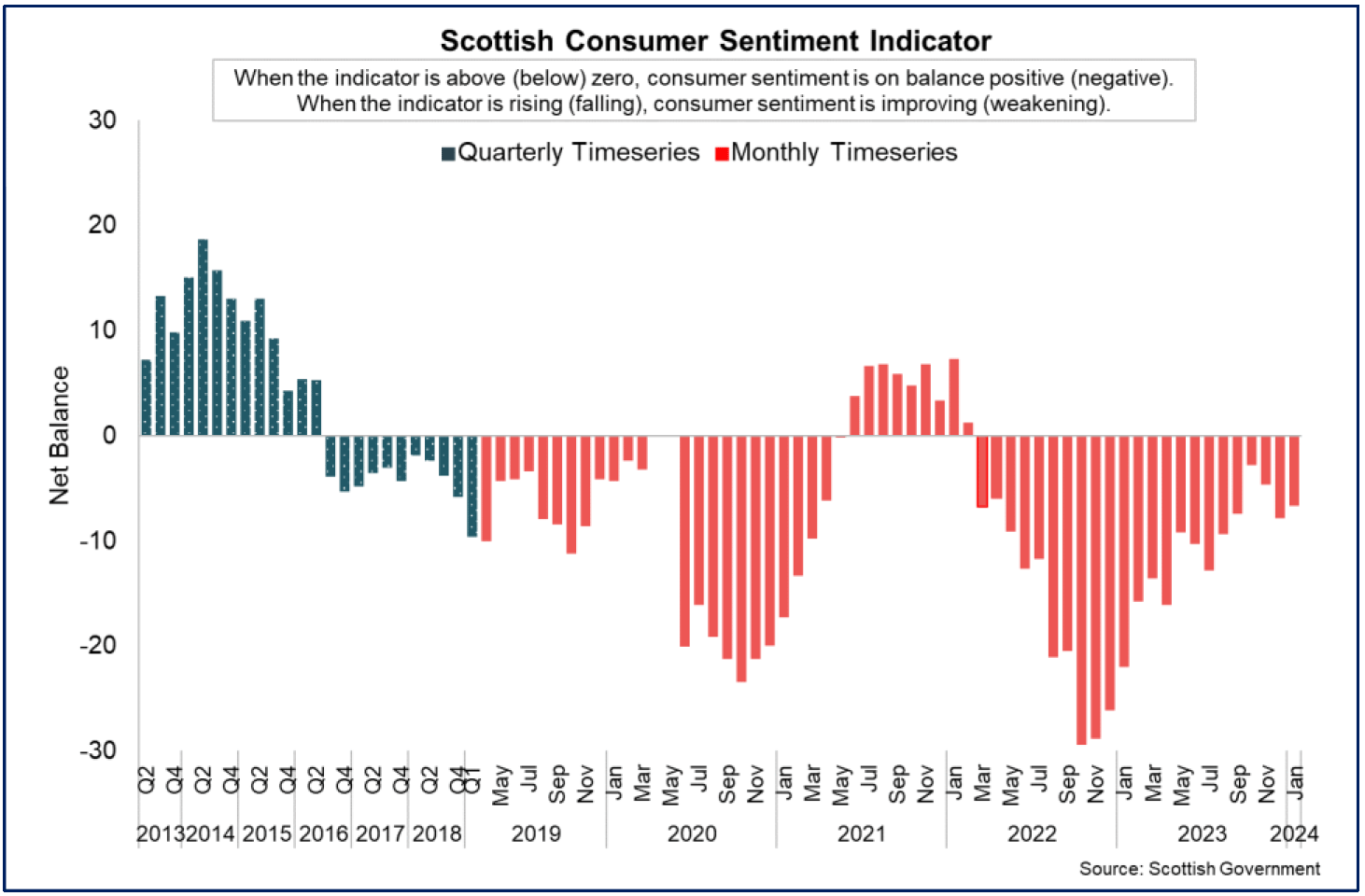

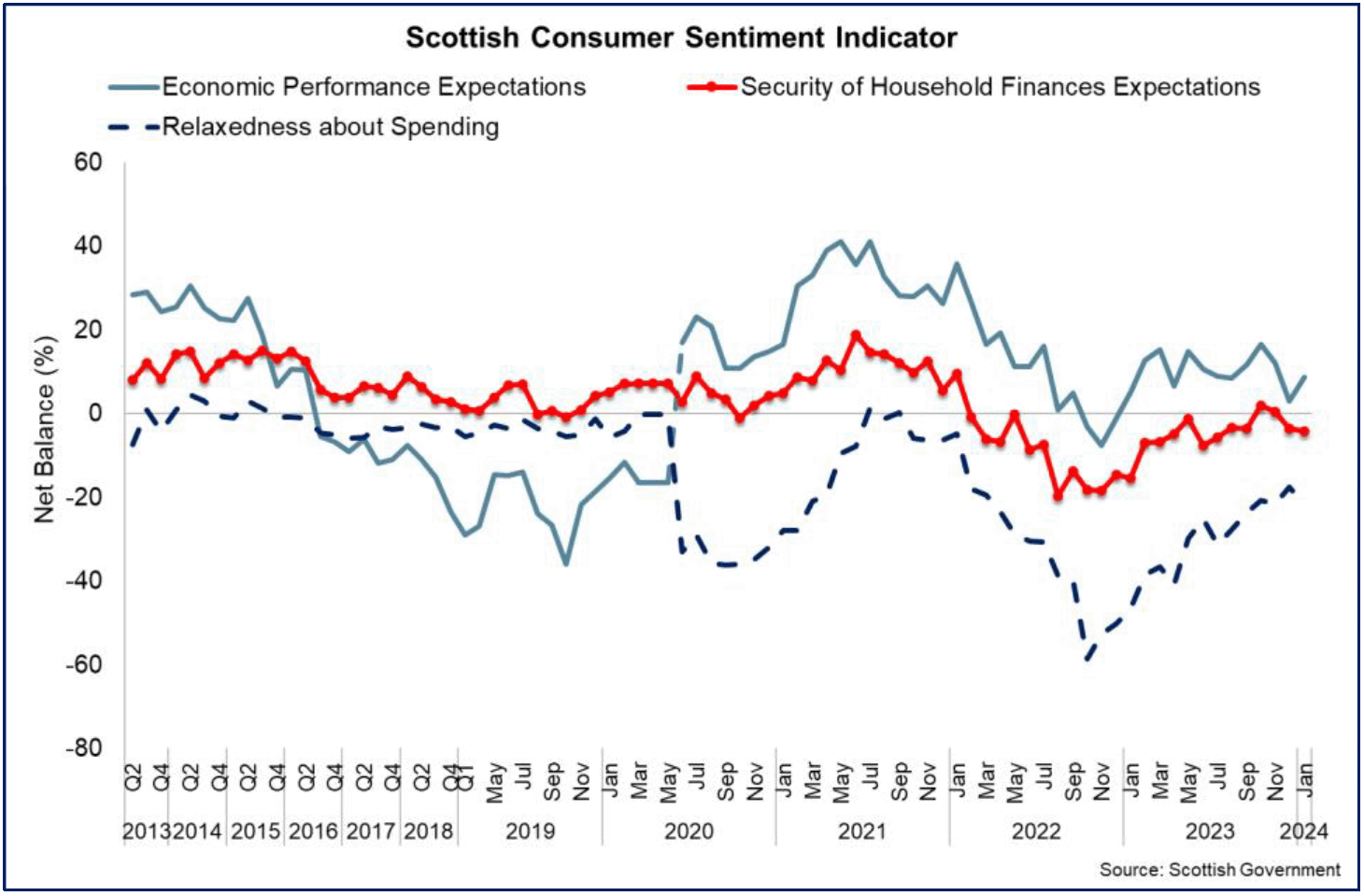

- The Scottish Consumer Sentiment Indicator reflects how households think the economy is performing, how secure they feel about their household finances and how relaxed they feel about spending money.

- Consumer sentiment fell sharply during 2022 to -29.4 as inflationary pressures increased and the economic outlook weakened. However sentiment strengthened significantly over 2023 as inflationary pressures reduced and latest data for January show sentiment increased by 1.2 points over the month and by 15.3 points over the year to -6.7.[17]

- While all the sentiment sub-indicators have strengthened over the past year, households continue to report on balance that the economy is performing less well than last year (-6.8) and their personal financial secuity is weaker (-9.4). Looking ahead to the coming year, households expect the economy to improve (8.8) however continue to expect their personal financial security to weaken (-4.2).

- This is reflected in the spend indicator which remains significantly negative (-21.6) and reflects that households are not currently relaxed about spending money.

Cost of Living and Spending

- The rate of inflation has reduced significantly over the past year, however the sharp rise in cost of living and higher interest rates continues to impact household decisions on spending (essential and non-essential), saving, and borrowing (including financing outstanding borrowing).

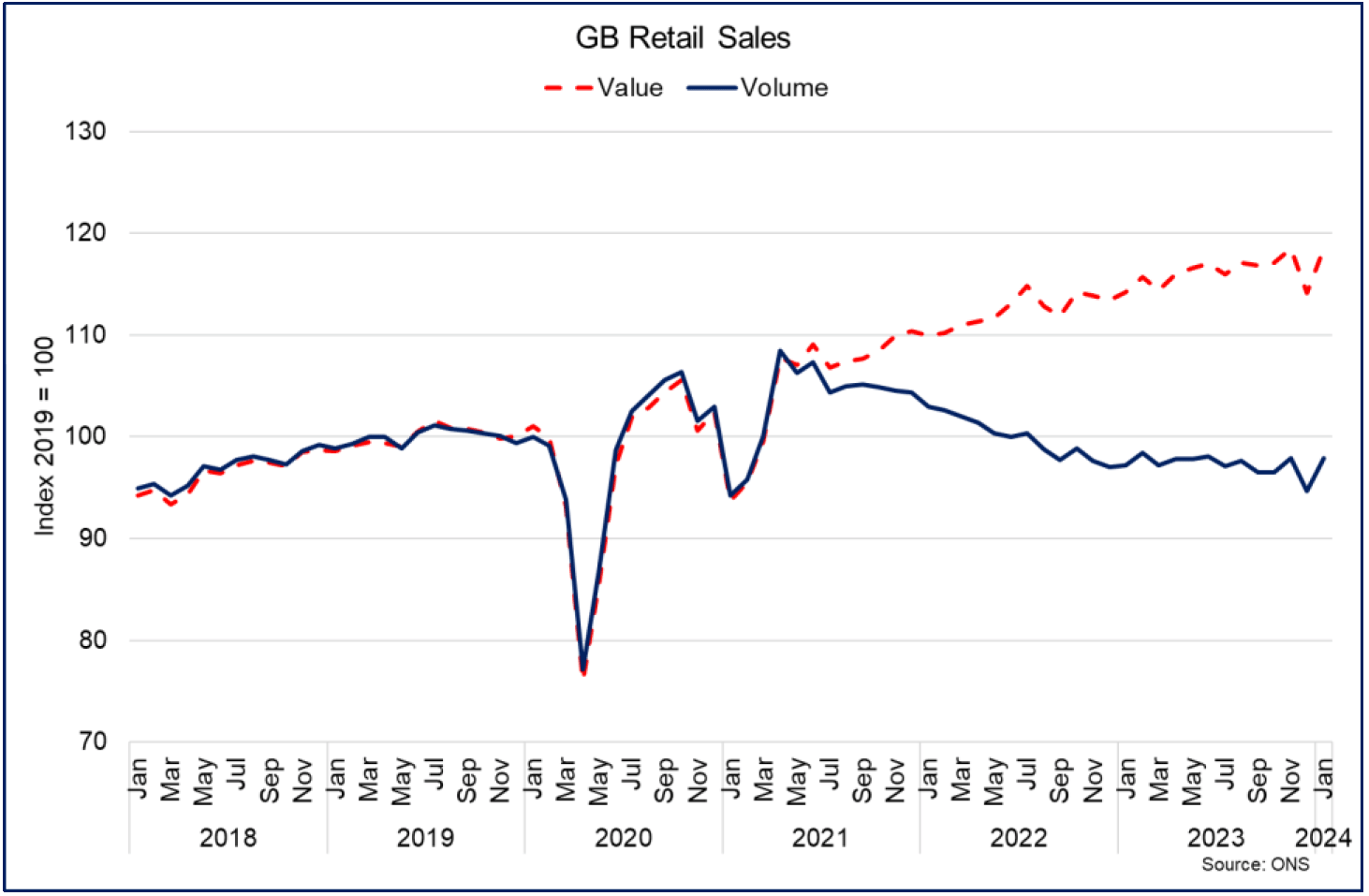

- For example, retail sales volumes in Great Britain have settled below their 2019 level over the past year and rose 0.7% over the year to January while sales value grew 3.8% with the divergence reflecting the pace of rising prices.[18]

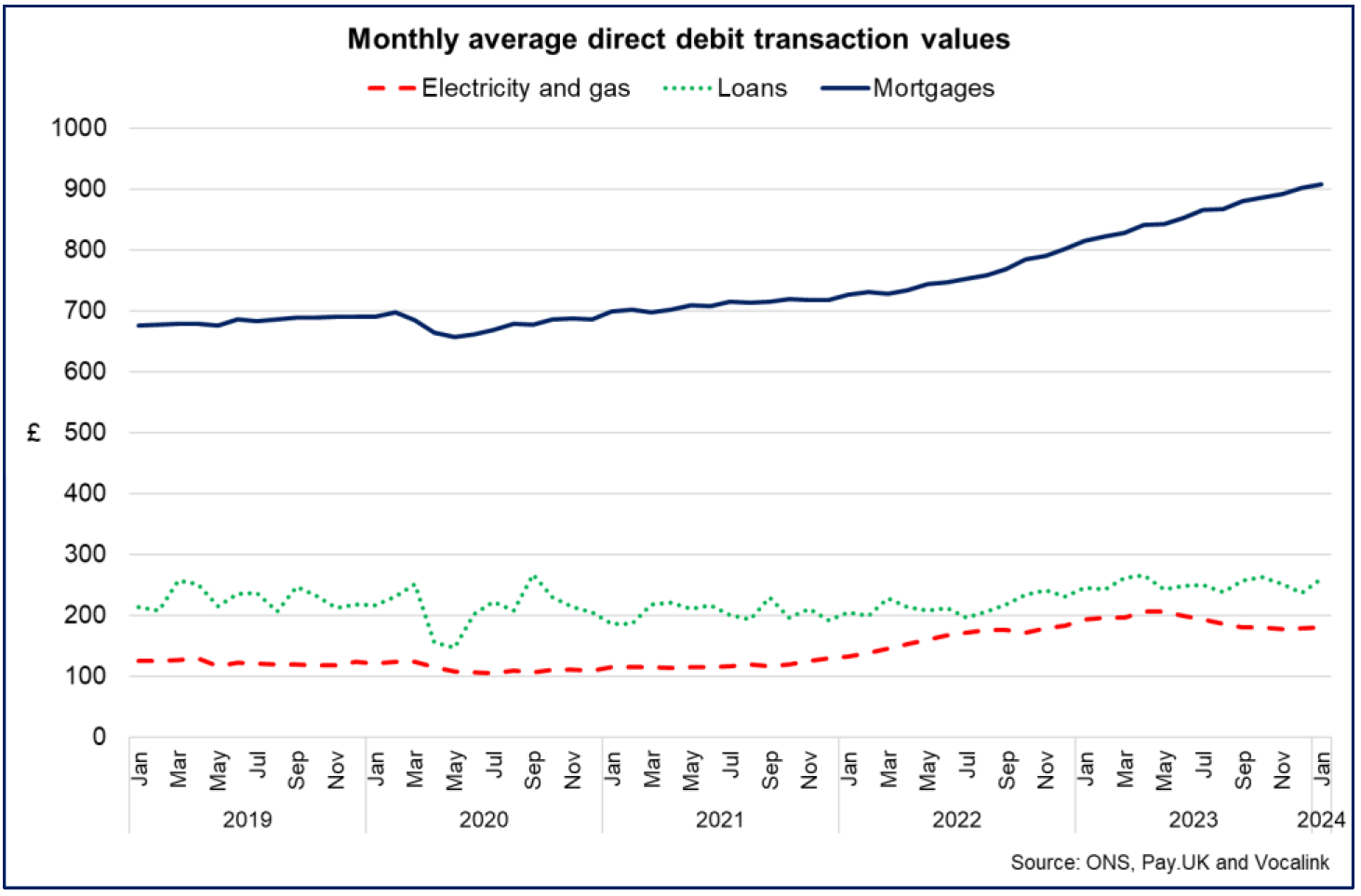

- Similarly the change in prices and interest rates have had a significant impact on the amount UK conumers are paying for their energy costs, mortgages and other loans. In January the average monthly direct debit payment for electricity and gas was £180.05, down 7.3% compared to January 2023 however was up 35.4% compared to January 2022. This in part reflects that the Energy Price Cap has fallen over the past year, however remains significantly higher compared to two years ago.[19]

- However, the average monthly direct debit payment for mortgages was £907.70 in January (up 11.3% over the year and 24.8% since the start of 2022) and £260.30 for loans (up 6.1% over the year and 27% since 2022). Ths in part reflects that higher interest rates are continuing to progressively feed through to higher borrowing costs.

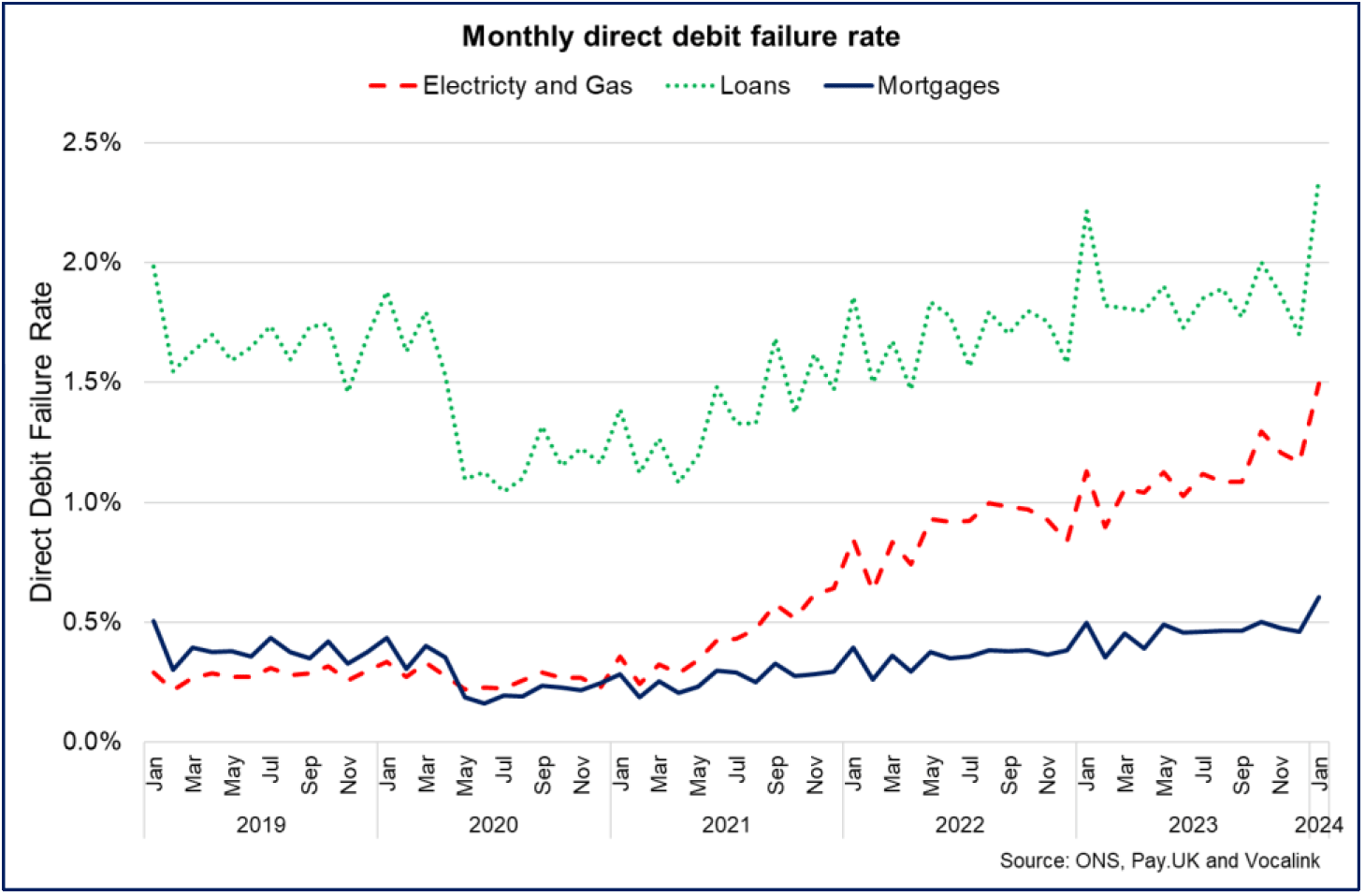

- The sharp increase in prices has been accompanied by an increase in the direct debit failure rate (the percentage of transactions that fail due to insufficient funds), reflecting the challenges facing some household budgets. For electricity and gas payments, the payment failure rate has risen to 1.5% (up from 1.13% in January 2023), while for mortgages it has risen to 0.61% (up from 0.5% in January 2023).

- More broadly in February, the ONS Public Opinions and Social Trends survey showed that 41% of respondents were finding it very or somewhat difficult affording energy bill payments and 39% for mortgage and rent payments. For energy bills, this was slightly lower than at the same point in 2023 (48%), however has risen for mortgages payments from 33%.[20]

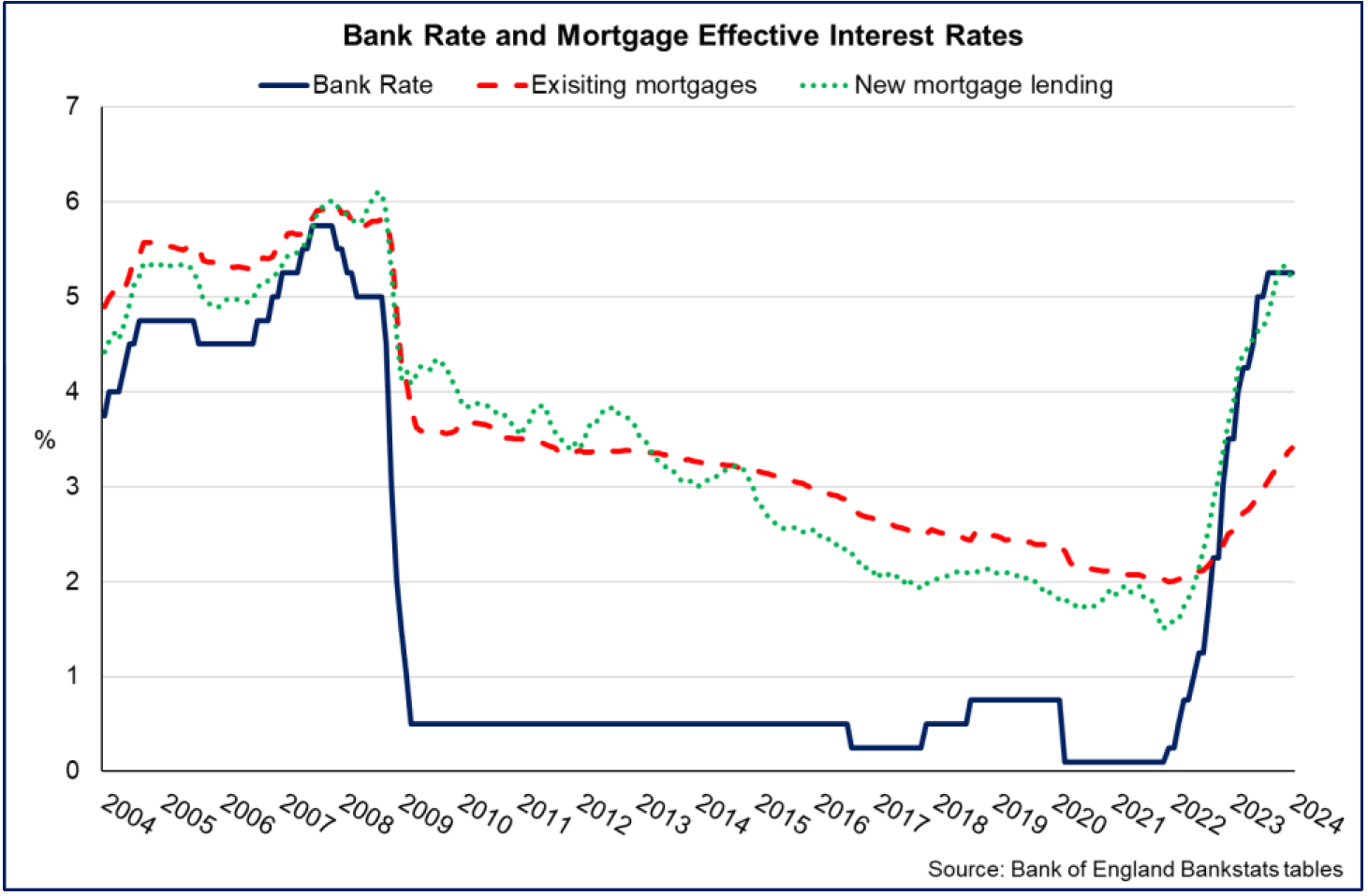

- The more gradual impacts of higher interest rates on mortgage payment challenges compared to energy payments reflects the sharp rise in the Bank Rate between the end of 2021 and middle of 2023 and the time it takes for the full impact of the increases to be felt at an aggregate level due to the high share of mortgages that are on a fixed rate.

- Reflecting this, the ‘effective’ interest rate – the actual interest paid – on newly drawn mortgages remains elevated but fell for a second consecutive month in January to 5.19%, in part reflecting increased market expectations that interest rates may have peaked. Rates on the outstanding stock of mortgages however continued to rise to 3.41%.[21]

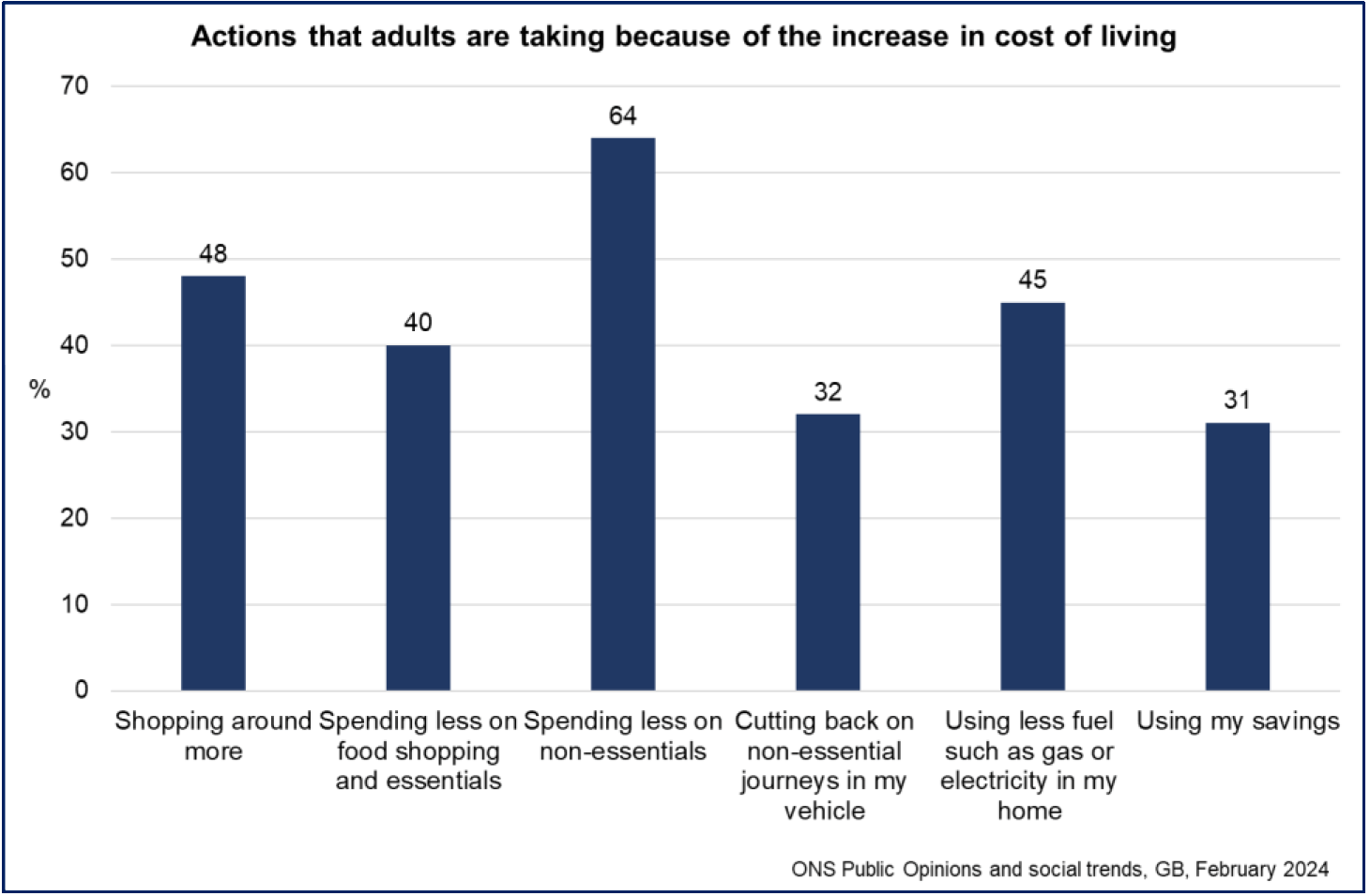

- In response to the change in cost pressures facing households, ONS Public Opinions and Social Trends survey data from February show that the most common actions people are taking in response to the increased cost of living were spending less on non-essentials (64%) and shopping around more (48%). 45% reported using less fuel such as gas or electricity in their home and 40% reported spending less on food shopping and essentials.

Contact

Email: OCEABusiness@gov.scot