Scotland's Fiscal Devolution Story

An account of how Scotland's fiscal landscape has transformed over the past 3 decades, with an overview what fiscal devolution has enabled, how the system now operates and the medium-term challenges ahead.

2012-2016: emerging fiscal powers

From 2012, a series of reforms significantly increased the Scottish Parliament’s tax and spending powers, informed by two key reviews: the Calman Commission (2008-09)[8] and the Smith Commission (2014)[9]. Both reviews aimed to increase the financial accountability of the Scottish Parliament.[10]

The Scotland Act 2012 gave the Scottish Parliament greater fiscal responsibility by increasing its powers over Income Tax – reforms that were much better formulated than the previous unused ‘variable rate’ – and by devolving Stamp Duty Land Tax and Landfill Tax. With these, the Scottish Parliament would directly raise a proportion of the money it would spend, setting rates and thresholds for devolved taxes (within limits for Income Tax) and with revenues based on actual tax receipts from Scottish taxpayers, rather than being pooled across the UK.

These reforms were the most significant legal transfer of power since devolution in 1999. They created national-level devolved taxes within the UK and a distinct Scottish taxpayer for the first time.

The Scotland Act 2016 gave the Scottish Parliament significantly greater autonomy and a stronger stake in the performance of the Scottish economy. The Scottish Parliament would now have:

- the power to set Income Tax rates and bands on all earned income – meaning all non-savings, non-dividend (NSND) income, over 90% of income taxes in Scotland,

- the power to introduce devolved taxes in Scotland to replace the UK Aggregates Levy and Air Passenger Duty,

- the ability to create new devolved taxes with UK Government agreement

- assignment of around half of Scottish Value-Added Tax (VAT) revenues,

- legislative competence over a range of social security benefits, mainly relating to disability, carers, maternity, and funeral and heating expenses and

- the power to create new benefits in devolved areas and top up existing UK benefits.

Each set of reforms was significant and groundbreaking. In each case, legislation and supporting instruments had to be developed quickly. The Smith Commission, for example, published its recommendations in just over two months, with the resulting Scotland Act 2016 delivered in just over a year.[11] Both Acts were subject to significant parliamentary and public scrutiny, with success being seen as a key test of Scottish Government competence and of the value (or not) of devolution itself.

New fiscal framework

The devolution of new fiscal powers required the Scottish and UK Governments to agree detailed rules and mechanisms to manage their financial consequences. The detail of how the block grant would be adjusted to reflect Scotland’s new fiscal powers was particularly critical for determining how risks (such as population growth or economic shocks) would be shared between the two governments.

After almost a year of negotiation, the Fiscal Framework Agreement between the Scottish and UK Governments was signed in 2016, setting rules for an initial five-year period[12]. It aligned with a set of principles including the ‘no detriment’ principle[13]’, taxpayer fairness, economic responsibility and fiscal shock resilience. It also specified the limits within which the Scottish Government could borrow and draw on reserves to manage capital investment, short-term cash shortfalls and forecast errors in tax revenues or social security spending.

From the outset, it was recognised that, as a product of negotiation, the Fiscal Framework was a compromise. Given this, both governments agreed to commission an independent report on the different methods that could be adopted on a permanent basis to adjust the block grant to take account of revenues raised by devolved taxes and of devolved social security benefits. Both governments recognised that circumstances were expected to change over time and agreed that the Agreement should be reviewed periodically to ensure it remained fair, effective and responsive to changing conditions.

The 2023 review of the Fiscal Framework drew on a jointly commissioned independent report, whose authors included Professor David Bell from the University of Stirling, David Eiser from the Fraser of Allander Institute, and David Phillips from the Institute for Fiscal Studies, and informed by wider stakeholder input[14].

The renegotiated Fiscal Framework Agreement included the permanent adoption of the indexed-per-capita (IPC) mechanism for the block grant adjustment (BGA). This ensured that Scotland’s funding continued to be protected from the impact of Scotland having slower population growth relative to the rest of the UK. The annual resource borrowing limit to cover forecast errors was doubled from £300 million to £600 million (in 2023-24 prices). The resource and capital borrowing limits, and the cap on the Scotland Reserve, are now indexed to inflation. Constraints on drawing down from the Scotland Reserve were abolished to improve flexibility for the Scottish Government to carry funds between financial years.[15]

New powers, new opportunities, new risks

These new powers enabled the Scottish Government to develop its own distinctive fiscal policy. It has used these powers to introduce a more progressive tax system than the rest of the UK, including a five-band Income Tax system and a more progressive schedule of tax on residential property transactions via the Land and Buildings Transaction Tax (LBTT). It has enhanced the accessibility of devolved social security benefits and has created new benefits such as the Scottish Child Payment.

At the same time, fiscal devolution and the rules under which it would operate meant that Scotland’s public finances and the preparation of budgets became more complex and more uncertain, with new risks that needed to be well-managed, and shorter timeframes to prepare Scottish budgets.

Scottish budgets would now depend on three elements:

- the block grant determined by the Barnett Formula, a mechanism that allocates Scotland a population share of comparable spending in England, adjusted to reflect devolved tax and social security powers,

- the tax policy choices of the Scottish and UK Governments; and

- the relative performance of Scottish tax revenues, particularly whether tax revenues per head grow faster or more slowly than the equivalent taxes in the rest of the UK.

As for any government, Scotland’s tax revenues fluctuate with the performance of the economy. However, the performance of Scottish tax revenues relative to the rest of the UK also determines how the block grant is adjusted each year. If Scotland’s tax revenues grow more quickly than the equivalent tax revenues in the UK, Scotland will be better off; if those revenues grow more slowly, Scotland will be worse off. The Scottish Government therefore bears the risk not only of changes in revenues due to its own policy choices, but also for any factor that shifts economic performance relative to the UK, including due to UK Government decisions.[16]

Demand for devolved social security benefits also fluctuates in response to economic conditions, levels of need, and shocks such as the COVID-19 pandemic or cost-of-living crisis. Unlike the rest of the UK, where social security spending is classified under Annually Managed Expenditure (AME) and adjusted automatically with changing demand, the cost of devolved Scottish benefits is included within the Scottish Government’s overall Departmental Expenditure Limit (DEL), which is subject to fixed annual limits.[17] If demand for these benefits rises, the Scottish Government would need to secure additional funding through taxation or cut back on other spending.

Although AME classification may appear to offer more flexibility, the funding arrangements set out in HM Treasury’s Statement of Funding Policy[18] mean that this would not provide additional protection for the Scottish Budget. Where programmes are funded through AME, devolved governments must meet the cost of offering more generous provision than the UK Government. Because the Scottish Government has chosen to deliver a more generous social security system, a move to AME would still require the Scottish Government to fund any additional costs resulting from its own policy choices. It would also remove the current discretion to use the Social Security block grant adjustment for other spending.

In addition, under the Fiscal Framework, the Scottish Budget is informed by forecasts of revenues and welfare spending, which can only later be ‘reconciled’ with actual data, resulting in retrospective adjustments, either positive or negative. Forecasting is not an exact science. If, as will almost always be the case, actual revenues differ from forecasts, the reconciliation process can affect the Scottish Budget for several years.

The changes also saw the Scottish Parliament gaining new borrowing powers. However, these powers, and the ability to save into and draw from the Scottish Reserve was limited, providing little flexibility in balancing the budget each year or over the medium-term.

In practical terms, the operation of the Fiscal Framework means that the timeframes under which Scottish Budgets can be prepared are constrained. Forecasts of expected devolved tax revenues and social security payments, and the adjustments made to the UK block grant to reflect these, are not known until the autumn, when the Office for Budget Responsibility (OBR) publishes independent forecasts for Scotland alongside the UK budget. As a result, the Scottish Government’s budget cannot be considered by Parliament until November or December, or occasionally later, reducing the time available for parliamentary scrutiny.

In response to these challenges, a joint initiative by the Scottish Parliament and Scottish Government established the Budget Process Review Group (BPRG). Its 2016 recommendations played a key role in reshaping how budgets are developed and scrutinised in Scotland.[19]

Most importantly, the Scottish Budget process shifted from a single annual event to a year-round cycle. A Medium-Term Financial Strategy (MTFS) is published each May to enable parliamentarians to take account of forecast revenue and demand-led spending over a five-year period. A Fiscal Framework Outturn Report, including reconciliations, is published annually in September to enable parliamentary committees to scrutinise the public finances in advance of the formal budget process. These publications marked a significant improvement in transparency, providing a more comprehensive basis for debate about Scotland’s finances in the short and medium-term.

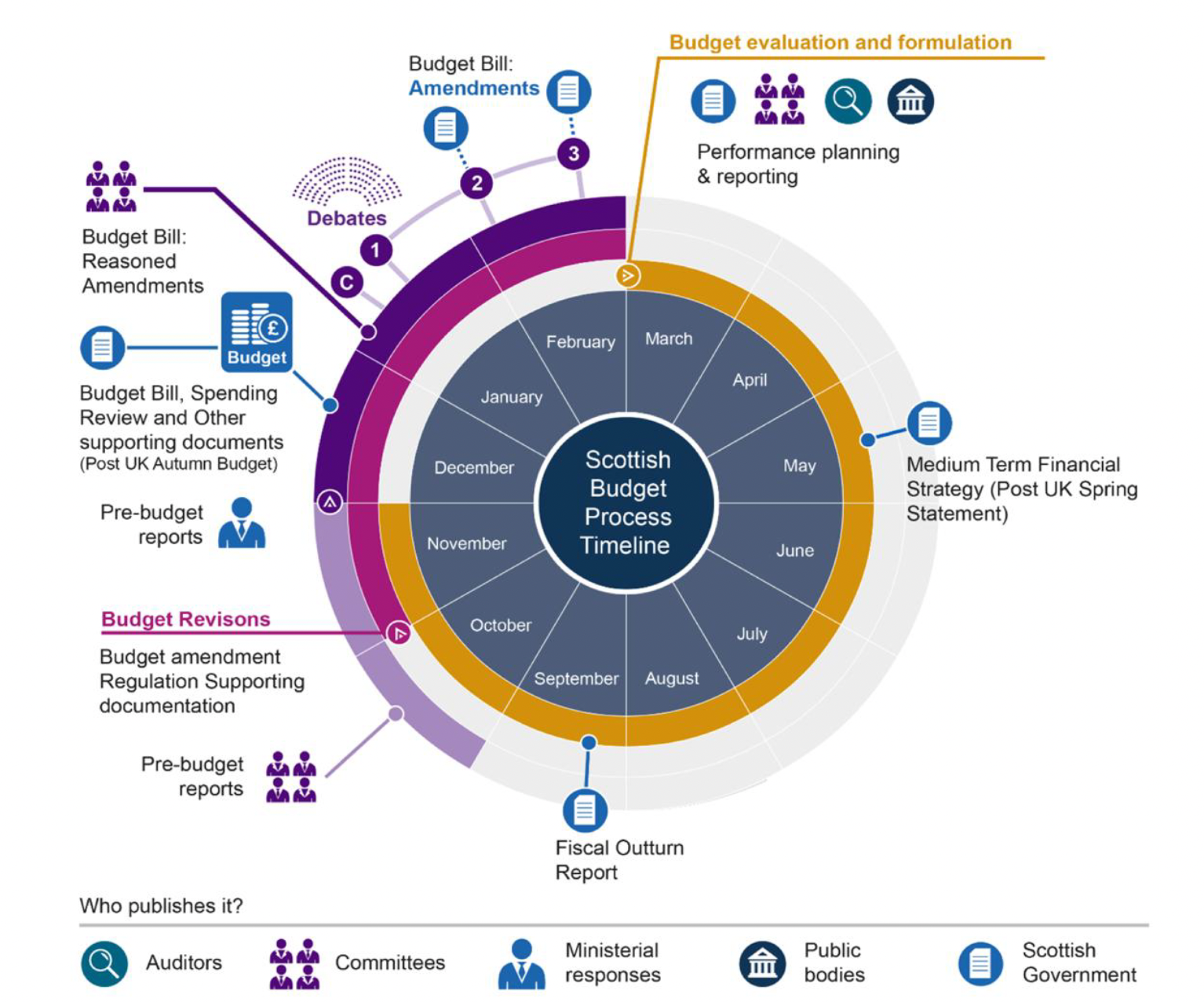

Scottish Budget process following the Budget Process Review Group’s recommendations

Source: Scottish Parliament Information Centre (SPICe)[20]

Budget evaluation and formulation (March –September)

Activities:

Performance planning and reporting.

Medium Term Financial Strategy (published after the UK Spring Statement, around May).

Fiscal Outturn Report (around September).

Budget Bill and Debates (October–February)

October–December:

Pre-budget reports are prepared.

Budget Bill, Spending Review, and supporting documents are published after the UK Autumn Budget.

December–February:

Budget Bill Reasoned Amendments are introduced.

Parliamentary debates take place.

Budget Bill Amendments (1, 2, and 3) are made during the process.

Budget Revisions (February–September)

February–September:

Budget amendment regulations and supporting documentation are produced.

Pre-budget reports accompany revisions.

Who publishes it?

The bottom section of the image lists icons showing who is responsible for different parts of the process:

Auditors

Committees

Ministerial responses

Public bodies

Scottish Government

Summary

The Scottish Budget process operates continuously throughout the year, with:

Formulation and evaluation in spring and summer,

Budget Bill and debates in winter,

Revisions and reporting continuing through the rest of the year.

This process continues to operate today, with the Parliament’s finance committees regularly reviewing and seeking to improve its effectiveness, most recently in its inquiry into the Scottish Budget process in practice.[21]

New institutions

Effective governance and institutions are essential to maintaining a country’s financial credibility by ensuring that public finances are managed responsibly, transparently and sustainably. The structure, independence and effectiveness of institutions directly impact how financial markets and credit rating agencies view a government’s fiscal trustworthiness.

Devolution of new fiscal powers required consideration of what fiscal institutions would be needed to ensure Scotland’s fiscal reputation was strong, to manage new powers and the fiscal opportunities and risks they presented effectively, and to collect and administer new taxes and social security benefits.

Throughout this period, officials reached out to other similarly constituted governments to understand the key elements, strengths and weaknesses, of their fiscal architecture. Informal discussions were undertaken with a range of international agencies to understand best practice and the considerations that would inform any assessment of Scotland’s financial credibility. From this it was clear that institutional governance and design at a country level, not only within government, would be critical.

Scottish Fiscal Commission

Careful consideration of international best practice highlighted the importance of credible economic and fiscal forecasts and the role played by an Independent Fiscal Institution in jurisdictions including Canada, Australia, Sweden, and the United States.

The Scottish Fiscal Commission (SFC) was initially established on a non-statutory basis, to provide scrutiny of Scottish Government forecasts, particularly for tax receipts. The SFC’s independence was emphasised from the outset through the appointment of expert, non-political commissioners. Its first Chair, Dame Susan Rice OBE, brought extensive qualifications and experience in banking, public service and economic governance, while the two other founding Commissioners, Professors Campbell Leith and Andrew Hughes-Hallet, brought academic macroeconomic and fiscal expertise.

Following the Scottish Fiscal Commission Act 2016, the SFC moved to a statutory footing in 2017. In preparing this legislation, the Scottish Government drew on both international best practice and assessment of how arrangements for other scrutiny bodies within Scotland, such as Audit Scotland, had performed. The Scottish Government aimed to ensure that the Scottish Fiscal Commission would be an exemplar of independence, with the legislation establishing stronger protections for the SFC’s independence than were in place for the Office of Budget Responsibility in the UK and appointments were required to be formally approved by the Scottish Parliament. The Bill was amended as the Scottish and UK Governments negotiated the first Fiscal Framework agreement. The SFC would now produce Scotland's official forecasts for devolved taxes, social security and the Scottish economy, and have broad power to produce other reports at its own discretion. The legislation obliged Scottish Ministers to base Scottish budgets on the Scottish Fiscal Commission’s official forecasts.

An early challenge for the SFC was to identify data sources and set up agreements with a range of Scottish and UK organisations to access data. In some cases, historic Scotland-specific data was limited, or unavailable, making initial forecasting difficult. The SFC also had to build its own models for forecasting and devolved taxes, social security and the economy with no pre-existing models at the Scottish level. While developing their understanding of Scotland's finances more deeply, the SFC have extended the scope of its analysis beyond forecasts of devolved taxes and social security spending to medium- and long-term fiscal sustainability. The Chair and Commissioners regularly give evidence on their forecasts and reports to the Scottish Parliament’s committees.

In line with best practice, the Scottish Fiscal Commission Act 2016 sets out that there must be an external, independent evaluation of the SFC two years after enactment, and every five years thereafter. The 2019 Organisation for Economic Co-operation and Development (OECD) review concluded that “the SFC has achieved many positive results in the two years since its creation, building good relationships with stakeholders and a reputation for independent and credible forecasts, and improving the fiscal policy debate in Scotland.” [22]

Similarly, the OECD’s 2025 review concluded that the Scottish Fiscal Commission “has built a reputation for rigorous analysis and transparency. Its work, grounded in international best practices, is crucial for guiding Scotland's economic and fiscal policy debate.” [23]

In its evidence to the Parliament’s Finance and Public Administration Committee, the OECD added that “in relation to how it compares internationally, the SFC is a very strong institution. Scotland can be quite proud of the standing and independence of the institution.”[24]

Revenue Scotland

Revenue Scotland was established in 2015 to collect and manage the newly devolved taxes: the Land and Buildings Transaction Tax and the Scottish Landfill Tax (SLT).

Ministers set high expectations for the quality of service the new non-ministerial organisation would provide, and the level of efficiency with which it would operate. Revenue Scotland was required to be responsive, digital, and lean – collecting taxes at a lower cost than His Majesty’s Revenue and Customs (HMRC) would charge for a similar service. From the outset, including in its design, it was to have a different and more positive relationship with stakeholders.[25] These were ambitious objectives for an agency initially responsible for only two small taxes, with limited scope for economies of scale and little existing tax administration expertise in Scotland.

Revenue Scotland was established under the Revenue Scotland and Tax Powers Act 2014 as a non-ministerial office. It is part of the Scottish Administration but independent of Ministers and accountable to the Scottish Parliament to ensure the administration of tax is independent, fair and impartial.

At the same time, the ongoing debate about independence or further devolution during 2014 and 2015 meant that any new tax collection agency needed to be ‘future-proofed’, to deliver not only the taxes being devolved under the Scotland Act 2012 but provide the institutional basis on which any further changes or additions to tax functions required by future Scottish Governments could be built.

From the outset, Revenue Scotland established an effective collection and management framework for the new devolved taxes and has continued to meet or exceed the OECD benchmark for efficient tax administration, of keeping running costs below 1% of the total tax collected. Even in its first year, more than 98% of tax returns were submitted online and 96% of written communications were responded to within 10 working days. Performance on all of these indicators improved further in its second year of operation and has been maintained since.[26]

While Revenue Scotland drew initially on expertise from HMRC and others, its first few years focused on developing specialist capability in each of its new functions, establishing effective compliance and wider corporate functions, prioritising learning and development that included the creation of a new tax profession within the Scottish Government. In 2018-19, the new Scottish Electronic Tax System, developed collaboratively with stakeholders and experts, transformed Revenue Scotland’s operations and created a more efficient system for taxpayers.[27]

Having celebrated its 10th anniversary, Revenue Scotland has evolved from a fledgling organisation of around 45 staff to an established and respected tax authority with a reputation for effective and efficient tax administration. Since its establishment, it has collected approximately £7 billion in revenue, contributing to the Scottish Consolidated Fund and financing essential public services across Scotland.[28]

As an organisation based in, and focused on, Scotland, Revenue Scotland is much more accessible to taxpayers and stakeholder organisations.

Looking forward, the scope of Revenue Scotland’s functions will expand, with the introduction of the Scottish Aggregates Tax (SAT) on 1 April 2026[29] and the planned introduction of Air Departure Tax (ADT) on 1 April 2027[30] and a Scottish Building Safety Levy (SBSL) on 1 April 2028.[31]

Social Security Scotland

Social Security Scotland was established in 2018, under the Social Security (Scotland) Act 2018, to administer the new social security benefits. The principles of dignity, fairness and respect were embedded in the legislation, with social security to be treated as a human right and the system co-designed with people with lived experience of the benefits system.

Initially, the Scottish Government relied on agency agreements with the UK Department for Work and Pensions (DWP) to deliver certain devolved benefits on its behalf while it developed equivalent new benefits. In other cases, completely new benefits were introduced by the Scottish Government with no DWP equivalent. Since 2018, Social Security Scotland has gradually rolled out these new benefits, including the Scottish Child Payment, Child Disability Payment, Adult Disability Payment, Best Start Grant and Best Start Foods, Carer’s Allowance Supplement and Funeral Support Payment. This process of devolution is almost complete. In 2026-27, it is estimated that Social Security Scotland will directly administer 97% of devolved benefits, or £7.1 billion per annum of benefit spending.

As benefit-making powers have been devolved, the new benefits have, where appropriate, been developed to have at least comparable rates and less intrusive application processes than UK equivalents. Efficient administration remains important. Social Security Scotland has a resource budget of £354.6 million to administer benefits in 2026-27. The resource budget settlement represents 4.9% of benefit expenditure which is line with the estimate of 5%[32] included in the Financial Memorandum for the Social Security (Scotland) Bill published in 2017. [33]

Benefit expenditure itself is demand-led and cannot be controlled in the same way as other budgets where spending limits can be set.

Consistent with Scotland’s emphasis on continual improvement and external review, the Scottish Commission on Social Security (SCSS) was set up in 2019 as an independent body, separate from the Scottish Government and the Scottish Parliament, to provide independent scrutiny of the Scottish social security system and hold Scottish Ministers to account.[34] Social Security Scotland’s Charter Measurement Framework tracks delivery against commitments, with a report published annually on how well it has implemented the principles of dignity, fairness and rights across its policy and operations.[35]

Scottish Exchequer

New fiscal responsibilities also had implications for the Scottish Government itself. Fiscal policy became more complex, with greater opportunities and risks, much greater multi-year interaction between budgets based on forecasts that would later be adjusted for reconciliations, and a wider set of economic and social factors that would impact on both devolved tax revenues and demand-led social security spending and, in turn, be impacted by them. Policy development needed both to take account of much wider dynamics and impacts and be developed in collaboration with a broader set of stakeholders.

In response, in 2017 the existing Director General (DG) Finance role was changed by agreement to a new DG Scottish Exchequer role, with a remit to establish those Exchequer functions required in the new Scottish devolved landscape. Day-to-day finance functions were moved to align with other corporate functions situated in DG Corporate, such as HR, IT and procurement, to be led by a Chief Financial Officer, overseeing the Financial Management Directorate in the Scottish Government.

To shape the new Exchequer function, officials developed a maturity model, identifying the functions, capacity and capabilities required in the short-, medium- and longer-term, to support the Government’s aspirations for inclusive growth, fiscal sustainability, national outcomes, financial risk management, and transparency.

The resulting Scottish Exchequer was established as part of the Scottish Government, headed by the Director General Scottish Exchequer, and responsible for supporting the Cabinet Secretary for Finance with fiscal strategy, policy, and analysis; and the overall Scottish Budget, including taxation and public spending (such as public sector pay and infrastructure spending). The role of Internal Audit within the Scottish Government was also situated in DG Scottish Exchequer, and its functions were expanded to include assurance activities.

The Scottish Exchequer has overseen the production of the Medium-Term Financial Strategy since its first publication in 2018. This was the first time the Scottish Government had set out, and committed to regularly publishing, a statement of its financial projections including the potential medium-term untreated gap between expected funding and revenues, and its assessment of the fiscal challenges that block grant adjustments, economic uncertainty and budget volatility could create for Scottish Budgets. Over time, the Exchequer has developed the MTFS[36] to strengthen its focus on management of fiscal risks, provide a range of funding and spending scenarios, enhance its modelling and, most recently, include actions to be taken to support delivery of the strategy with the ultimate aim of closing the fiscal gap, as set out in the Fiscal Sustainability Delivery Plan (FSDP).[37]

DG Scottish Exchequer worked with the Financial Management Directorate, to drive improvements in the openness and transparency of the Scottish Government’s finances. The Scottish Budget now includes data by classification of functions of Government (COFOG), an internationally approved and consistent way of identifying spending by function, and comparisons between proposed spend and actual (rather than budgeted) spend in the previous year. This is an ongoing process, with commitments to further improve the accessibility of fiscal information to the public set out in the Scottish Government’s Open Government Action Plan.[38]

The establishment of the Scottish Exchequer was a significant change within the Scottish Government. It coincided with a growing understanding in the Scottish Parliament and wider society that new devolved powers had significant financial implications that would require a more sophisticated approach. Its teams and functions have been designed to deliver advice for fiscally sustainable decision making, advise on how best to grow and protect Scotland’s tax revenues and drive long-term public value from public spending and investment.

The Scottish Exchequer has recently been brought together with the Director General for Strategy and External Affairs to form the new DG Exchequer, Strategy and Performance, creating a more integrated strategic centre for the Scottish Government.

Other institutions

Other fiscal organisations have developed significantly to respond to the new fiscal landscape and to support parliamentary scrutiny of Scotland’s devolved fiscal powers.

The Scottish Rate of Income Tax (SRIT) is collected by HMRC on behalf of the Scottish Government, following an exercise to identify Scottish Income Taxpayers. A service-level agreement sets out requirements and performance measures to ensure a consistent quality of service to Scottish taxpayers and enable both HMRC and the Scottish Government to meet their respective responsibilities for its operation.[39]

Audit Scotland was established on 1 February 2000, following the implementation of the Public Finance and Accountability (Scotland) Act 2000 – part of a significant reform in Scotland’s public audit framework. Audit Scotland was created to support both the Auditor General for Scotland and the Accounts Commission, consolidating audit responsibilities under one independent public body. In 2018, it established a financial powers audit team in recognition of the significance of the change in fiscal powers, building its capacity to audit their implementation and then ongoing administration. It now regularly briefs the Parliament’s Finance and Public Administration Committee as well as the Public Audit Committee.

COVID-19 and its aftermath

Along with the rest of the UK and many other countries, the COVID-19 pandemic and the subsequent cost-of-living crisis created unprecedented challenges for the Scottish Government. Unlike other countries, Scotland was responding to these within the limits set by the Fiscal Framework and with a set of fiscal institutions that had only recently been established and were still developing their capabilities.

These relatively new institutions adapted quickly and performed well. In response to the pandemic, Revenue Scotland rapidly transitioned from predominantly office-based working to full remote operations. Tax systems remained fully functional without interruption, with all tax returns and payments able to be made digitally; security was maintained; service targets were met; and additional measures to assist taxpayers (such as suspension of penalties and debt pursuit) put in place. While tax revenue inevitably fell short of forecasts due to the pandemic-related slowdown in the housing market, tax collection remained effective despite the difficult circumstances.[40]

Social Security Scotland also swiftly transitioned its workforce to remote operations, rolling out new digital tools such as web chat and online document upload to support applications. It continued to roll out new social security benefits, maintaining high levels of client satisfaction throughout.[41]

The Fiscal Framework continued to operate during this period. New flexibility was provided by a temporary funding arrangement known as ‘guaranteed funding’, which provided a guaranteed a level of ‘consequential’ funding to Scotland and the other devolved administrations in advance of any Barnett block grant funding arising from the UK Government’s responses to the crisis. The guarantee took effect from July 2020, five months after the pandemic began.

This delay highlighted the limitations of existing arrangements, as the Scottish Government lacked certainty over its funding in the early months of the pandemic. This issue may arise again in future, particularly if the need for emergency measures emerges first, or is more acute, in a devolved nation, or if bespoke arrangements are required in different parts of the UK to meet local needs.

The journey so far, and looking to the future

The scale and speed of fiscal devolution in Scotland since 1999 has been unprecedented. In a little over a quarter of a century, the Scottish Parliament and Scottish Government have moved from being almost entirely reliant on the Barnett formula-driven block grant from the UK Government, the size of which was not related to Scottish economic performance and could not be altered by Scottish administrations, to raising a significant portion of the Scottish Budget from taxes in Scotland. A range of new fiscal institutions have been established and operated very successfully, despite increased volatility, new fiscal risks and significant global turmoil.

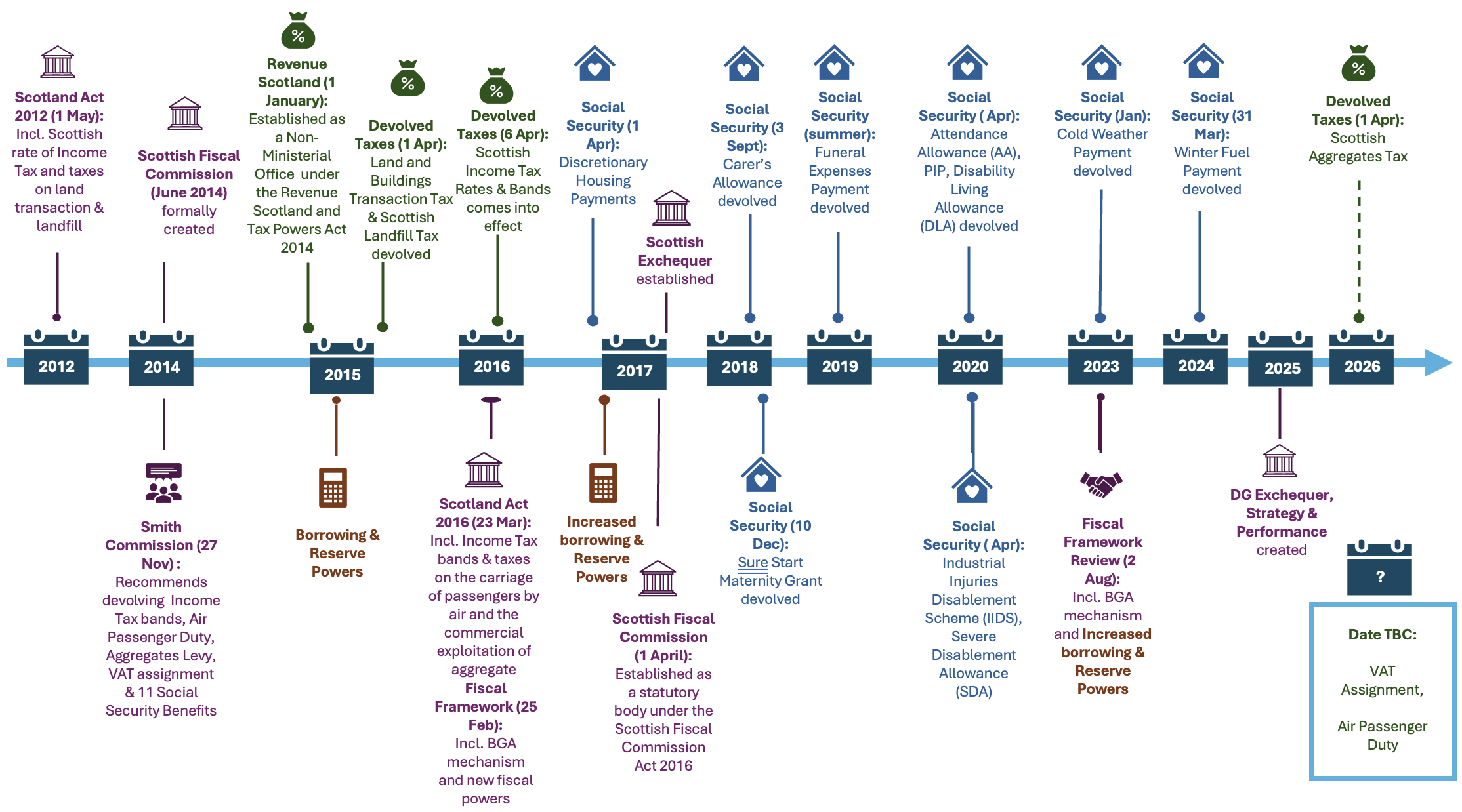

Scotland Fiscal and Social Security Powers Timeline (2012–2026), shows the gradual devolution of fiscal and social security powers to Scotland between 2012 and 2026.

- 2012: Scotland Act 2012 (1 May) — includes Scottish rate of Income Tax and taxes on land transactions and landfill.

- 2014: Scottish Fiscal Commission (June) formally created. Smith Commission (27 Nov) recommends devolving Income Tax bands, Air Passenger Duty, Aggregates Levy, VAT assignment, and 11 Social Security Benefits.

- 2015: Revenue Scotland (1 January) established as a Non-Ministerial Office under the Revenue Scotland and Tax Powers Act 2014. Devolved Taxes (1 Apr) — Land and Buildings Transaction Tax and Scottish Landfill Tax devolved.

- 2016: Devolved Taxes (6 Apr) — Scottish Income Tax rates and bands come into effect. Scotland Act 2016 (23 Mar) includes Income Tax bands and taxes on land transaction and landfill. Fiscal Framework (25 Feb) includes BGA mechanism and new fiscal powers.

- 2017: Increased borrowing and reserve powers. Scottish Fiscal Commission (1 Apr) established as a statutory body under the Scottish Fiscal Commission Act 2016.

- 2018: Social Security (3 Sept) — Carer’s Allowance devolved.

- 2019: Social Security (summer) — Funeral Expenses Payment devolved. Social Security (10 Dec) — Sure Start Maternity Grant devolved.

- 2020: Social Security (Apr) — Attendance Allowance, Personal Independence Payment (PIP), and Disability Living Allowance devolved.

- 2021: Social Security (Apr) — Industrial Injuries Disablement Scheme and Severe Disablement Allowance devolved.

- 2022: Social Security (Apr) — Discretionary Housing Payments devolved.

- 2023: Social Security (Jan) — Cold Weather Payment devolved. Fiscal Framework Review (2 Aug) — includes BGA mechanism and increased borrowing and reserve powers.

- 2024: Social Security (31 Mar) — Winter Fuel Payment devolved.

- 2025: DG Exchequer, Strategy & Performance —created.

- 2026: Devolved Taxes (1 Apr) — Scottish Aggregates Tax devolved.

- Date TBC: VAT Assignment and Air Passenger Duty.

Devolution of agreed powers is still underway, with the planned implementation of the Scottish Aggregates Tax, Scottish Building Safety Levy and Air Departure Tax. The Scottish Government has outlined its intention to go directly to the bond market in its own right for the first time and is considering options for a bond issuance in 2026-27.[42]

In October 2023, the Scottish Government outlined its intention to go directly to the bond market in its own right. Achieving a credit rating to raise Scotland’s profile in the international capital markets was recommended by the Independent Investor Panel that year. In November 2025, the Scottish Government received the highest feasible credit rating it could achieve, securing parity with the UK Government. This was a significant milestone in the Scottish Bond Programme, and the Scottish Government is now making the necessary preparations for a multi-year programme over the next parliamentary term, subject to the outcome of the Scottish Election in May 2026. The total value of the programme is expected to be £1.5 billion, with issuances of roughly £300 million per annum expected in line with the already published Capital Borrowing Policy. The first bond issuance is anticipated in the latter half of 2026-27.

The Scottish Government’s ability to make the most of fiscal devolution has depended on constructive working relationships between the Scottish and UK Governments, at both Ministerial and official level, and across a range of organisations including HM Treasury, the Office for Budget Responsibility, HMRC and DWP. Reaching agreement on, and then working within, the Fiscal Framework has required negotiation and compromise on both sides; no agreement can specify every detail or anticipate every eventuality, so its effective operation has depended on co-operation and goodwill. The pandemic illustrated and reinforced the importance of maintaining and continued improvement of methods of joint working, processes and structures, and relationships between the four nations of the UK.

Following the UK Government-led review of intergovernmental relations in 2022, finance intergovernmental relationships for the four nations of the UK were formulised through the Finance Interministerial Standing Committee (F:ISC) which comprises the relevant finance ministers from the UK Government and the Devolved Governments. F:ISC meetings typically take place each quarter around key fiscal milestones and adheres to an agreed term of reference. The aim of F:ISC is to consider the impact of economic and finance matters affecting the UK.

Fiscal devolution has significantly increased the Scottish Parliament’s fiscal control and accountability. It has enabled Scotland to set distinct tax and spending policies, making Scottish taxes more progressive and designing social security benefits to contribute to outcomes such as reducing child poverty, and deliver both taxes and benefits differently.

Scotland has also been able to take a different approach to developing and implementing policies. From the outset, taxes have been designed in consultation with stakeholders and the wider public, with evaluation and continual improvement a hallmark of Scotland’s approach; benefits have been designed with the active involvement of people with personal experience of the social security system and are regarded as a shared investment.

Devolution has also brought increased financial risk for the Scottish Government to manage. The Scottish Budget is now much more exposed to the structural risks in the Scottish economy, from population ageing to other economic factors. The time lag between forecasted tax revenues and reconciliations based on actual levels of Scottish Income Tax revenues can impact budgets over multiple years. Scotland remains reliant on the UK Government block grant for a substantial portion of its funding, and in-year spending changes by the UK Government directly affect Scotland’s devolved budget, adding to volatility and uncertainty.

The inclusion of tax powers in the devolution settlement has helped expand fiscal dialogue and debate in Scotland. Parliament’s role has shifted from a focus largely on allocating a block grant transferred from Westminster to responsibility for raising a significant portion of government funding. Parliamentary scrutiny is a year-round process. Publication of the Scottish Government’s MTFS and the SFC’s long-term fiscal sustainability reports are building the stock of knowledge about the longer-term structural and strategic challenges that Scotland will face in future.

Distinct policies and new risks have required new institutions and tools to manage them. Scotland’s new fiscal institutions are highly credible and well-regarded, both within Scotland and internationally. Institutions have been created or extended to advise on and administer fiscal policy and Scottish Budgets (Scottish Exchequer), taxes and benefits (Revenue Scotland, Social Security Scotland), and dedicated parliamentary scrutiny (the Finance and Public Administration Committee and the Public Audit Committee) informed by independent forecasting and review (Scottish Fiscal Commission, Scottish Commission on Social Security) and external audit and assurance (Audit Scotland). Despite being only recently established, and operating at a time of unprecedented global challenges including EU Exit, the COVID-19 pandemic and cost-of-living crisis, institutions have been highly effective in overseeing and administering fiscal devolution.

Looking to the future

The fiscal system must continue to evolve to adapt to new challenges. The complexity of the devolution settlement creates challenges for parliamentary and wider public understanding and scrutiny. This is compounded by the dynamic volatility created by economic and fiscal forecasts that can only ever be best estimates, and external shocks that cannot always be anticipated. There are now many more interactions between devolved and reserved powers, including the separation of Income Tax on earnings (devolved) from Income Tax of other income (savings and dividends), and National Insurance Contributions (powers reserved to the UK Government), which can create anomalies and perverse incentives.

This can also mean that parliamentary and public scrutiny and debate focuses on small, specific aspects of the framework, rather than the big picture.[43] Policy proposals are not always assessed within the financial context provided by SFC forecasts and the MTFS, although these have increasingly become a yardstick for judging the credibility of proposals.

While the Scottish Parliament’s Finance Committee and others have argued that more needs to be done to support a strategic and multi-year approach to financial planning, the Scottish Government has achieved a balanced budget each year, often in difficult circumstances. The Committee’s recent Inquiry found a broad consensus from witnesses that the introduction of the MTFS had been a positive and welcome step and called for it to be developed further, to include a greater level of detail and disaggregation, and more information about plans to manage identified pressures and risks, to support more effective committee scrutiny and influence.[44] The proposal by the UK Government for a regular cycle of Spending Reviews will assist this strategic approach, given the continued importance of the block grant in determining the funding available to Scotland.

There are challenges in improving the level of transparency and public understanding of the public finances in a complex fiscal system like Scotland’s. The work of bodies like the Fraser of Allander Institute, the Institute for Fiscal Studies and the Scottish Fiscal Commission are important in offering independent and trusted sources for policymakers, media and the public. Their contributions to improve communication and education around fiscal events are vital to supporting informed public debate.

The novelty of tax devolution, and the need to set rates and bands for devolved taxes, has meant that tax policies have tended to dominate debate on fiscal issues. Yet as has been set out in the MTFS, the largest fiscal challenges over the next years are expected to arise from the growing demand for spending. The OECD has highlighted increasing budgetary pressures due to an ageing population, increasing healthcare costs, new social security measures and climate commitments. Barnett consequentials for Scotland in future years may also tighten, given the fiscal pressures faced across the UK and the subsequent spending decisions the UK Government may need to take.[45] In either case, and with a requirement to fund Scottish social security from within an overall capped DEL, spending decisions will need to be based on robust and clear evidence. In the coming years, there will need to be debate about the trade-offs and choices required over the medium-term to manage the growing differential between revenues and spending.

The OECD and the Scottish Parliament’s Finance and Public Administration Committee have highlighted the need to improve Scottish Parliament capability and capacity to scrutinise and debate fiscal options and choices. They have called for additional financial and economic training for MSPs to ensure they are up to date on the growing complexity of Scotland’s public finances and to support more effective scrutiny of budgetary matters and encourage a wider debate around the Scottish Government’s tax and spending decisions.[46] This will be particularly important after the May 2026 Scottish Parliament election, to ensure that new and returning MSPs are well-equipped to engage with and further the debate at the start of the new parliamentary session.

The Scottish Parliament’s Finance and Public Administration Committee has asked the Scottish Government to take forward the OECD’s recommendation that the Scottish Fiscal Commission broaden and deepen its spending analysis to provide “robust independent analysis” of spending pressures across the budget, not just in social security, to help support a more informed debate about the trade-offs needed to ensure the public finances are on a sustainable path.[47] The Scottish Government has recently published the 2026 Scottish Spending Review[48], which marks an important step forward in setting out the fiscal context in which we operate and the spending challenge faced by Portfolios across Government.

While the policy decisions of Scottish Governments will drive future developments, some key challenges and opportunities are clear.

Challenges remain in co-ordinating Scottish Government budgets with UK fiscal events, given short lead-in times between forecasts and confirmation of the block grant, and Scottish Budgets. There are questions about how risk is, or should be, shared between the Scottish and UK Governments and what tools Scotland should have to manage volatility or shocks.[49]

Reliance on the UK Government block grant, the size of which is dependent on the UK Government’s own spending choices, makes it difficult for the Scottish Government to plan ahead, or to give greater certainty about funding to the many public and not-for-profit organisations that provide vital services to the people of Scotland. This is particularly evident when shocks generate new spending needs, as was highlighted in the early months of the COVID-19 pandemic. Practical issues have emerged such as forecasting errors and funding risks if Scottish tax revenues grow more slowly than in the rest of the UK. The requirement to balance a budget each year with very limited scope to set money aside in the Scottish Reserve or borrow – meaning the government has only a very limited ‘overdraft-type’ capacity, creates a “use-it or lose-it” dynamic that reduces flexibility and makes real multi-year planning difficult.

The UK contrasts with a number of other countries in not having some form of fiscal equalisation to reflect differences in the revenue-raising capacity or spending needs of different parts of the country. It has also been suggested that Scotland and the UK have a fairly narrow definition of ‘no detriment’ in terms of being no better or worse off from replacing an element of funding for Scotland with taxes.[50] The Scottish Government has limited powers to manage these risks, with caps on the amounts it can borrow or put aside in reserves. The next review of the Fiscal Framework agreement is due to take place in 2028, but the Scottish Government has called on the UK Government to agree to an earlier review to consider issues such as borrowing and reserve limits in the context of the overall size of the Scottish Budget.[51]

Looking ahead, it will also be important to further assess the interaction and cumulative impacts of Scotland’s tax policy decisions at both national and local levels, as recognised in the Scottish Government’s Tax Strategy.[52] Tax powers have been added incrementally to the pre-devolution local taxes (Council Tax and Non-Domestic Rates), starting with Land and Buildings Transaction Tax and Scottish Landfill Tax in 2015-16, followed by the Scottish Rate of Income Tax in 2016, with Aggregates Tax, Air Departure Tax and the Scottish Building Safety Levy due to be rolled out in 2026, 2027, and 2028 respectively. At local government level, Edinburgh will be the first local authority to adopt a Visitor Levy in 2026, with Glasgow, Aberdeen City, West Dunbartonshire and Stirling Councils all having approved schemes to progress after Edinburgh. Several other councils are in the process of consulting but are awaiting the outcome of the Visitor Levy (Amendment) Bill progressing through Parliament, which is expected to complete scrutiny prior to Parliament rising in March 2026. The Scottish Government is currently considering giving local authorities the power to impose a cruise ship levy.[53] The Scottish Government is also working closely with Local Government to build consensus on the future of the Council Tax system. Work between the Scottish and UK Governments on how to assign a proportion of VAT revenues to the Scottish budget is ongoing.[54] The Scottish Government has also explored the introduction of a Carbon Emissions Land Tax.[55]

Responsibilities and administration of these taxes and levies are spread across national and local levels, with separate IT and delivery systems, and across different divisions within the Scottish Government and different Parliamentary committees. Whilst work has and continues to be done to ensure policy coherence, there are further opportunities for improvement, especially operationally.