Air quality report 2022: public engagement

Findings from a quantitative study exploring public perceptions of air quality in Scotland among adults.

5. Attitudes towards and take up of Ultra Low Emission Vehicles and Public Transport

5.1 Ultra Low Emission Vehicles

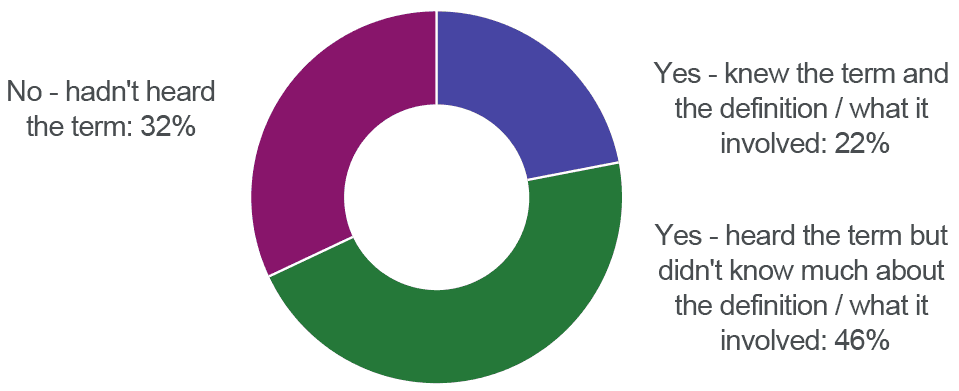

A third (32%) of Scots had not heard the term Ultra Low Emission Vehicle before taking the survey, while just 22% knew the term and the definition and what it involves. 46% had heard the term ULEV but didn’t know much about the definition or what it involed.

Men are significantly more likely to say they know the term and definition of ULEV (30%), while just 29% said they hadn’t heard the term. Just 15% of women say they know the term and definition, and 35% say they’ve not heard it before. Awareness of ULEVs and understanding of the term also increases as you go up the income scale. For example, 15% of those with a household income of £15k or less say they know the term and definition, rising to 34% among those with a household income of £70k and over.

C03b: Have you heard about Ultra Low Emission Vehicles (ULEVs) before taking this survey?

Unweighted base: 1,520

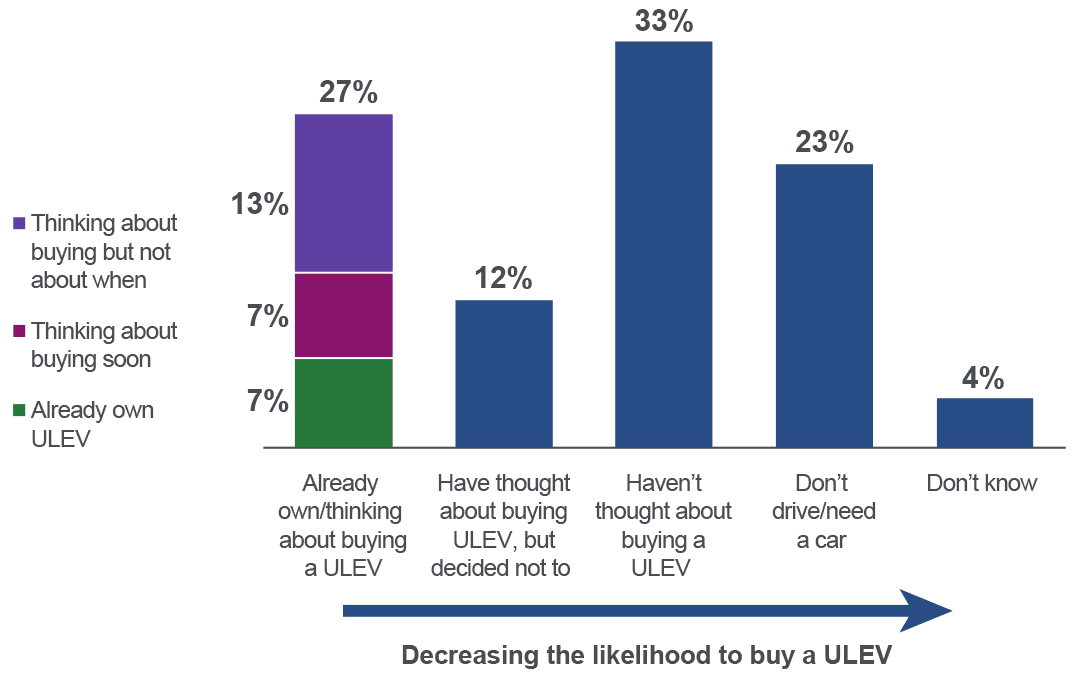

7% of respondents already own or are thinking about buying a ULEV[3]: 7% of respondents already own a ULEV, while another 7% are thinking about buying one quite soon, and 13% have thought about buying a ULEV but not when they will buy one. A third (33%) have not thought about buying one. The likelihood of not having considered buying a ULEV decreases according to respondents’ income. 39% of respondents with a household income of £15-25k say they haven’t thought about buying a ULEV, compared to 28% of those with a household income of £70k and over.

Looking at the urban/rural divide, respondents living in remote rural areas are more likely than those living in large urban areas to say they have not thought about buying a ULEV (47% cf. 25%).

C04 Thinking specifically about ULEV cars or vans, which of these statements best describes your current attitude towards buying a ULEV car or van?

Unweighted base: 1,520

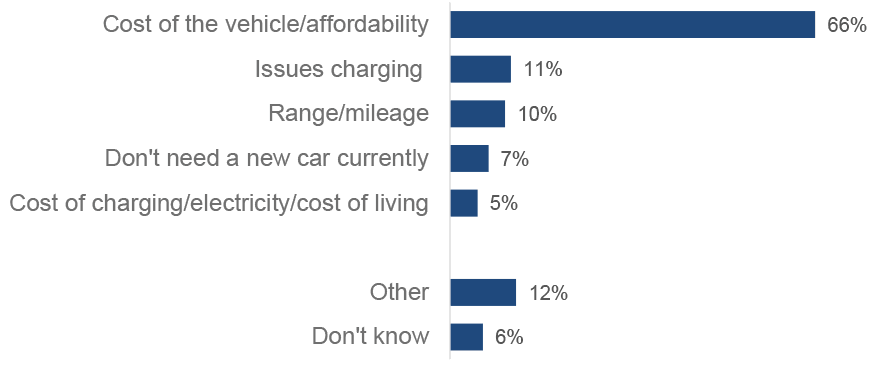

Among respondents who thought about buying a ULEV but decided not to (12%), the most common reason for not doing so is cost/affordability (66%). Around one in ten cite charging issues (11%), range/mileage (10%), and not needing a new car (7%).

C04A Please tell us why you decided not to buy an Ultra-Low Emission vehicle

Unweighted base: 191

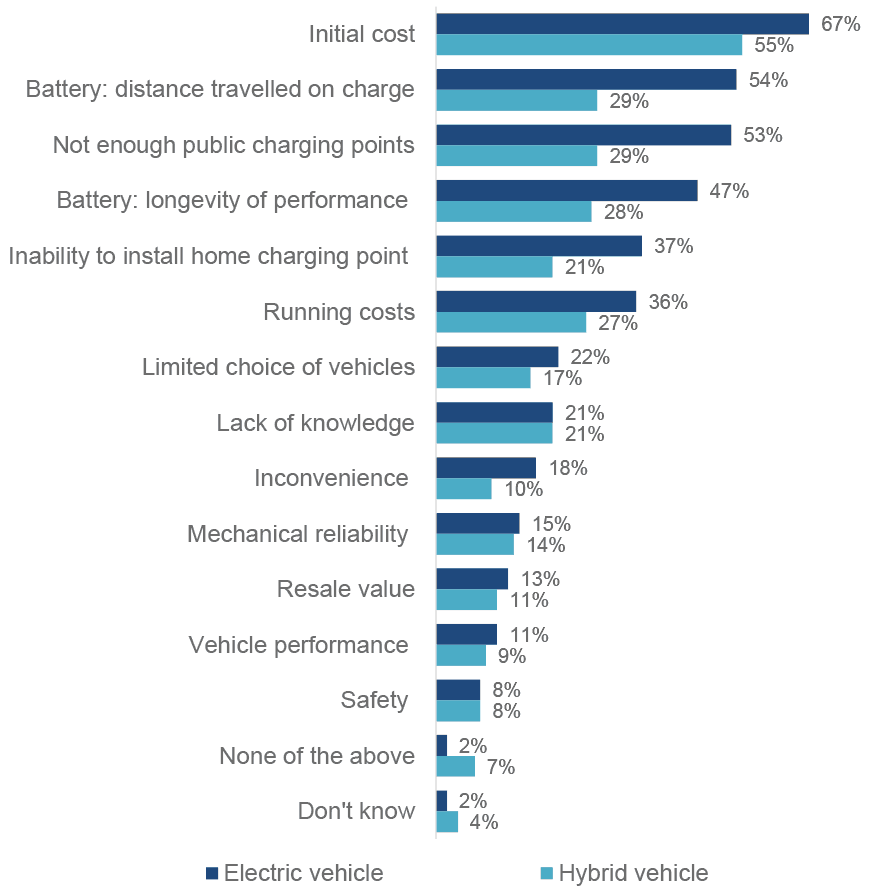

Respondents were also asked to think about potential barriers in greater detail with specific reference to both electric and hybrid cars. The initial cost is the most important deterrent when buying either an electric (67%) or hybrid (55%) vehicle. Battery issues around the distance you can travel (54% and 29% respectively), access to charging points (53% and 29% respectively) and longevity (47% and 28% respectively) follow as more secondary concerns.

Generally, respondents identify more deterrents to buying an electric vehicle than a hybrid vehicle, which is unsurprising given that, apart from cost, the main barriers relate to battery issues.

The longevity of performance for electric cars is a greater issue among those living in accessible rural areas compared to an urban area (58% cf. 40%) where the average distance travelled each day is likely to vary significantly. Similarly, the distance travelled on a charge is of greater concern to those in remote rural areas compared to large urban areas (66% cf. 49%).

Meanwhile, the initial cost is unsurprisingly less important for respondents on higher incomes. For example, 77% of those on a relatively modest household income of £30-35k cite it as a barrier, compared to 51% of those earning £85-100k.

C05: If you were to buy a car or van in the next 12 months, what, if anything would put you off buying an electric/hybrid vehicle?

Unweighted base: 1,129

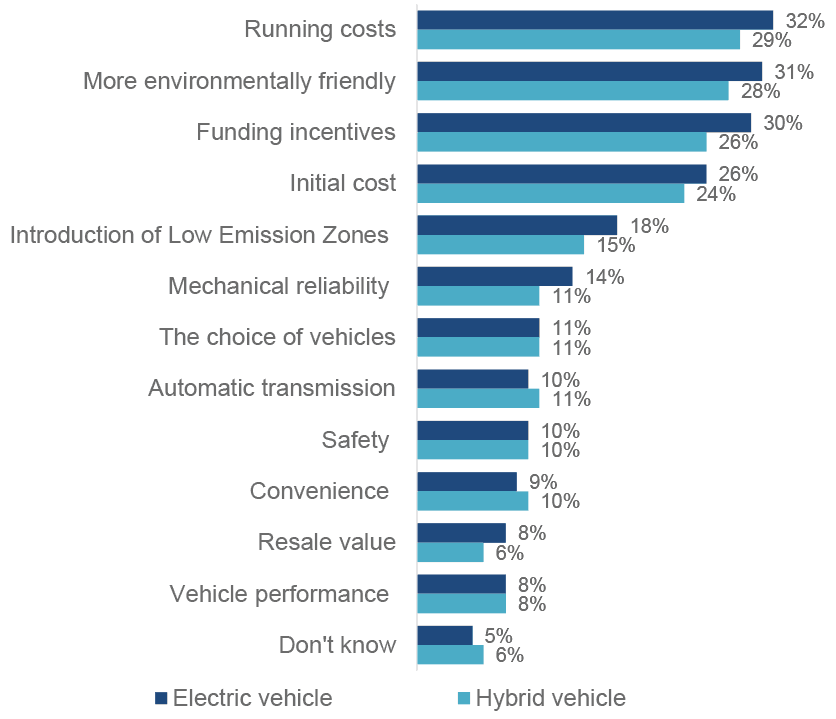

Running costs are an important incentive to buying either an electric (32%) or a hybrid (29%) car, as are environmental considerations (31% and 28% respectively), funding incentives (30% and 26% respectively) and the initial cost (26% and 24% respectively).

Generally, and unlike perceived barriers, the pattern of response is very similar with regards to incentives to buy electric or hybrid cars.

C06: If you were to buy a car or van in the next 12 months, what, if anything, about current ULEV vehicles would encourage you to buy one?

Unweighted base: 1,129

When asked what was the single most appealing aspect about a ULEV, the environmental benefit is the most common response for both electric and hybrid cars (29% and 28% respectively).

Cost is a unique factor in determining whether respondents would or would not buy a ULEV: the initial cost of purchasing a ULEV acts as a barrier to purchasing either an electric or hybrid vehicle and appears to have a greater influence on the decision-making than the incentive of potentially lower running costs. Indeed, the running costs of a ULEV is more of a barrier than an incentive, though the proportion who say so for hybrid vehicles is closely aligned (27% barrier, 29% incentive).

When key considerations are looked at together, the initial cost of a ULEV deters most Scots from buying one despite the opportunity for cheaper running costs, and the potential environmental benefit encourages them. In a trade-off between costs and environmental benefits, the initial cost is a greater deterrent to buying a ULEV than the environmental benefit is as an incentive.

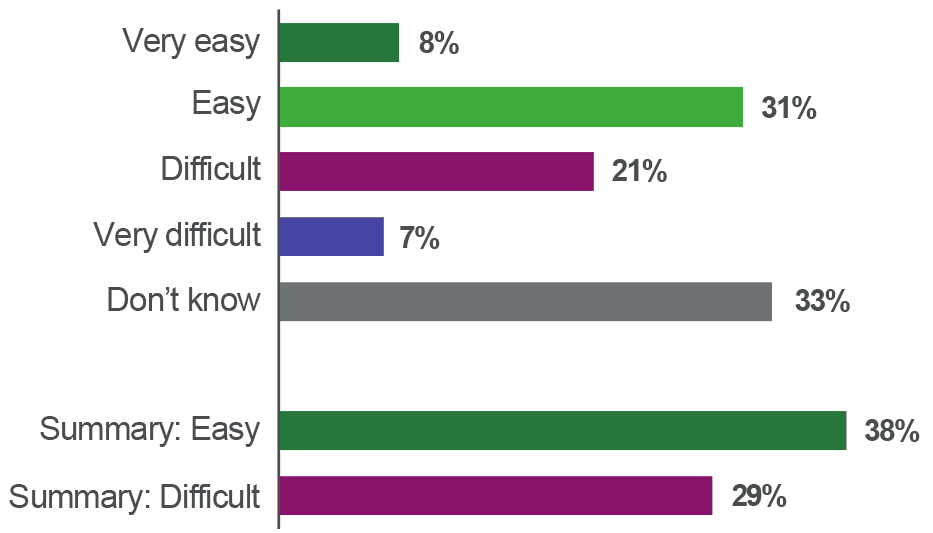

While slightly more Scots think it’s easier to find a ULEV for sale than say it is difficult (38% and 29% respectively), a third (33%) do not know.

C07: How easy or difficult would you say it is to find an Ultra-Low Emission Vehicle for sale in Scotland?

Unweighted base: 1,129

The perception that it is easy to find a ULEV for sale in Scotland is higher among men than women (47% cf. 30%). Respondents in Central Scotland are also more likely to say it’s easier to find a ULEV (48%) compared to those in the North East (29%), while those living in large urban areas consider it easier (44%) compared to 54% in remote small towns who don’t know whether it would be easy or difficult.

Respondents who are more concerned with local air quality are more likely to say finding a ULEV is easy (48%) compared to those who are not concerned (31%), with a sizeable proportion of this latter group saying they don’t know either way (42%).

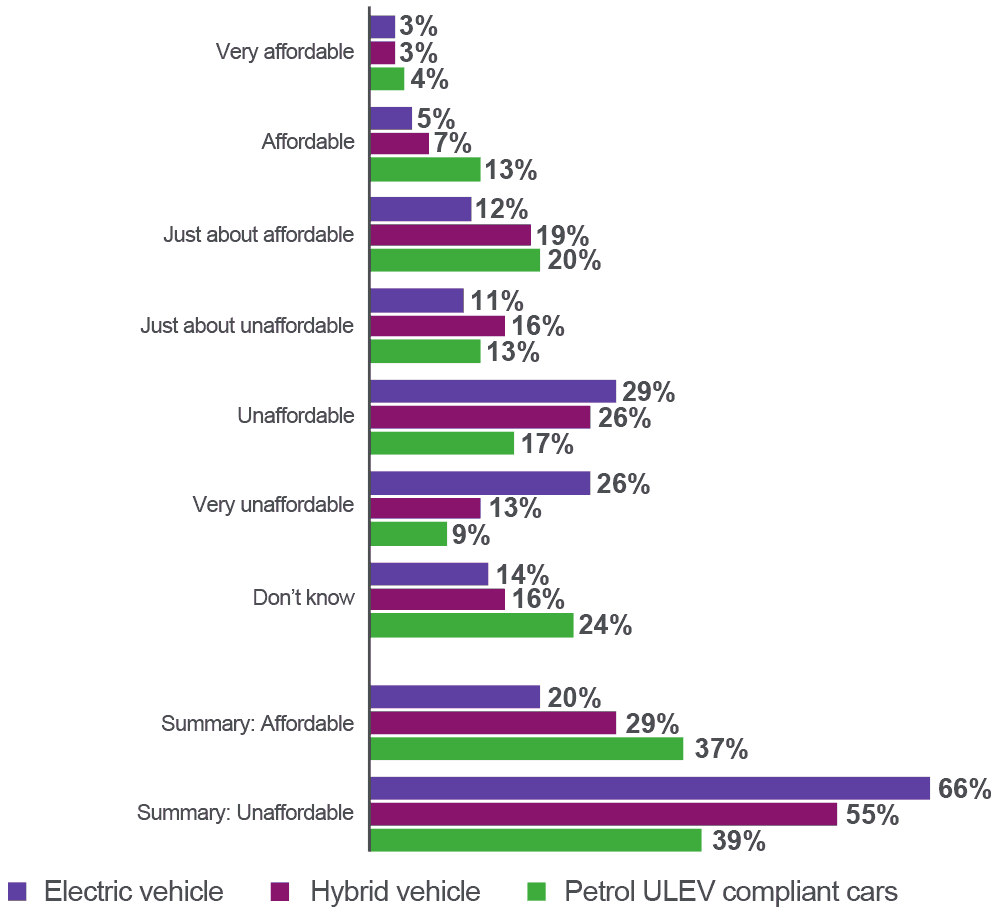

Looking at cost in more detail, there is a trend whereby the more fully electrical the car, the more likely it is to be perceived as unaffordable (39% petrol ULEV compliant, 55% hybrid and 66% electric). For petrol ULEV compliant cars, the proportion of Scots who say they are affordable is similar to the number who say they are unaffordable (37% and 39% respectively).

C06: If you were to buy a car or van in the next 12 months, what, if anything, about current ULEV vehicles would encourage you to buy one?

Unweighted base: 1,129

5.2 Public Transport

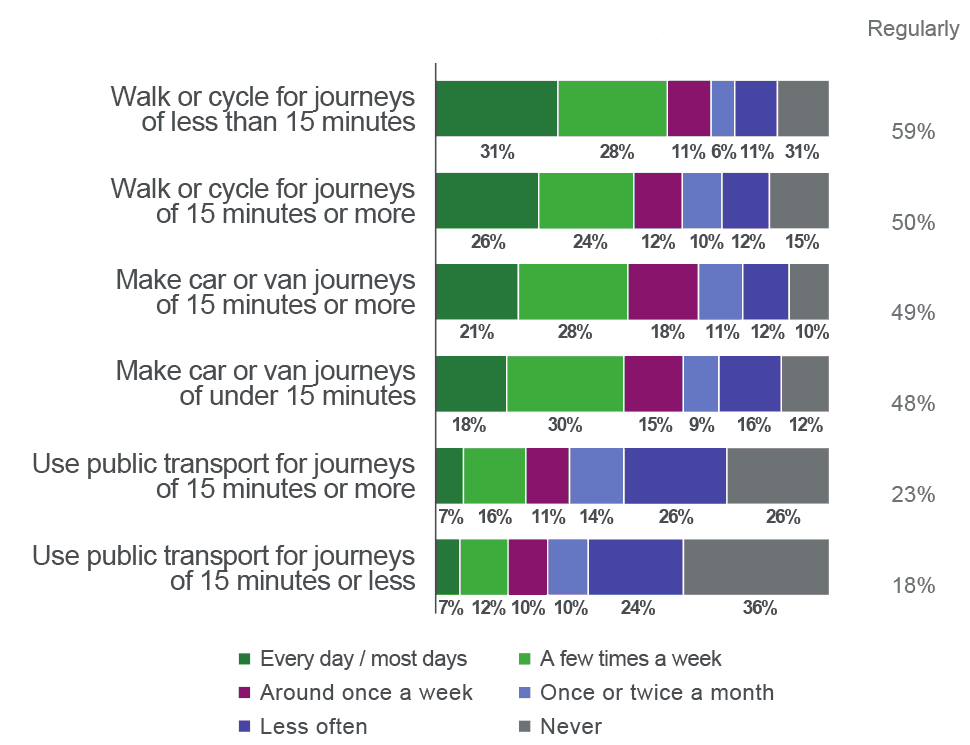

Almost half (48%) of Scots regularly make a car or van journey of under 15 minutes each week, while around one in five regularly make journeys by public transport for any length of time. Those aged 16 to 24 are generally more likely than average to undertake each type/length of journey, but this is particularly the case when it comes to their use of public transport, with 38% regularly making journeys of less than 15 minutes, and 45% making journeys of 15 minutes or more.

Among Scots who use public transport, 75% say they use the bus and 53% say they use the train. Bus use is higher among respondents aged 55 and over (86%) while the train is more popular among those aged 25-34 (62%) and 25-44 (62%).

Three in five (61%) of Scots do not have regular use of a bicycle, and this rises to 70% among women, and 79% of those aged 65 or over.

D01: Thinking about the type of journeys that you make in your day-to-day life (including for work). Generally, how often do you do the following?

Unweighted base: 1,520

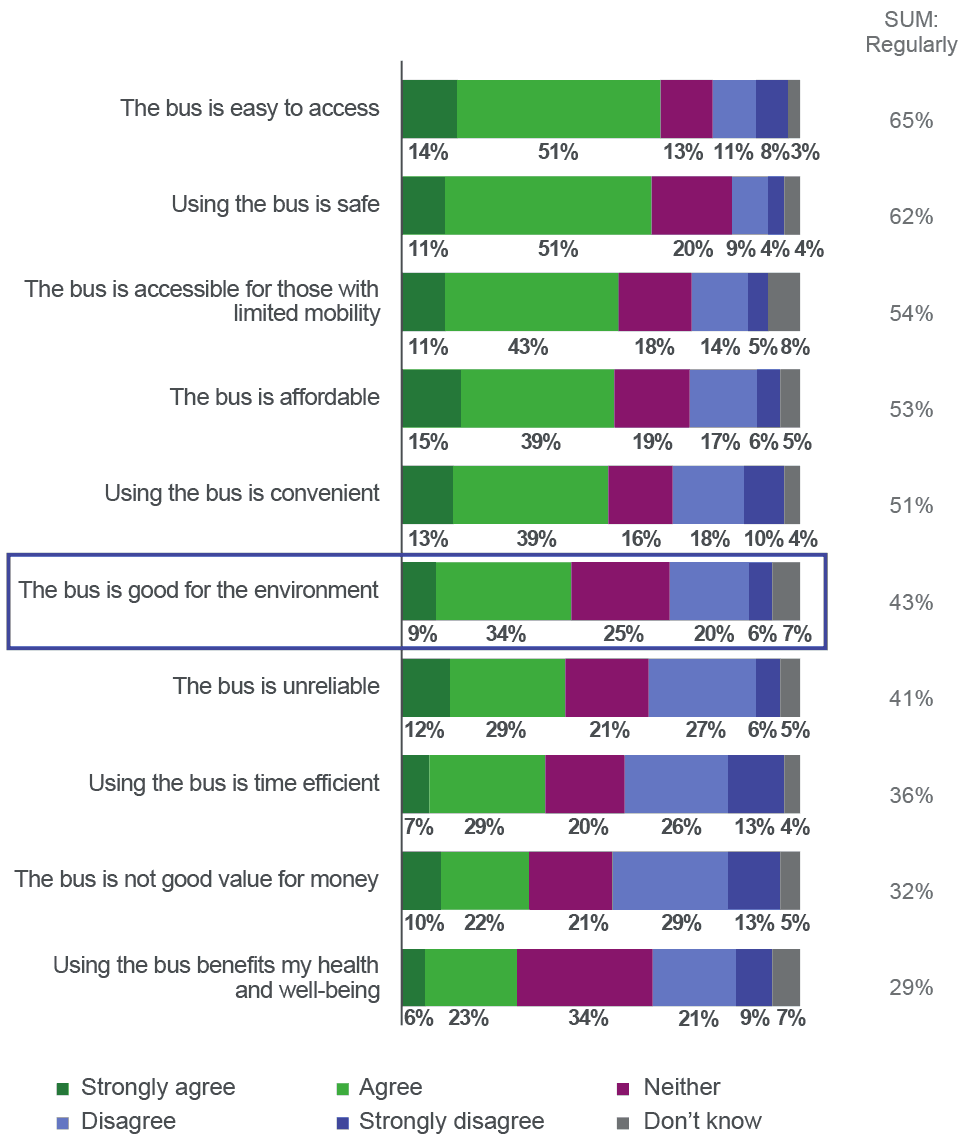

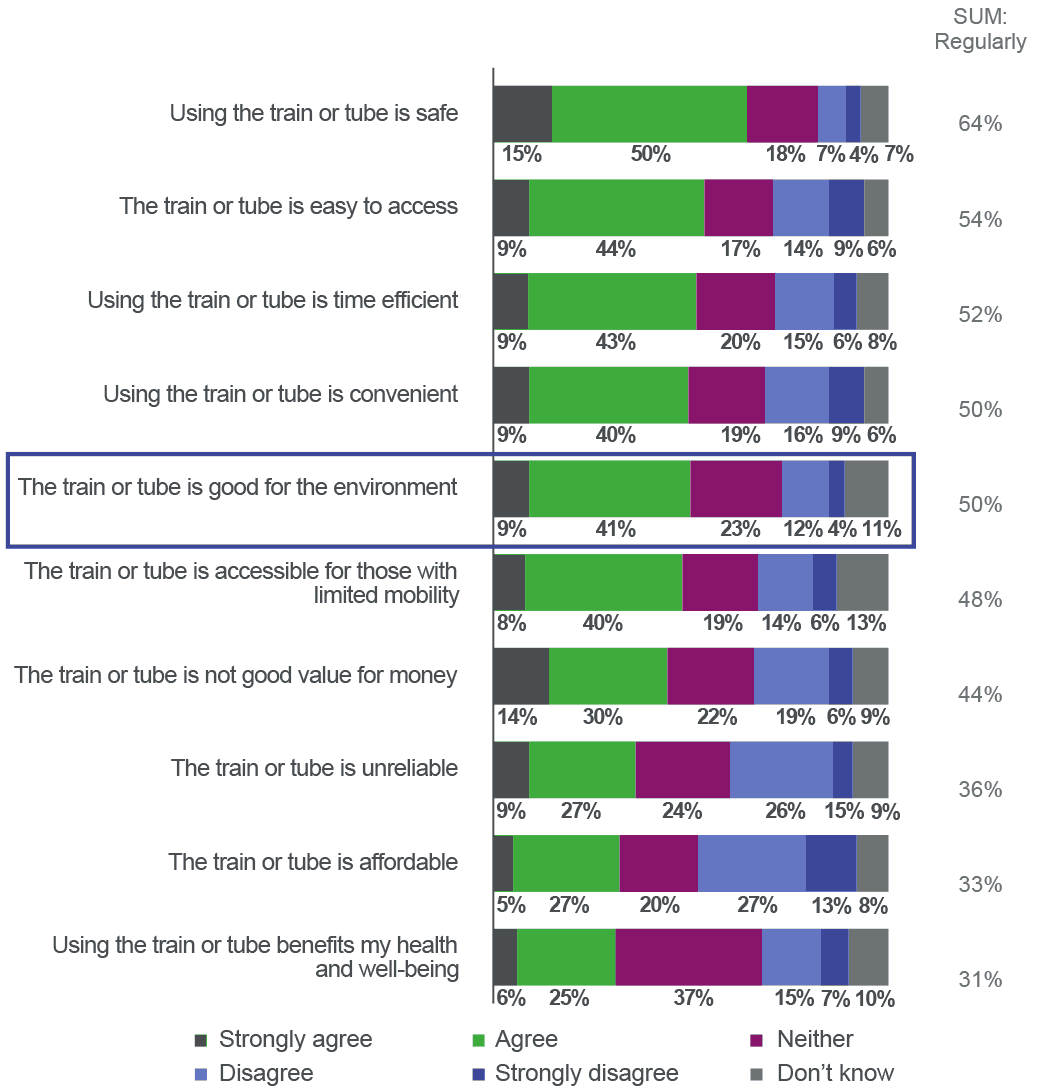

Across various dimensions, respondents rate buses and trains/tubes similarly. For example, similar proportions agree that buses and trains/tubes are safe (62% for buses, 64% for trains) and convenient (51% for buses, 50% for trains). The bus is seen as more affordable (53%) and more accessible (65%) than the train/tube. The train/tube, meanwhile, is seen as more time efficient (52%) and good for the environment (50%).

D04. Thinking about public transport, please indicate your agreement or disagreement with…?

Unweighted base: 1,520

When looking at these key considerations in the context of respondents who actually use the bus, we see that agreement that using the bus is good for the environment sits at 50%, but 67% agree that the bus is convenient and 64% say the bus is affordable. This suggests that where buses are being used, convenience and cost rank higher than environmental benefit as motivating factors.

The convenience and environmental benefit of using trains both rank equally high as considerations among all respondents (50%). The perception that trains are affordable drops to 32%.

D04. Thinking about public transport, please indicate your agreement or disagreement with…?

Unweighted base: 1,520

Among respondents who report using the train/tube, we see agreement that the train/tube is convenient rise to 68%, but the perception that the train is affordable drops to 43%. Concern for the environmental benefit of this form of travel sits at 61% which suggests that despite the perceived unaffordability of trains, their convenience motivates use more than the potential environmental benefits, and train users are still willing to pay for that convenience.

Contact

Email: Andrew.Taylor2@gov.scot