Publication - Research and analysis

Scottish economic bulletin: February 2024

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Conditions

Business activity further weakened in December however optimism remains resilient.

Business Activity

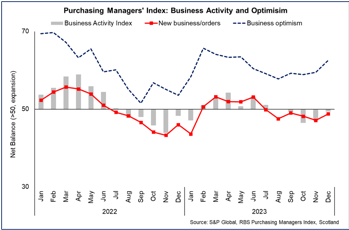

- The Purchasing Managers Index (PMI) business survey indicates that business activity in Scotland’s private sector fell in December and across the fourth quarter of the year.[5]

- The business activity indicator was 49.4 in December, slightly improved from November however was the fourth consecutive month indicating falling activity with a sharp fall in the manufacturing sector (45.2), partly offset by marginal growth in services (50.4).

- A key driver of weaker business activity has been subdued new business orders, which have fallen continuously since July and most notably in the manufacturing sector in recent months.

- Despite the current weakness in business activity and demand, business optimism for the year ahead improved over the second half of 2023 and in December was at its highest level since earlier in the year in May. Business optimism stemmed from a combination of expected improvements in trading conditions alongside an increase in marketing and sales activity.

Business Concerns

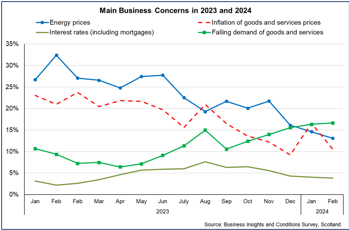

- The factors weighing on demand continue to reflect the broader concerns that businesses are currently reporting on business conditions. The main business concern reported in the Business Insights and Conditions survey (BICS) for February is falling demand of goods and services (16.6%). This has been a rising concern reported by businesses since the middle of 2023.[6]

- Businesses continue to have concerns about energy prices (13.1%) and wider inflation of goods and services (10.5%) however these has been on a downward trend over the past year and likely reflect adjustments businesses have made in response to the changes in costs, the general easing of inflationary pressures and expectations of further reductions over the coming year.

- Concerns regarding interest rates have also eased over the second half of 2023 and start of 2024 and also likely reflect increased expectations that interest rates have peaked and may start to fall over the coming year.

- The Scottish Chambers of Commerce (SCC) Quarterly Economic Indicator shows a similar pattern with concerns about inflation (52%) and interest rates (40%) easing in the final quarter of 2023 albeit remaining higher than prior to the inflation shock.[7]

Business Costs

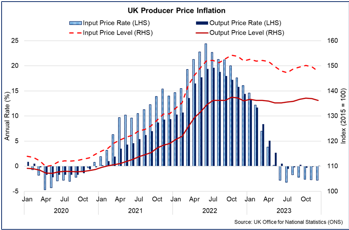

- At a headline level, producer input price inflation continued to decline with input prices falling on an annual basis for a seventh consecutive month and by 2.8% in December.[8] The change in input prices has also been reflected in producer output prices which grew by 0.1% annually.

- Overall, input and output price levels have been relatively stable since June 2023, and remain substantially higher than their 2021 levels. The moderation of energy price inflation has been a key driver of falling producer price inflation with crude oil input costs falling 10.2% over the past year, however imported food material costs rose 10.4% over the year.

- Looking across a broader range of input costs the PMI business survey indicates that business input costs continued to rise in December, with businesses indicating that labour, shipping and fuel costs were creating upward pressure though at one of the slowest rates since the start of 2021.

- The SCC Quarterly Economic Indicator also shows that while cost pressures are easing, the source of these for businesses remains broad based with 60% reporting increased cost pressures from labour costs, 57% from energy costs, 45% from raw materials and 37% from fuel costs.

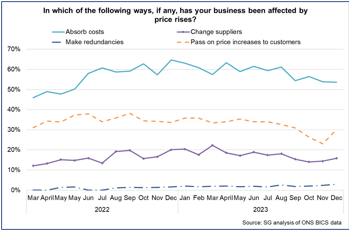

- BICS data for Scotland provide latest insights into the changing effects on businesses of price rises. At the start of December, 53.7% of businesses reported that they had to absorb costs, 30.2% reported having to pass on price increases to customers and 15.8% had to change suppliers. A much lower percentage of firms reported having to make redundancies (3%).

- The slight downward trend in the share of businesses reporting to be absorbing costs potentially reflects the slowing pace of input cost rises and similarly, while the share of businesses passing on price increases to customers rose in December, it remains slightly down compared to December 2022. The SCC Quarterly Economic Indicator also reported a declining share of businesses planning to raise prices (40% in Q4 2023, down from 48% in Q3 2023).

Business Investment

- The combination of business concerns around weakening demand, inflationary pressures and higher interest rates continues to weigh on business investment decision making.

- The SCC Quarterly Economic Indicator for Q4 2023 reported that while on balance firms continue to increase rather than reduce investment, over half of firms continued to report no changes to both total (55%) and training (54%) investment. At a sector level the balance of firms reported a return to investment growth in the construction sector, further positive growth in the manufacturing sector and a return to investment growth in retail and wholesale for the first time since the start of 2020. Elsewhere in the services sector the majority of investment remained positive on balance in the financial and business services sectors, however capital investment contracted for the first time in a year.

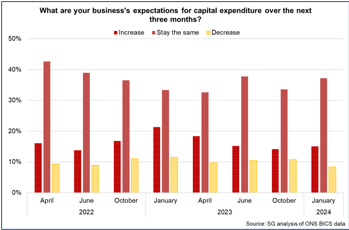

- BICS data for Scotland in January show 15% of respondents thought their capital expenditure would increase over the next three months, lower than at the start of 2023, while 8.4% of respondents continue to expect to decrease capital expenditure over the coming year. Overall compared to the start of 2023, there has been an increasing share of businesses reporting that capital expenditure will stay the same.

Business Optimism

- PMI business survey data indicates that business optimism improved over the second half of 2023, rising to a seven-month high in December however remains lower than at the start of last year. This optimism for improving demand is partly reflected in the PMI data indicating that firms have continued to add to their staffing numbers by filling vacant positions and replacing leavers.

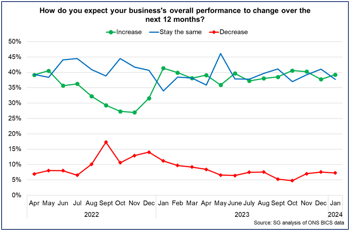

- BICS data for Scotland indicates that at the start of 2024, most businesses expect their overall business performance to increase (39.3%) or stay the same (37.7%) over the coming year. On aggregate, this has slightly improved compared to the start of 2023, while the share of businesses expecting their performance to decrease has fallen slightly to 7.3%.

Contact

Email: OCEABusiness@gov.scot