Scottish Budget 2022 to 2023: Your Scotland, Your Finances

Guide setting out key information about how the system of public finances in Scotland stands in 2022 to 2023, and how this system is changing.

Your Scotland, Your Finances: 2022-23 Scottish Budget - Key facts and figures for 2022-23

Competent, financially prudent Scottish Government

Devolved Finances

- The Scottish Government is accountable to the Scottish Parliament and the people in Scotland for its use of public money.

- Scottish Ministers decide spending plans that have to be approved by Holyrood.

- Since 2009-10, the Scottish Government has produced its accounts on the basis of international accounting standards.

Barnett Formula

Westminster decides how much it will spend in England on public services. Holyrood is automatically allocated a population share of changes in spending on public services devolved to Scotland.

Money In

Block Grant, Scottish Income Tax, Land and Buildings Transaction Tax, Scottish Landfill tax, Non-domestic Rates, Borrowing, Scotland Reserve

The Scottish Consolidated Fund

Money Out

Spending on priorities including Schools, Hospitals, Police, Housing, Farming, Fishing, Infrastructure and the Economy

Delivered by Scottish Government, Executive Agencies, NHS, Crown Office, Local Councils, Third Sector and Other Bodies

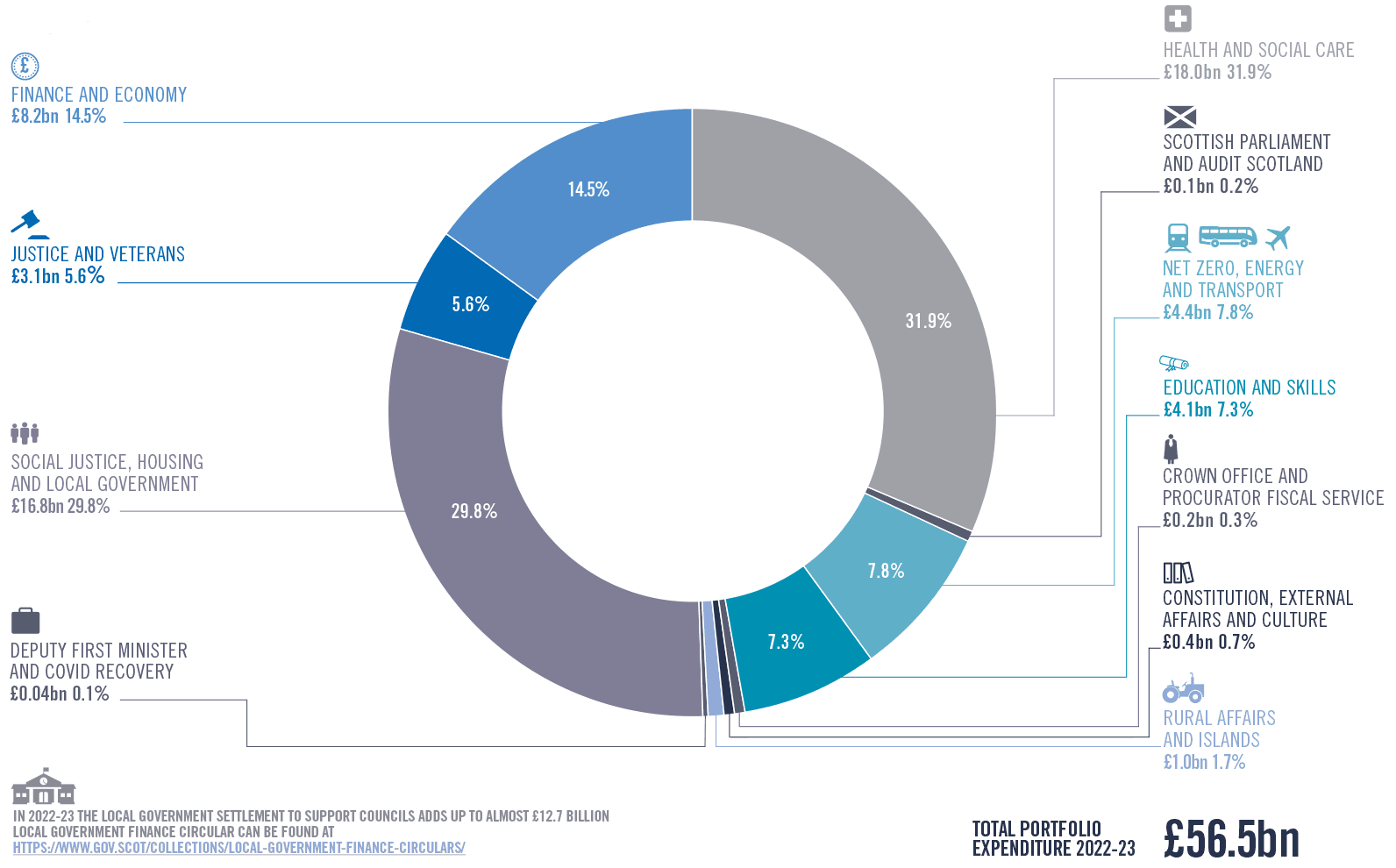

Our financial system in 2022-23

Scottish Budget in 2022-23 is £56.5 Billion

Scotland’s Published Accounts

- The Scottish Government's latest published accounts are for 2020-21 and they were given a clean bill of health by Audit Scotland. This was the 16th consecutive year they received an unqualified opinion.

Payments Made

- For financial year 2020-21 the Scottish Government, its Executive Agencies and the Crown Office and Procurator Fiscal Service made 96.6% of all payments within 10 days.

Block Grant Adjustment

- For all taxes set, raised or assigned in Scotland, the block grant is reduced. Additions are made for social security expenditure now devolved.

Equality And Fairer Scotland Budget Statement

- We have published an Equality and Fairer Scotland Budget Statement which considered how the new Budget would impact on key inequalities across protected characteristics and socio-economic disadvantage, as well as on human rights. Found at https://www.gov.scot/publications/equality-fairer-scot land-budget-statement-2022-23/

Taxes Set in Scotland in 2022-23:

Scottish income Tax

The Scottish Parliament has control over parts of Income Tax paid in Scotland, specifically the power to set the rates and bands of Income Tax paid on non-saving, non-dividends income.

This is income earned through employment, self-employment, pensions or property.

Scottish Income Tax is collected by HMRC and the money raised through the tax is transferred to the Scottish Government. The latest rates and bands can be found at https://www.gov.scot/publications/scottish-income-tax-2022-2023/

Non-Domestic Rates

Non-Domestic Rates (NDR), often referred to as ‘business rates’, are a tax paid on non-residential property. This includes supermarkets, high street retailers, schools, and even ATM sites and billboards. The amount of NDR paid is generally based on the estimated rental value of the property on the open market.

The Scottish Government sets the tax rate, but the tax is administered and collected by local authorities to spend on local services like education, social care and waste management. More information can be found at https://www.gov.scot/policies/local-government/non-domestic-rates/

Land And Buildings Transaction Tax

Land and Buildings Transaction Tax is the tax payable on land or property transactions in Scotland over a certain value. Taxpayers pay the tax via their solicitor when buying a home. Tax is also payable on non-residential property transactions, such as the purchase or lease of office or other commercial buildings.

The current rates for Land and Buildings Transaction Tax can be found at https://www.gov.scot/policies/taxes/land-and-buildings-transaction-tax/

Scottish Landfill Tax

Scottish Landfill Tax is a tax on the disposal of waste to landfill. The tax provides a financial incentive to reduce the amount of waste going to landfill, and therefore encourages recycling and the re-use of material. You will likely never pay this tax directly, instead, it is paid for by landfill operators who pass on costs to waste management services, businesses, and Local Authorities.

The current rates for Scottish Landfill Tax can be found at https://www.gov.scot/policies/taxes/landfill-tax/

The Scottish tax landscape 2022-23

Illustrative chart based in devolved powers in 2022-23

UK Government

- Fuel Duty

- Oil & Gas Receipts

- Income Tax

- National Insurance

- Corporation Tax

- Air Passenger Duty

- Vat

- Tax on Alcohol, Cigarettes

- Inheritance Tax

- Capital Gains Tax

UK Block Grant

Scottish Government

- Scottish Income Tax (Collected by HMRC)

- Business Rates (Collected by Local Authorities and Redistributed by SG)

- Land and Buildings Transaction Tax (Collected by Revenue Scotland)

- Scottish Landfill Tax (Collected by Revenue Scotland)

Local Government Finance Circular

Local Government Finance Circular Includes:

- General Revenue Grant

- Business Rates

- General Capital Grant

- Specific Revenue and Capital Grants

Local Government

- Council tax

- Receipts and Rents

What is planned to be spent in 2022-23

The Fiscal Framework - from 1999 to today

Timeline of Change

1999

- Scottish Parliament can increase or reduce Income Tax by 3p in the Pound

- Scottish Parliament has powers over Non-Domestic Rates

2015

- Introduction of Land and Buildings Transaction Tax and Scottish Landfill Tax

2016

- Scottish Parliament gains partial powers to set the Scottish rate of Income Tax and also gains an increase in borrowing powers

2017

- Scottish Parliament gains further powers to set Income Tax rates and Bands

2018

- Two new bands are added to the Scottish Income Tax system to improve fairness, protect lower earning taxpayers and raise more funding for public services

2022 and future years

- Assignment of VAT Receipts

- Replacement for Air Passenger Duty

- Aggregates Levy

- Review of the Fiscal Framework

The Fiscal Framework

Is an agreement from 2016 between the UK and Scottish Governments that sets the rules for how Scotland’s Tax and Social Security Powers are managed and implemented.

- The Smith Commission - on whose conclusions the Fiscal Framework is based - envisaged a fundamental change in how the Scottish Government would be funded. It foresaw a substantial proportion of the Government’s Budget coming directly from tax revenues raised in Scotland and greater borrowing powers.

- The main objective of the Fiscal Framework is to support the transfer of tax and social security powers to Scotland while, to a significant extent, retaining the stability of Block Grant funding. It also provides the Scottish Government with some limited borrowing powers.

- The guiding principle of the Framework is ‘no detriment’. This means neither the Scottish nor the UK Government being worse off as result of the powers transferring.

How the Scottish Budget is calculated

- Component One – Barnett formula determined Block Grant – Barnett continues to determine the initial size of the Block Grant.

- Component Two – Block Grant Adjustments (BGA) – The Block Grant is adjusted to reflect the impact of the transfer of tax and social security powers to the Scottish Budget.

- Component Three – Devolved Revenues – These are the revenues now retained from devolved tax powers which contribute to Scotland’s funding.

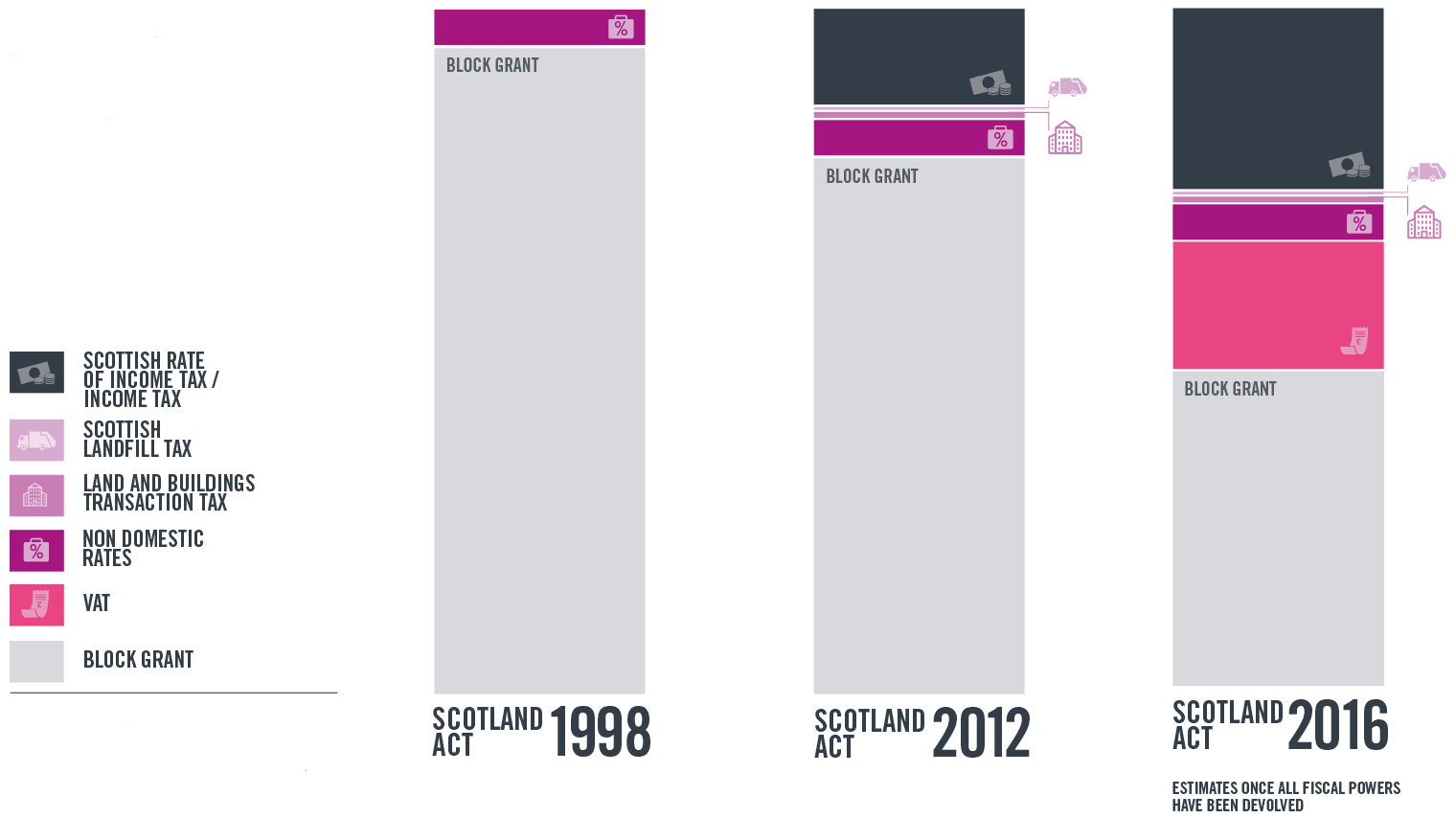

How our funding system is changing

Chart shows illustrative share of budget based on estimates from 2017-18 figures.

Figures for Scotland Act 2016 also include revenues based on the Scottish share of UK Air Passenger Duty and the Aggregates Levy.

In addition Local Uauthorities set and raise Council Tax to fund local services, but this is outwith the Scottish Budget

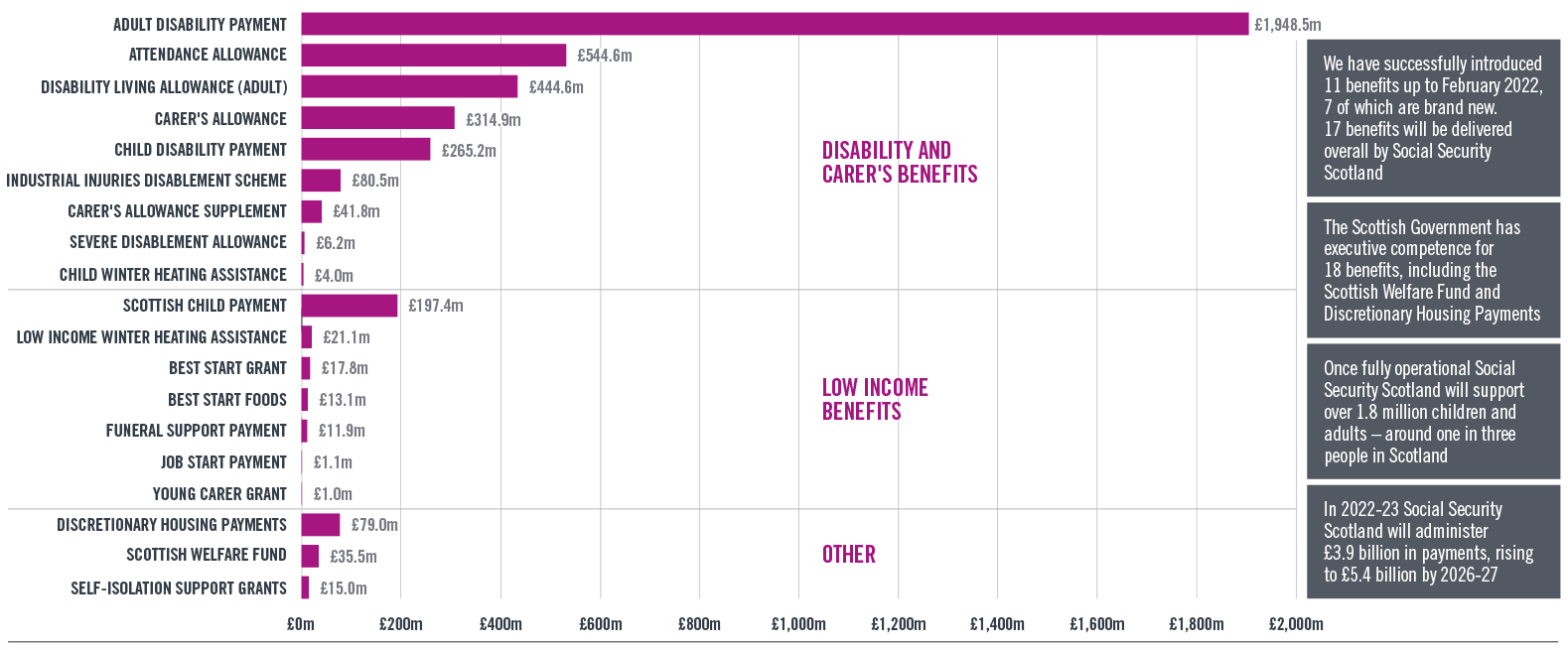

Social Security delivering for Scotland

Further benefits to be delivered

- Adult Disability Payment (Summer 2022 / Pilot Spring 2022)

- Pension Age Winter Heating Assistance

- Scottish Carer's Assistance

- Pension Age Disability Payment

- Carer's Additional Person Payment

- Employment Injury Assistance

- Low Income Winter Heating Assistance (Winter 2022)

* All figures (except Job Start Payment and Young Carer Grant) based on Scottish Fiscal Commission forecast December 2021

Contact

Email: ScottishBudget@gov.scot