The Private Housing Rent Control (Exempt Property) (Scotland) Regulations 2026 - business and regulatory impact assessment

The business and regulatory impact assessment for The Private Housing Rent Control (Exempt Property) (Scotland) Regulations 2026.

Section 1: Background, aims and options

Background to policy issue

A good quality, affordable, and well-regulated housing system generates benefits that can help tackle poverty (including for families with children), promote equality, and support wellbeing.

Housing to 2040[4] set out a vision for what the Scottish Government wants homes and communities to look and feel like. It is a vision where homes are affordable for everyone, where standards are similar whether people rent or own their homes, where homes have easy access to green spaces and essential services and where homelessness, child poverty and fuel poverty have been eradicated.

The Scottish Government is of the view that further long-term changes to improve affordability, fairness and strengthen existing legislation are required to deliver our

vision for rented sector housing; in line with commitments made in Housing to 2040, the Bute House Agreement Shared Policy Programme[5] and the New Deal for Tenants Draft Rented Sector Strategy Consultation[6]. We therefore brought forward a range of measures for both the private and social rented sectors through the Housing (Scotland) Bill[7] (‘the Bill’) introduced in March 2024 which, among other measures, included powers for the introduction of a system of long term rent controls.

The Bill received Royal Assent in November 2025 and is now the Housing (Scotland) Act 2025[8]. It creates a power for Scottish Ministers to introduce rent control areas, following the assessment of rent levels by the local authority and after consultation with the relevant local authority and representatives of affected landlords and tenants. If the Scottish Ministers are satisfied, after reviewing this evidence, that capping rent increases for Private Residential Tenancies (PRTs) in an area is necessary and proportionate, that area may be designated as a rent control area through regulations that must be approved by the Scottish Parliament.

In any area where rent control applies, rent increases will be limited to CPI+1% point, up to a maximum of 6%. Rent increases for properties let under PRTs in rent control areas (other than exempt properties) would be limited to one rent increase per property per year, regardless of how many tenancies are granted by the landlord in that period. This means that the rent cap would apply to rent increases both during and between tenancies, to stabilise the level of rents within the area and avoid the potential for rents to continue to rise more steeply between tenancies.

Recognising the importance of making sure that the system of rent control is capable of balancing the interests of tenants with the property rights of landlords, in a way that recognises the important role that the supply of new rented housing plays in ensuring that rents are affordable, the Act includes a regulation-making power for the Scottish Ministers to specify types of property that will be exempt from rent control or other circumstances relating to the tenant or landlord where rent increases above the rent cap would be allowed.

Our engagement with stakeholders, both before and after the introduction of the Bill to parliament, brought forward concerns from investors and some providers of affordable accommodation, about the possible impacts of rent control on investment in BtR and MMR accommodation. These concerns were also raised in Parliament during the Bill’s parliamentary process.

In addition to the qualitative feedback, there is also quantitative data to support the proposition that investment in BtR has slowed during the period in which the rent control legislation has been developed. There are no official statistics on the level of BtR, which has not previously been a legally defined type of rented accommodation, but the British Property Federation publishes data on the number of BTR units based on the industry understanding of this term.

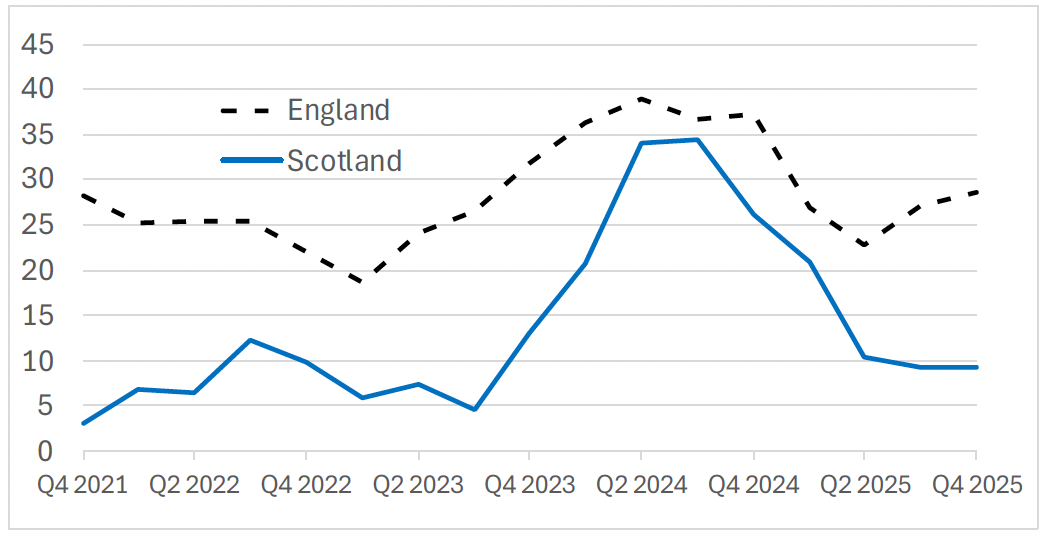

Chart 1 shows the annual change in completed BtR units. The completion rate in Scotland is compared to England, in order to control for cross-UK market and legislative factors which could have affected BtR trends. To facilitate this comparison, completions are expressed as BtR units completed per 100,000 people in each country. It should also be noted that the data, particularly in Scotland due its smaller size, is quite lumpy because a few large-scale projects can affect overall rates.

The data shows that while the BtR completion rate in Scotland, which had previously been significantly below England, approached the rate in England in mid-2024, it has subsequently fallen, and by more than the fall in England (with the fall in England also reversing in recent quarters).

Sources: BtR completions – British Property Federation, BtR quarterly reports; Population – ONS, Population estimates time series dataset.[9]

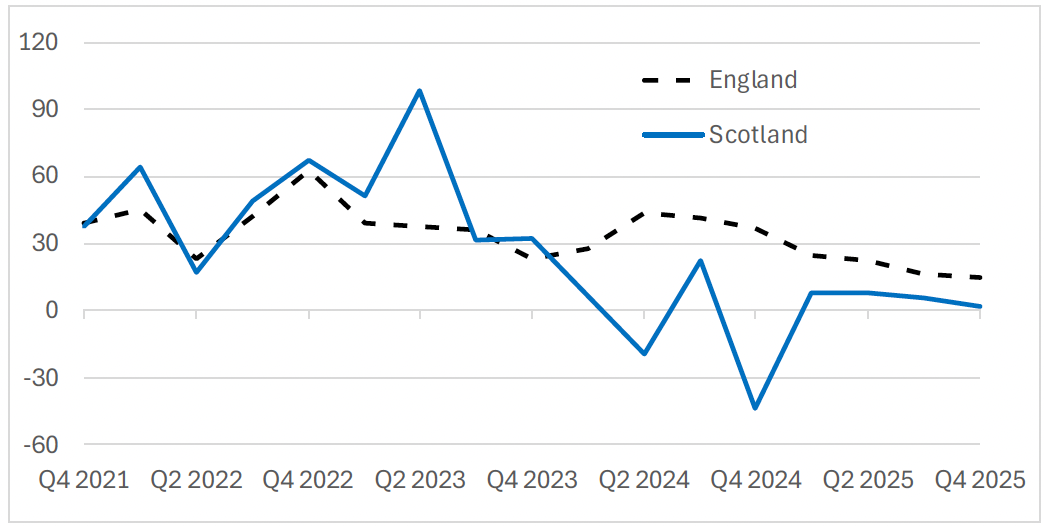

Due to the timescales involved in building BtR properties, completions shown in Chart 1 will be the result of decisions made in earlier years. Chart 2 uses the same data sources, but provides the annual rate of change in total units, again expressed per 100,000 people in each country. Total units include completed units, units under construction and units in the planning system. Unlike completions, the change in total units can be negative, for example, if BtR units are removed from the planning system before they start to be constructed (either completely or due to being switched to another use[10]). Chart 2 shows that on this basis the decline in total BtR units in Scotland began in mid-2023, earlier than the fall in completions. Since then, the BtR rate in Scotland has been below that in England, and even negative in certain quarters.

Sources: As per Chart 1.

Further, the BtR sector have made clear there is substantial untapped demand for build to rent property in Scotland, including in the recent industry publication “A new Dawn for Scottish Build to Rent” from November 2025. It is suggested that this untapped demand arises from prior demand and lack of development in Scotland influenced by prior policy positions, regulatory decisions and market conditions. This includes issues such as the development and implementation of the Private Rented Tenancy in Scotland (elements of which are now being developed in similar ways in other parts of the UK through UK Government action), the Covid period and post-pandemic inflation.

Prior Scottish Government policy approaches have sought to ameliorate these concerns and support growth, including through a Rental Income Guarantee Scheme (RIGS), called for by industry but never ultimately called upon.

Our engagement with stakeholders included the work of the Housing Investment Taskforce[11], which was set up in April 2024, to identify actions that will unlock both existing and new commitments to investment in housing across all tenures as part of our work to boost housing in Scotland. The Taskforce produced their report setting out these actions[12] on 9 June 2025, and this included a recommendation to exempt Build to Rent and Mid-Market Rent properties from rent control to support increased rental market housing supply, arguing this would support higher housing provision through private finance.

Scottish Government brought forward a consultation[13] on the potential use of the powers in the Bill to exempt properties from rent controls or to allow for rent increases above the rent cap in certain circumstances, which ran alongside Stage 2 of the Bill's parliamentary process. An interim partial analysis of the consultation[14] was published on 2 September 2025 to allow for early consideration of responses covering some of the issues that received most focus through Stage 2 of the Bill’s consideration by the Scottish Parliament. This included interim analysis of the responses to questions on possible exemptions from rent control, including the issue of whether BtR and MMR properties should be considered for exemption. (The final analysis report was subsequently published on 6 January 2026[15]).

In light of the potential barrier to investment in new rented housing and, as part of the actions to address the housing emergency, during stage 3 of the Bill’s passage through Parliament the Cabinet Secretary for Housing signalled the intention to introduce regulations to exempt, where appropriate, MMR and BtR properties from rent control measures, as soon as possible after the legislation received Royal Assent, in order to give certainty to the sector. This was influenced by the necessity to prioritise expanding housing stock in Scotland, acknowledging that exempting certain categories of property, where that is appropriate, will support supply in these sectors.

Purpose / aim of action and desired effect

Mid-market Rent

The Scottish Government recognises the important role housing providers play in offering properties at Mid-Market Rent (MMR). MMR homes are aimed at assisting people on low to moderate incomes to access affordable rented accommodation, in particular those who are unlikely to have priority for social rented housing, but who will have difficulty in buying their own home or renting privately on the open market. Tenants generally pay a lower rate than renting privately, but more than for local social housing. In order to make these sub-market rents financially viable, some form of public sector subsidy is generally required.

The Scottish Government is keen to see continued investment in this type of housing provision to grow the supply of good quality affordable rented property that offers choices for tenants.

The MMR model already incorporates controls on rent levels to ensure that they remain affordable to tenants. Tenants will receive the benefits of these protections throughout the period that they stay in the MMR property, whether or not a Rent Control Area has been designated.

For those properties receiving public support, the level of support provided is calibrated so that it is just enough to ensure that MMR projects remain financially viable while keeping rents at an affordable level. Adding further restrictions to rents might therefore either deter investment or require more public subsidy.

It should also be noted that the regulations propose that for a property to qualify for an MMR exemption, the rent cannot exceed the median rent in the BRMA in which the MMR unit is located. Therefore, if a significant part or all of the BRMA falls into a rent control area at any point, the median rent in the BRMA will tend to be reduced due to the operation of rent controls, and this will help to ensure that MMR tenants are not adversely affected due to their tenancies being exempt.

The analysis of responses to our recent consultation, which included questions on the potential use of the powers to exempt properties from rent control, set out some of the wider reasons which some respondents gave for supporting an exemption for MMR properties:

“‘Developer or investor’ and ‘Social landlord or their representative bodies’ respondents were amongst those highlighting the role of MMR in providing options and choices for those who cannot afford to rent privately in the open market or buy their own home. Respondents gave examples of those benefiting from MMR, including people relocating for work or leaving education and key workers such as teachers, care workers and NHS staff.

There was specific reference to rural areas where housing supply is limited, and it was noted that MMR homes can support local employment and sustainable communities, including by providing an option for younger people who wish to stay in communities where social housing options may be very limited or non-existent.”[16]

(More details on consultation and stakeholder engagement as a whole are covered later in this document).

Build to Rent

Investment stakeholders have consistently reported that the potential introduction of rent control areas has reduced investor confidence in the BtR sector, which builds homes for the rental market, as opposed to long-term home ownership. The financing of these units has certain distinctive elements.

Firstly, BtR developments require the developer to bear risk throughout the period of development, which can take a number of years. Development stages include identifying sites, putting together funding packages, submitting planning applications, waiting for planning applications to be decided, and undertaking construction of the units. BtR can therefore be distinguished from a landlord who buys a single new-build unit from a developer, since in this latter case the landlord will not have capital tied up for a number of years before they are able to start receiving returns.

Secondly, in contrast to homes built for home ownership, the return from capital invested in a BtR unit is not received as a single large payment on sale, but from a relatively smaller rental income stream over a long period of time. In other words, the risk for investor and developer is longer-term across the lifetime of operation as well as the development phase, in contrast to speculative development of homes for sale or developments where the risk is also taken in development phase and relies on early sale for capital receipt to repay finance and redeem investment in a (planned for) shorter period. The BtR, rather than capital sale, model therefore requires longer term investing and longer term holding of risk by the developer/operator or transfer of such risk from the developer to a purchasing operator if that is the model used.

The combination of these two elements means that BtR developers bear risk over a significant period of time, covering both the period of development and the period over which a rental stream has to be earned before the cost of development is fully recouped. As a result, concerns about the impact of potential controls on rents far into the future can have a significant impact on whether to proceed with investment in the present and the access to and desirability of investment over longer time periods, with consequent pricing decisions made by investors and developers which may make projects financially unviable.

Rent control therefore has the potential to disrupt this model of development, as the uncertainty in relation to investment returns makes it difficult to leverage the financial investment required for delivery. There are concerns that this could lead to a reduction in the volume of new homes being made available for rent unless action is taken.

Conversely, our engagement with stakeholders representing investors in housing suggests that encouraging investment in this sector has the potential to have significant positive impact on the supply of rented housing in the places we need - both in urban Scotland and in our rural and island communities.

Homes delivered under BtR models are likely to stay in the rental market for long periods of time, boosting the overall supply of rented homes. BtR can often quickly deliver substantial numbers of new rental homes into the housing market, which can boost supply and help to mitigate rental pressures and importantly do so from private capital investment, increasing housing stock overall without additional cost to Government.

Feedback from stakeholders, including local authorities, also indicates that new build BtR property can play an important role in providing quality rental accommodation important to attracting and retaining inward investors such as financial services companies and in the competitiveness of (primarily) Scottish cities relative to other cities in the UK.

Our engagement has suggested that BtR providers tend to be long-term focussed, often pension fund sponsored corporate landlords with a ‘for-rent only’ strategy, which could guarantee both long-term supply of BtR properties as well as the absence of a risk of evictions for personal use.

Turning to the academic literature, in a recent econometric study based on long-term data from 16 developed countries[17] Kholodilin & Kohl found that over the period since 1960, the impact of rent controls on housing construction was negative and statistically significant.[18] However, this finding was driven by countries with first-generation rent controls. The researchers also point to the fact that rent controls often exempt new construction from regulations as being one obvious explanation for why the impact of rent controls on construction is not larger, although they did not have sufficiently fine-grained data to test this directly.

As was set out in the BRIA for the Rented Secor Reform Measures in the Housing Bill, the approach taken by the Scottish Government falls into the category of second- or third-generation rent controls, since the controls will apply to rent increases and are indexed to inflation, as opposed to the nominal rent freezes typical of hard first-generation rent controls. Together with the proposed exemptions of BtR and MMR housing from rent controls, this should help ensure that the Scottish rent control system is similar to countries in the Kholodilin & Kohl dataset where rent controls did not result in significant negative impacts on housing construction.

The researchers also identify that a possible contributory factor to the impact of rent controls on construction being relatively weak is that construction might have been diverted from new rental housing into the home-owner market[19] or been accompanied by increased social housing provision (although this would require additional government funding).[20] While, to the extent that this is the case, the impact of rent controls on the housing system as a whole is smaller than on the rented system alone, the fact that the market would supply rented housing in a particular location in the absence of controls suggests there may not be as much demand for owner occupied housing as for rented housing in that location. The Scottish Government’s view is therefore that BtR plays an important role both in increasing the total quantity of housing and also in providing the appropriate tenure mix for a particular location.

We acknowledge that it is possible that permanent or long-term exemptions may exacerbate price differentials between older and newer stock and thus create perverse incentives for landlords to dispose of regulated stock prematurely, or potentially incentivise tenants to remain in properties that they might have otherwise exited. Our view is that importance of incentivising new supply outweighs the disadvantages of such effects. Furthermore, the characteristics of the rent control system set out in the Act (e.g. that it applies to rent increases rather than rent levels,[21] and that rent controls are not indefinite but only apply if the evidence base supports that a rent control area is required) should reduce the degree to which different segments of the market can diverge in this way, minimising unintended consequences.

Taking account of all of these factors, the Scottish Government recognises that there can be significant benefits from the provision of new build, or newly converted, rental property which increases the overall housing stock.

The Scottish Government is therefore keen to support and encourage investment in both the MMR and BtR sectors, with a view to increasing the supply of housing in the rented sector. Engagement with the Housing Investment Taskforce and with investment stakeholders more widely, has suggested that, whilst setting out an inflation-linked rent cap in the primary legislation may go some way to mitigating investor concerns, the application of an exemption from the rent cap in appropriate circumstances may be the minimum action needed to support further investment in these parts of the PRS.

Options (considered so far/ still open)

Option 1 – take no action.

Under this option, the rent control measures in the Act would be brought into force with no exemptions set out in regulations for MMR & BtR.

This would mean that, in any areas where rent controls were applied[22], all relevant properties would have a restriction on the amount by which the rent could be increased, limited to CPI+1% point, up to a maximum of 6%.

Whilst this would most directly impact properties in any designated rent control area, there could also be resultant impacts on investment in some parts of the PRS across Scotland, as set out above.

For these reasons, we do not consider that this option would provide sufficient reassurance to the sector to support the necessary provision of increased supply of new rented homes.

Option 2 – bring forward regulations to set out criteria for exemptions from rent control measures for MMR and BtR properties (preferred option)

Build to Rent

The overall aim of exempting this category of property is to remove the potential barrier to investment in purpose-built homes for rent, which rent controls represent, and to promote the retention of these properties in the private rented sector. The proposed exemption is designed to cover the types of commercial developments of residential property which were most affected by reduced investment following the announcement of rent control in August 2021.

In order to target the developments which could have seen a reduction in funding following the announcement of rent control, the exemption is applied to properties constructed after the date of the announcement. This is designed to promote future investment in new purpose-built homes for rent and to promote the retention of those BtR developments already constructed, and which may have seen a reduction in funding, in the private rented sector.

In order to target these types of commercial developments of residential rented property, the exemption applies to groups of 6 or more properties covered by the same planning permission and all owned by one person or one group of persons. This reflects the status given to transactions of 6 or more residential properties for the purposes of Land and Buildings Transaction Tax (LBTT). Section 59 (8) of the Land and Buildings Transaction Tax (Scotland) Act 2013 provides that, in relation to those transactions, those properties are treated as not being residential property. Non-residential property transactions are taxed differently than residential property transactions for the purposes of LBTT.

The Regulations provide that the BtR exemption will cease to have effect where the nature or use of the property is changed. For example, the exemption will cease where the property is owner-occupied or used as a short term let. These restrictions on the exemption in regulation 4(2) are designed to promote the retention of Build to Rent properties in the private rented sector – the loss of the exemption acting as a deterrent against removing the property from the private rented sector.

Mid-market Rent (MMR)

This proposed exemption recognises that properties already have some form of contractual restriction on rent increases based on a variety of different measures of affordability. A form of control on rents already exists and layering additional rent control measures could create unnecessary complexity for providers without offering further benefit to tenants. The exemption is designed to apply where there is a restriction included in such funding, placed either directly or indirectly on the landlord. Properties provided via direct public funding will operate where conditions directly prevent the landlord from raising the rents above a specified level.

As this type of funding for properties can be provided to a registered social landlord who offers those properties for rent via a holding company or subsidiary company (Registered Social Landlords cannot be the landlord in a private residential tenancy), Regulation 5(3) captures these arrangements by applying the exemption where funding is provided to someone other than the landlord and the landlord is indirectly prevented from raising the rent above a certain level.

It is acknowledged that properties can be provided by persons who do not receive public funding but keep rents below a certain level. The Regulations cater for these circumstances by applying the exemption to circumstances where the landlord contractually restricts themselves from raising the rent above a specified level via the terms of the tenancy.

The Regulations set out a specified level above which the rent cannot be raised as the median of broad rent market area values as this reflects the restrictions on rent increases which are found in conditions for the provision of properties which are funded by the Scottish Government. This specified level above which rents cannot be raised applies to all forms of properties that are seeking to be exempt from rent control as a property, whether publicly funded or not. The requirement that the rent must not be raised above the specified level, separate from the required restrictions on raising the rent, ensures that the exemption will no longer apply if the restrictions on rent increase are ignored and the rent is raised above the specified level.

Laying regulations which define the criteria under which properties will be exempt from rent control will give confidence to investors and developers that a stable rental income stream will still be achievable over time for properties which meet the criteria, even if a rent control area is subsequently designated in the area where those properties are built.

The criteria have been designed to support and encourage investment in either:

- developments of multiple properties, which increase the supply of properties which will remain in the rented sector, or

- properties which will have restrictions on the level of rent which can be charged for the property.

Properties which fall under these criteria will represent a long-term increase in the supply of rented housing, which the Scottish Government is keen to encourage, particularly in light of the current housing emergency, and for this reason, we consider that it is most appropriate to pursue Option 2.

Sectors / Groups affected

The Scottish Government considers that the sectors or groups affected by the proposed measures would include:

- Landlords, including housing association and local authority subsidiaries who let property in the PRS

- Investors and developers

- Tenants

The existing rent control measures will affect all PRS landlords with a property within a rent control area, unless these are exempt properties under the criteria set out in these proposals.

Landlords

Landlords with properties within a rent control area which are defined as exempt under these proposals will not be directly impacted by the rent cap, but there are likely to be some administrative impacts on these landlords. The Act includes a power for the Scottish Ministers to set out a process by which a property is confirmed as an exempt property. The intention is that the details of this will be set out in future regulations, but this may involve an approval process or some form of inclusion in a register. The intention is that this process will give tenants and prospective tenants confidence in the system.

While there is no official estimate on the size of the MMR sector,[23] some idea of scale can be given for MMR which is funded by the Scottish Government. Over the period from 2000-01 to 2024-25, 14,314 MMR properties have been delivered through the Affordable Housing Supply Programme.[24] It should be noted that this does not mean that the total stock of Scottish Government funded MMR units is currently 14,314, as this figure does not include any units completed prior to this date or which were not funded by the Scottish Government, and it does not exclude units which have left the MMR sector since they were first delivered.[25]

The trends within this time period are also of interest: over the period from 2000-01 to 2011-12, an annual average of 49 units was delivered, while over the period from 2012-13 to 2024-25, an annual average of 1,056 units was delivered. This illustrates the increasing importance of MMR as part of the Affordable Housing Supply Programme, with the share in 2024-25 standing at 16%. 89% of MMR units funded through the Affordable Housing Supply Programme have been new build.

The Scottish Government recently published a report on the analysis of the characteristics of MMR providers and tenants[26], although it should be noted that this was a voluntary survey, and that no attempt has been made to weight or scale up the data to make it representative of the MMR sector as a whole.

This report included survey results suggesting that, among the MMR providers who responded, the highest number of MMR properties were located in the Edinburgh local authority area (49%), followed by Glasgow (16%), and Aberdeen City (11%). For the MMR tenants who responded, there was a similar pattern in terms of the properties they lived in.

As BtR is not currently legally defined or categorised under planning legislation, there are no official statistics on the size of this sector.

However, there are some existing private estimates that indicate that this is a small but potentially growing sector. Figures published by the British Property Federation[27] estimated that by Quarter 3 of 2025 there were around 4,218 complete units in Scotland, with 1,932 under construction and 11,001 at the planning stage.

Section 17D (3) of the 2016 Act, inserted by the Housing (Scotland) Act 2025, gives Scottish Ministers the power to introduce a process whereby landlords are required to confirm the property meets the description of an exempt property by making an application to a specified body. Over time, this will help build up our understanding of the extent of BtR properties across Scotland.

Landlords with properties in a rent control area which are not exempt from the rent cap will remain subject to the rent controls set out in the Act, although as set out elsewhere in this document, the Scottish Government is also considering circumstances where it may be appropriate for a rent increase above the rent cap to be permitted in specific circumstances, in order to prevent some landlords being disproportionately affected where a rent cap is applied.

The analysis of responses to the Scottish Government’s recent consultation includes a summary of reasons given by respondents who are not in support of an exemption for BtR properties. The views expressed by some respondents, particularly ‘Private landlord, letting agent or their representative bodies’ and ‘Individual’ respondents, include concerns about possible negative impacts on some landlords:

“...granting an exemption for (predominantly) large professional BtR landlords operating in one part of the private rented sector will create a two-tier system that unfairly disadvantages the (often) small private landlords whose properties would be subject to rent controls.

This was also expressed as giving new build BtR an unfair advantage over existing rental stock and was linked to an argument that an exemption for BtR could encourage private landlords to divest existing stock and invest in new BtR properties.”[28]

The Scottish Government acknowledges these concerns, and is keen to ensure that individual private landlords in the PRS are not disproportionately impacted by the rent control measures in the legislation. Further engagement with the sector will be necessary as part of the assessment of possible impacts as the policy in relation to potential rent increases above the rent cap is developed further.

Investors and Developers

As set out above, the Scottish Government considers that these proposed regulations will give greater confidence to investors and developers who operate in the MMR and BtR sectors that rents over the longer term will offer a viable return on investment, which may increase their confidence in investing in the rented sector in Scotland.

Tenants

There are likely to be impacts on tenants who are living in properties which are exempt under proposed regulations. The rent cap set out in the Act is intended to provide predictability and protection for tenants, limiting more significant rent increases and helping renters at times when inflation spikes. Over time, the cap should also help limit rent inflation, especially during periods of high general inflation. As the rent cap will not be applied to rent increases in exempt properties, tenants in BtR properties in particular may see higher rent increases than tenants in properties where the rent increases remain capped. However, tenants in properties which are exempt from rent controls will have access to the existing rent adjudication process, which will allow them to challenge a rent increase which they consider to be unreasonable in relation to market rents for comparable properties in the area.

Furthermore, in the absence of the exemption, it is anticipated that there would reduced appetite for investment in new, purpose-built rented housing in Scotland with the implications on the potential to increase the supply of properties made available for rent through this route. In this scenario, tenants could have less choice of accommodation options and there could be a risk of pushing up rents across the wider rental market.

Tenants in MMR properties

The analysis of the recent consultation summarised reasons given by respondents who are not in support of an exemption for MMR properties, which speak to concerns about potential negative impacts on tenants, setting out that ‘Campaign’ respondents were amongst those commenting that:

“...while MMR properties should be affordable to people on low incomes, this is increasingly not the case; they suggested that MMR developments should be rent controlled to ensure that they provide affordable housing. It was suggested that people may already struggle to afford the current level of MMR rents, and that exempting these properties may lead to affordability issues for existing tenants and make the sector unaffordable for others.”[29]

Some consultation responses referred to cases where MMR tenants experienced rent increases which represented a percentage increase above that which would be allowed in a rent control area under the Act.

The consultation analysis also summarised practical matters which were raised:

“Another frequently raised concern was that there is no accountability mechanism for MMR landlords as, although often subsidiaries of a Registered Social Landlord (RSL), they do not fall directly under the auspices of the Scottish Housing Regulator (SHR). An associated concern was that, as MMR rents are below market level, exempting MMR properties from rent control would leave MMR tenants without a mechanism to challenge rent increases.”[30]

Scottish Government monitoring data for 2020-2025[31] shows that, of those who responded:[32]

- 98% said that the rent being affordable was a very or quite important reason for choosing their property

- 67% said their previous home being unsuitable was a very or quite important reason for choosing their property

Of those who responded, 60% stated that they were previously renting from a private landlord. Whilst the majority were not on a housing waiting list, 29% were. 63% of tenants who responded had a gross household income of less than £35,000.

For tenants in MMR[33] properties which would be exempt under these proposals, under the criteria set out in the regulations, there would already be a restriction on the provider in terms of the level of rent increases which they are permitted to apply. This must be set out, for example, in the funding conditions set by the Scottish Government or the tenancy agreement, which means that their rents are likely to remain below market rents for the area. This protection applies throughout the life of a MMR tenancy, whether or not a rent control area has been designated.

It should also be noted that the regulations propose that for a property to qualify for an MMR exemption the rent cannot exceed the median rent in the BRMA in which the MMR unit is located. Therefore, if a significant part or all of the BRMA falls into a rent control area at any point, the median rent in the BRMA will tend to be reduced due to the operation of rent controls, and this will help to ensure that MMR tenants are not adversely affected due to their tenancies being exempt.

In the absence of the exemption, stakeholder concerns suggest some development of MMR properties may not proceed (as per the consultation response quoted in the section on ‘Investment’, below) and tenants on low and moderate incomes will have less opportunity to access this form of affordable housing.

The Scottish Government’s view is that for MMR properties, making the exemption available only where there is an existing restriction on the level by which rents can be increased and where rents do not exceed the median of market rent levels for that size of property in that Broad Rental Market Area, provides protection to tenants, while maintaining the financial conditions for continued investment in this important form of affordable housing. Investment in new supply MMR will also help to reduce pressure on rents across the private rented sector more generally, and thus potentially benefit tenants even if they don’t live in an MMR property.

Tenants in BtR properties

There is not a great deal of data available on tenants who live specifically in BtR properties in Scotland, although a recent report by British Property Federation (BPF), Association for Rental Living (ARL) and BusinessLDN has suggested that ‘renters in BtR are often not materially different from those in the wider Private Rental Sector in terms of age, average incomes, or household types’[34].

The analysis of the recent consultation summarised reasons given by respondents who are not in support of an exemption for BtR properties, which speak to concerns about potential negative impacts on tenants:

“A frequently made point, including by ‘Campaign’ and ‘Tenant, community group or union’ respondents, was that rent controls should be applied consistently across all types of privately rented property, including BtR. Points made in relation to BtR specifically included that some tenants might not know they are renting in a BtR property and, by extension, that they would not be protected by any local rent cap that might apply.

‘Local authority’ respondents were among those raising concerns in relation to the affordability of rental properties in the BtR sector, with reports that rents are already high, and that BtR rents above average can impact BRMA and LHA levels.

There was also a view that an exemption could encourage developers to prioritise the luxury end of the market, especially in urban areas, at a time when many BtR properties are already unaffordable for people on low incomes, including older people. It was argued that rents in the BtR sector should be brought down rather than introducing measures that could have the opposite effect.”[35]

The analysis also drew out reasons why respondents supported an exemption for BtR properties, some of which speak to potential positive impacts on tenants:

“Arguments in support of an exemption were made primarily by ‘Developer or investor’ and ‘Private landlord, letting agent or their representative bodies’ respondents, although there was also support from some ‘Local authority’, ‘Professional or representative body’, ‘Social landlord or their representative bodies’ and ‘Individual’ respondents. Reasons given included that the BtR sector has the potential to deliver new homes at scale to help address unmet demand for housing.

It was also suggested that BtR developments typically provide high quality, professionally managed homes on longer tenancies, often with on-site services that benefit tenants, and that the model provides choice for tenants and depends on resident satisfaction, rather than short-term profit.”[36]

In taking forward these proposals, the Scottish Government acknowledges that BtR tenants will not have the same protections as tenants in non-exempt properties, but believes that this is outweighed by the benefits of encouraging greater investment in new-build properties. Increased supply will give tenants more accommodation options to choose from, and will also help to reduce overall market rents relative to what they would have been without such investment.

Tenants in BtR properties, like all tenants in properties which are exempt from rent controls or not in a rent control area, will have access to the rent adjudication process which will allow them to challenge proposed rent increases they consider to be unreasonable. Section 25 of the Act[37] includes a change to the way rent adjudication for private residential tenancies is determined, to ensure that the rent set cannot be higher than the rent proposed by the landlord in the rent increase notice. It is hoped that once this measure is brought into force, it will remove any disincentive to tenants from making use of their right to refer a rent increase for independent adjudication, and encourage use of the rent adjudication process in cases where tenants consider a proposed rent increase to be unreasonable.