Scottish Aggregates Tax: proposed approaches to cross-border taxation

This consultation seeks views on how to approach cross-border taxation for Scottish Aggregates Tax (SAT). This will enable the Scottish Government to gain feedback to inform policy development in advance of the planned introduction date of SAT on 1 April 2026.

Closed

This consultation closed 18 August 2025.

View this consultation on consult.gov.scot, including responses once published.

Consultation analysis

2. Cross-border movement of aggregate

Background

2.1 As a result of devolving UKAL to Scotland, there will be two aggregates tax jurisdictions where there was previously one. This has implications in terms of the treatment of aggregate that moves across the border between Scotland and the rUK.

2.2 The 2024 Act sets out that SAT commercial exploitation is triggered in four separate circumstances when the aggregate is:

- removed from its originating site, moved from a connected site, or moved from a site where an excepted process was supposed to be applied but it has not;

- where there is agreement to supply;

- where it is used for construction purposes; or

- mixed with another substance other than water.

2.3 This consultation paper has also been shaped by the policy decisions previously set out in the Scotland Act 2016 and the 2024 Act. This includes the following key policy decisions:

2.3.1 The country of destination - rather than the country of origin - will retain the tax on intra-UK aggregate trade. This method is designed to reduce the risk of market distortion within the aggregates sector.

2.3.2 By allocating tax revenue to the destination country, the policy helps minimise commercial issues i.e. if the country of destination retained the tax then there could be potential for purchasers of aggregate to exploit differences in tax rates between jurisdictions. This approach will ensure that within each ‘geographical market’ - whether Scotland or the rUK - the same destination country tax applies regardless of where the aggregate was originally extracted.

2.3.3 Aggregate imported into Scotland from outside the UK will be subject to tax at the first point of commercial exploitation following its arrival. In most cases, the person responsible for this commercial exploitation in Scotland will be expected to account for the tax.

2.3.4 For aggregate transported to Scotland from rUK, the Scottish Government proposes that the producer - rather than individual customers - should account for the SAT, mirroring the process used for transactions occurring entirely within Scotland. This approach is intended to minimise administrative complexity and reduce the burden on businesses.

2.3.5 The tax will be applied as far up the supply chain as possible (e.g. aggregate producers rather than customers accounting for the tax when aggregate is moved to Scotland from the rUK). This approach was informed by stakeholder feedback.

2.3.6 Ensuring that the tax will be triggered where aggregate is first moved/ commercially exploited in the UK.

2.4 The Scottish Government, Revenue Scotland and HMRC are working closely to consider the approaches to cross-border taxation. This work has included joint engagement with various aggregate industry businesses and stakeholders to inform this consultation. There is a joint aim to develop cross-border tax options that:

- avoid double taxation of aggregate;

- minimise the risk of market distortion (should the respective tax rates vary);

- minimise the risk of tax avoidance or evasion;

- enable Revenue Scotland and HMRC to assure compliance; and

- are workable and proportionate for business.

2.5 Policy for SAT and UKAL will be the responsibility of the Scottish Government and UK Government respectively. This means that there is potential for policy divergence in the future, depending on decisions which respective Governments make on the taxes.

2.6 When SAT is operational, where cross-border activity results in aggregate being commercially exploited in both Scotland and rUK, then both SAT and UKAL would be due. However, to avoid double taxation, the proposed approach will be that only one tax is applied (the destination country), and that a tax credit is provided for the other tax.

2.7 As set out in point 2.3.1, the tax will ultimately be due in the destination country, whatever the origin of the commercially exploited aggregate.

2.8 Where appropriate, this consultation proposes to continue with that approach as it will minimise overall administrative burden on business, retain the tax point with existing UKAL taxpayers and have a less distortive impact on the aggregates sector.

Scale of cross-border movement

2.9 The available evidence suggests that small amounts of aggregate are moved to Scotland, with a 2019 Aggregate Minerals Survey for Scotland[4] suggesting around 80,000 tonnes. In comparison, the total sales of primary aggregate produced in Scotland in 2019 was 20.78 million tonnes. The Scottish Government has jointly commissioned, with the UK and Welsh Governments, the British Geological Survey to conduct a new aggregates survey, based on 2023 outputs. The survey findings are expected to be published in mid-2025 by the Ministry of Housing, Communities and Local Government (MHCLG).

2.10 At the 2025-26 UKAL rate of £2.08 per tonne[5] this would represent £166,400 of tax revenue. For context, the Scottish Fiscal Commission’s indicative forecast for the Scottish share of UKAL revenues in 2026-27 is £62 million. Furthermore, we believe that collection and middlemen transactions will only account for a proportion of the overall tonnage and revenue of aggregate moved across the border.

Questions

1. Can you provide any evidence on the scale of:

- Direct supplies (where aggregate is transported by the quarry on behalf of a middleman);

- Direct supplies (where aggregate is collected); and/or

- Indirect supplies (middlemen transactions)?

Cross-border scenarios requiring further consideration

2.11 Ongoing engagement with industry representatives has identified several cross-border scenarios that require more detailed consideration and stakeholder engagement. This consultation considers the following cross-border transactions:

- Direct supplies (i.e. aggregate supplied from a rUK quarry to a Scottish based customer and where a customer based in Scotland directly collects aggregate from a rUK quarry, for use in Scotland).

- Indirect supplies (i.e. where a rUK quarry supplies aggregate to a rUK middleman, who then supplies the aggregate to a Scottish customer).

- Other complex scenarios.

2.12 For the purpose of this consultation, the commentary on these scenarios below assumes that the rate of SAT and UKAL are the same. This does not, however, indicate a policy decision by the Scottish or UK Government. These scenarios will be most relevant to quarries and middlemen located near the border, but any aggregates producer undertaking cross-border activity could be affected.

2.13 This consultation focuses on the movement of aggregate that results in aggregate being subject to SAT (supplies from rUK to Scotland) and not UKAL (supplies from Scotland to rUK), which is the responsibility of the UK Government. Although policy for SAT and UKAL will be responsibility of the Scottish Government and UK Government respectively, both Governments will continue to work collaboratively to explore complementary approaches to cross-border taxation.

Direct supply

Introduction

2.14 A direct supply involves the supply of aggregate from a rUK quarry directly to a Scottish based customer.

2.15 The Scottish Government’s overall policy intention is that the country of destination retains the tax (see point 2.3.1). Therefore, for supplies of aggregate from rUK to Scotland, it would be SAT that would be ultimately paid on the material in this situation. The SAT legislation was developed in this manner, as tax rates for SAT and UKAL will be set by the respective governments and there is potential for the tax rates to be different. By having the country of destination retain the tax, this minimises the risk of commercial issues, i.e. there could be potential for businesses to “rate shop” if different rates applied depending on the country of origin of the material. This approach will ensure that within each ‘geographical market’ - whether Scotland or the rUK - the same destination country tax applies, regardless of where the aggregate was originally extracted.

2.16 In a direct supply scenario, the rUK quarry will become liable to account for UKAL when they supply the aggregate to the Scottish customer. The rUK quarry would also have to register for and pay SAT. However, as the aggregate has moved from rUK to Scotland, the quarry could then claim a tax credit for UKAL from HMRC. The ability to claim tax credits (either from Revenue Scotland or HMRC as appropriate) for aggregate which is moved across the border aims to prevent double taxation.

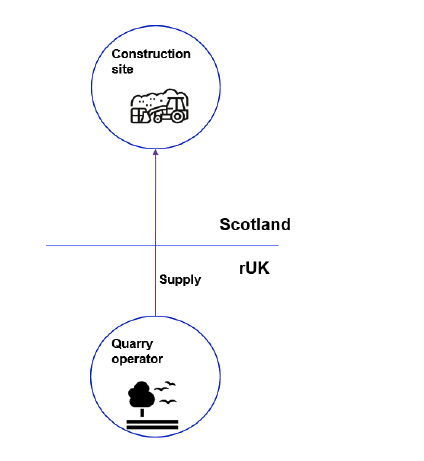

2.17 The most common form of direct supply is where a rUK quarry operator supplies and delivers aggregate to a Scottish based customer. An example of this type of direct supply can be seen in Diagram 1.

rUKquarry operator's tax position

- rUK quarry to register and account for UKAL (commercial exploitation when supply to Scottish customer made from rUK quarry). However, rUK quarry can claim UKAL tax credit (as same supply of aggregate moved from rUK to Scotland

- rUK quarry to register & pay SAT (commercial exploitation as aggregate has been supplied to Scottish quarry from rUK)

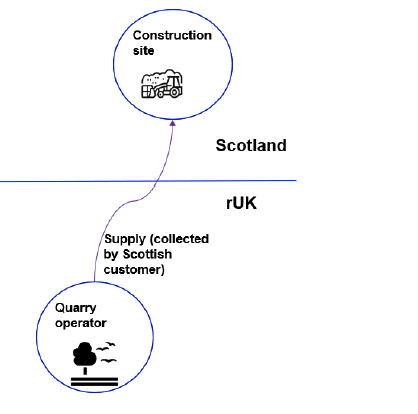

Collection scenario - where a customer based in Scotland directly collects aggregate from a rUK quarry, for use in Scotland

2.18 Engagement with industry stakeholders has identified a cross-border scenario where a Scottish customer collects aggregate from a rUK quarry and then brings that aggregate to Scotland themselves. This is another type of direct supply. See Diagram 2.

2.19 For example, there could be a quarry site based in rUK near the border and a Scottish based construction firm may travel to the quarry site to collect aggregate which they then take back to Scotland for use on a construction project. In this scenario, there is the potential for double taxation.

2.20 Where a Scottish based customer collects aggregate from a rUK quarry, the rUK quarry would register and pay UKAL, as they have commercially exploited aggregate in rUK (when supplying to the customer collecting). However, the rUK quarry would also be liable to account for SAT (as the aggregate has been transported into Scotland), as per section 8(2) of the 2024 Act[6].

2.21 As informed by stakeholder feedback during the development of SAT primary legislation, the tax will be applied as far up the supply chain as possible with aggregate producers (the quarry) accounting for the tax rather than the customers (see point 2.3.5). However, to enable quarries to identify collections that cross the border into Scotland and account for SAT due, a new process is required. This process would require aggregate suppliers to ask customers for a declaration that the material is going to Scotland. Customer declarations are currently used in UKAL for tax credits in relation to agricultural or industrial processes use.

2.22 Initial pre-consultation stakeholder engagement, with Scottish-based quarries near the border, has indicated that businesses could add a section to their sales ticket that would require the customer to indicate where they are taking the aggregate, for example in the form of a tick box with an option for Scotland and an option for rUK. Using a tick box would limit the administrative burden on businesses. This would then allow the quarry operator to pay the correct tax and make a tax credit claim (if required).

2.23 Pre-consultation questions have been raised in relation to tax compliance and the ability to ensure that the declaration is accurate. Revenue Scotland has indicated that it would take an approach to compliance based on the level of risk identified, although each case will be based on the available facts and circumstances.

2.24 If a process to enable quarries to identify cross-border collections could not be established, quarry operators could find themselves liable for SAT where customers had collected aggregate and taken it across the border. This would create uncertainty for quarry operators and risk double taxation.

2.25 This option would need agreement from HMRC and the UK Government to be effective and avoid double taxation and we are continuing to work collaboratively with them on these options.

2.26 In this scenario, and subject to agreement from HMRC and the UK Government, the customer declaration could be evidence retained by the rUK quarry to claim a tax credit on their UKAL liability (so avoiding double taxation) as well as to support their corresponding declaration of SAT. The rUK quarry would need to retain the customer declaration to enable Revenue Scotland and HMRC to check tax has been paid correctly at a later date, if required.

rUK quarry operator’s tax position

- rUK quarry to register and account for UKAL (commercial exploitation when supply to Scottish customer made from rUK quarry). However, rUK quarry can claim UKAL tax credit, evidenced by the declaration obtained from the customer (as same supply of aggregate moved from rUK to Scotland)

- rUK quarry to obtain a declaration from their customer confirming where the aggregate is being transported to

- rUK quarry to register & pay SAT (commercial exploitation as aggregate has been supplied to Scottish quarry from rUK)

Questions

2. Would the declaration approach set out in this scenario be workable for suppliers and / or customers? If there are issues, can you please specify?

3. Would the inclusion of a box on a supplier’s sales ticket to indicate the customer’s destination be easy to implement? If not, can you please provide reasons.

4. Do you think the proposed approach would create any opportunities for non-compliance?

5. Are there any alternate approaches that you think should be considered?

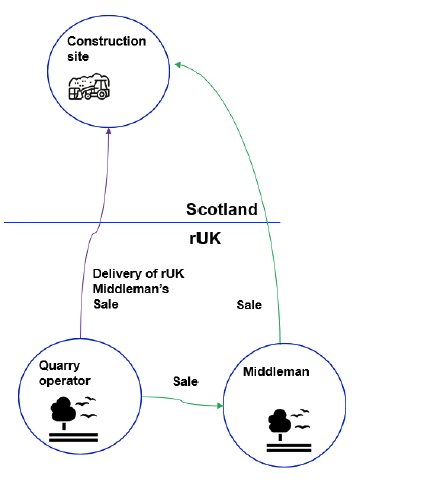

Indirect supply

Introduction

2.27 Further stakeholder engagement has identified indirect supplies that will create increased complexity with regards to cross-border taxation following the devolution of SAT.

2.28 An indirect supply involves multiple links in a supply chain for supplies originated in rUK and being received by a Scottish customer. Similar to the approach taken to direct supplies, the underlying principles of destination country taxation, tax compliance and market distortion are important considerations in relation to the handling of indirect supplies.

2.29 In an indirect supply scenario, there will be a point of commercial exploitation at the point where a rUK supplier sells aggregate to a rUK middleman and this will result in a liability to UKAL for the rUK supplier. In addition, there will be a further point of commercial exploitation when the aggregate is sold to a Scottish customer, this transaction will be exempt from UKAL as UKAL has already been paid but it will result in a SAT liability. This will therefore create a double taxation position, which we are aiming to resolve through the options set out in this consultation.

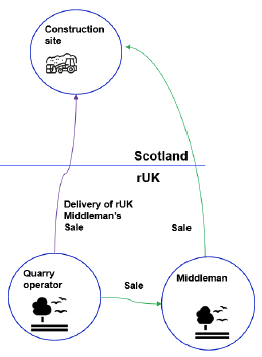

2.30 The indirect supply scenario includes:

a) where aggregate is supplied from a rUK middleman to a Scottish customer, but sourced from a rUK based supplier who also delivers it to the Scottish customer on the middleman’s behalf (i.e. producer-based delivery); and

b) where a rUK producer supplies aggregate to an rUK middleman who then supplies it on to a Scottish customer (i.e. over-the-counter sales)

2.31 Irrespective of whether the middleman scenario involves over-the-counter sales or producer-based delivery, there carries a risk of double taxation, which we are looking to address. These scenarios are illustrated in Diagram 3.

Tax points

1. aggregate is supplied from the rUK quarry

2. SAT becomes liable at the point the aggregate is supplied to the Scottish customer

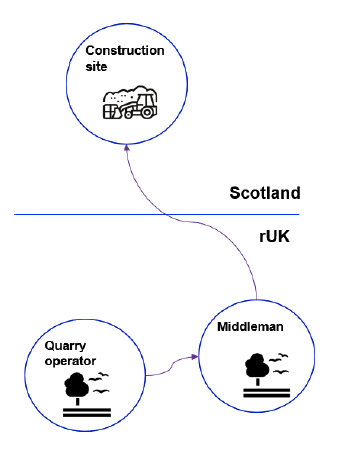

Producer-based delivery

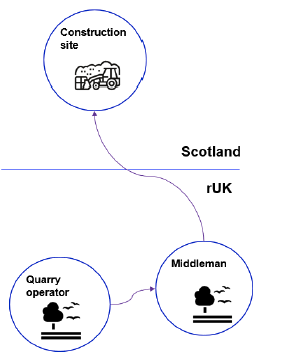

2.32 Producer-based delivery refers to situations where a rUK middleman supplies aggregate to a Scottish customer, with the material sourced and delivered directly by a rUK-based supplier on the middleman’s behalf. Industry engagement suggests this model is typically used for high-volume aggregate purchases. This scenario is illustrated in Diagram 4.

2.33 In this case, where the aggregate is delivered directly from a rUK quarry to a Scottish site, it constitutes commercial exploitation in Scotland. SAT is therefore due to be paid and the person responsible for this payment could be the rUK quarry operator or the rUK middleman. The Scottish Government is proposing that the simplest solution would be for the rUK quarry to register for and pay the SAT as this would be more in line with what happens currently under the UKAL regime. The quarry operator would also be required to declare the sale under UKAL but may claim a tax credit as the aggregate has been moved to Scotland. The middleman will not be required to register for SAT or UKAL in relation to the aggregate sold to the Scottish customer as the tax has already been accounted for and paid by the rUK quarry.

2.34 This approach would require rUK quarry operators to be able to identify SAT-liable sales made on behalf of rUK middlemen. Initial feedback from UKAL taxpayers indicates that delivery location data would make this possible.

2.35 If quarry operators apply UKAL to these cross-border transactions without clarity on the final destination, they risk dual liability under both UKAL and SAT. To address this, the Scottish Government are actively collaborating with HMRC and the UK Government to develop a workable approach. Details will be published after the consultation has concluded.

rUK quarry operator's tax position

- rUK quarry to register and declare/account for UKAL (commercial exploitation in rUK when supplying aggregate to rUK middleman). However, rUK quarry can make tax credit claim for UKAL as aggregate has moved to Scotland

- rUK quarry will register & pay SAT (commercial exploitation when aggregate supplied from rUK quarry to Scottish customer)

Questions

6. What are your views on the practical application of this approach?

7. Would this approach have a business impact, administrative and/or commercial, on aggregates suppliers and middlemen?

8. Do you think the proposed approach would create any opportunities for tax avoidance?

9. Are there any alternative approaches that you think should be considered?

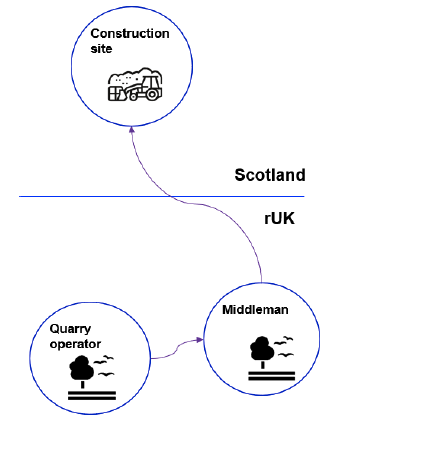

Over-the-counter sales

2.36 Over-the-counter sales are where a rUK based middleman, such as a builders’ merchant, supplies aggregate to a Scottish based customer from their own stock of aggregates. These sales tend to be bagged aggregate as they are smaller in volume. For over-the-counter sales there may be more than one middleman in a supply chain.

2.37 In this case, the rUK quarry supplies the aggregate to the middleman, constituting commercial exploitation in rUK and triggering a UKAL liability for the rUK quarry. When the middleman sells the aggregate to the Scottish customer there would be no UKAL liability as UKAL has already been paid by the rUK quarry. The rUK middleman would be liable to SAT on the sale to the Scottish customer however. There is therefore a double taxation issue to resolve.

2.38 Scottish Government and Revenue Scotland consideration of this scenario has identified two potential options for the tax treatment of middlemen in order to resolve the double taxation issue. Other factors considered as part of development of these options has included: alignment with legislative powers, tax compliance considerations, and market distortion impacts.

2.39 As the over-the-counter sales scenario is more complex, it will require a different tax approach than what has been described for producer-based delivery. In order to ensure that the correct tax can be reported by quarry operators, they will therefore be required to distinguish between sales made and delivered to middlemen (over-the-counter sales) and sales delivered on behalf of middlemen (producer-based delivery).

2.40 This distinction is necessary under both Option 1 and Option 2 to ensure correct tax application. Input from quarry operators on their ability to make this distinction is requested as part of this consultation (see the Questions section, specifically Question 9).

Option 1: Middlemen are exempt for over-the-counter sales

2.41 Under Option 1, over-the-counter sales - where an rUK-based middleman (e.g., a builders’ merchant) supplies aggregate from their own stock to a Scottish customer - would be exempt from SAT if UKAL has already been paid on the aggregate.

2.42 To prevent double taxation further up the supply chain, any subsequent supply of that aggregate would be exempt from SAT, as UKAL has already been paid. Neither the middleman nor any Scottish-based party in the supply chain would be required to register for or pay SAT. However, the middleman should maintain appropriate records, and they may also be required to notify Revenue Scotland of these exempt supplies.

2.43 Option 1 is illustrated in Diagram 5.

2.44 While this option introduces different tax treatments for each delivery model, it avoids double taxation and is viewed by those stakeholders engaged as part of the pre-consultation engagement process as practical and proportionate. The middleman may be required to provide a notification of exempt supply, which would support effective compliance oversight by Revenue Scotland and HMRC.

2.45 Option 1 would maintain the principle that the destination country retains the tax (see point 2.3.2).

rUK quarry operator's tax position

- rUK quarry to pay UKAL (commercial exploitation in rUK when physically supplying aggregate to rUK middleman)

rUK middleman

- No SAT due as UKAL has already been paid further up the supply chain. A notification to Revenue Scotland may be required to declare the exempt cross-border activity

Questions

10. What are your views on the practical application of Option 1? For example, would there be any administrative or commercial reasons why Option 1 would not work?

11. Do you think option 1 would create any opportunities for tax avoidance, if so can you provide examples?

12. Can a middleman distinguish between over-the-counter sales and producer-based delivery sales in their accounts?

13. Can a quarry operator distinguish between sales made and delivered to a middleman (for over-the-counter sales) and sales made to a middleman but delivered to the middleman’s customer (producer-based delivery)?

14. Would you propose any amendments to Option 1? If so, can you please provide details as to why the amendment would be an improvement.

15. What would be the business impacts of Option 1 on aggregate suppliers and middlemen?

16. What are your views on the potential requirement for middlemen to provide a declaration to Revenue Scotland to notify exempt supply? Would there be any reason why a notification would not be able to be supplied, for example?

Option 2: Middlemen to provide a declaration to quarry operators for over-the-counter sales, and quarry operator to register and pay SAT for producer-based delivery

2.46 Option 2 provides another potential approach, illustrated in Diagram 6, to resolve the double taxation issues. This option would see the quarry operator registering for and paying SAT based upon a declaration made by the rUK middleman.

2.47 For this option, the rUK middleman would provide a declaration to the rUK quarry operator to indicate what proportion of aggregate purchased by the middleman will be sold or moved to another jurisdiction (i.e. Scotland). The rUK quarry operator would then be responsible for paying the appropriate UKAL and SAT, based upon the declaration given by the middleman. This can then be used by HMRC and Revenue Scotland to check that the correct tax has been reported.

2.48 The example below provides an indication of how a declaration for over-the-counter sales would work. For simplification, the example assumes that the rate of SAT and UKAL are the same (£2.08 per tonne in 2025-26). This is for illustrative purposes only, and does not indicate any particular policy decision by the Scottish or UK Government:

- A rUK middleman purchases 1000 tonnes of crushed rock from a rUK quarry. To indicate the proportion of this aggregate ultimately being sold/moved to Scotland (and therefore liable to SAT), the middleman provides a declaration to the rUK quarry. In this case, the rUK middleman has indicated that 40% of the 1000 tonnes of rock purchased will be sold on to Scottish based customers. The rUK quarry will use this declaration to calculate its tax liability. In this case, they would declare and pay £832 SAT ((1000 x 40%) x £2.08)) to Revenue Scotland and £1,248 ((1000 x 60%) x £2.08)) to HMRC. The rUK middleman will have no requirements to register or complete a tax return to HMRC or Revenue Scotland.

2.49 With this option, the tax points would remain with UKAL taxpayers (rather than their customers). As noted previously, retaining the quarry operator as the taxpayer has been suggested to be less distortive in terms of market disruption. However, this option may result in additional administrative costs on aggregate suppliers and middlemen.

2.50 Pre-consultation engagement has indicated that this option may create several challenges, including how the declaration would work in practice, whether a declaration would be required on all purchases by middlemen or whether a broader arrangement could be put in place, and how this could be verified and monitored in terms of tax compliance. The declaration approach could create an administrative overhead for both the aggregates supplier and middleman. Engagement with aggregate businesses has indicated that a declaration would need to be for a significant period of time, such as an annual declaration, as it would otherwise be overly burdensome.

2.51 Furthermore, engagement with industry stakeholders has indicated that there may be more than one middleman in a supply chain. Therefore, providing a declaration in such circumstances would be administratively burdensome for both middlemen and quarry operators, and likely to be inaccurate as a result of different sources in the supply chain.

rUK quarry operator’s tax position

- Register & pay UKAL (commercial exploitation in rUK when supplying aggregate to rUK middleman)

- Register & pay SAT (Scottish commercial exploitation when aggregate moved to Scotland)

- rUK quarry will need to obtain a declaration from the rUK middleman to indicate the amount of aggregate which has moved to the Scottish customer

- rUK quarry is responsible for paying the appropriate proportion of both UKAL and SAT, based upon declaration given by middleman

Questions

17. What are your views on the practical application of option 2? For example, would there be any administrative or commercial reasons why Option 2 would not work?

18. Do you think option 2 would create any opportunities for tax avoidance, if so can you provide examples?

19. Would you propose any amendments to Option 2? If so, can you please provide details as to why the amendment would be an improvement.

20. What would be the business impacts of Option 2 on aggregate suppliers and middlemen?

C. Other complex scenarios

2.52 The Scottish Government and Revenue Scotland are aware that the middleman and collections scenarios are more commonplace and therefore require focussed analysis. However, we are aware that there could be further cross-border scenarios, distinct from those already outlined in this paper, which may also require more detailed consideration. For example, we are aware of scenarios where aggregate may cross back and forth across the border between Scotland and rUK.

2.53 This consultation therefore also seeks feedback on any additional cross-border scenarios that will require consideration as a result of the introduction of SAT.

Questions

21. Are there any further cross-border scenarios that need to be addressed in advance of the introduction of SAT? If yes, please provide as much detail as possible, setting out the factual circumstances and, if possible, your views on the best way in which to deal with these scenarios.

Contact

Email: Cara.Woods@gov.scot