Pathways: A new approach for women in entrepreneurship

An independent review into women in entrepreneurship in Scotland, authored by Ana Stewart and Mark Logan. Based on thorough data analysis and stakeholder engagement the report's recommendations seek to address the root causes of female under-participation in entrepreneurship.

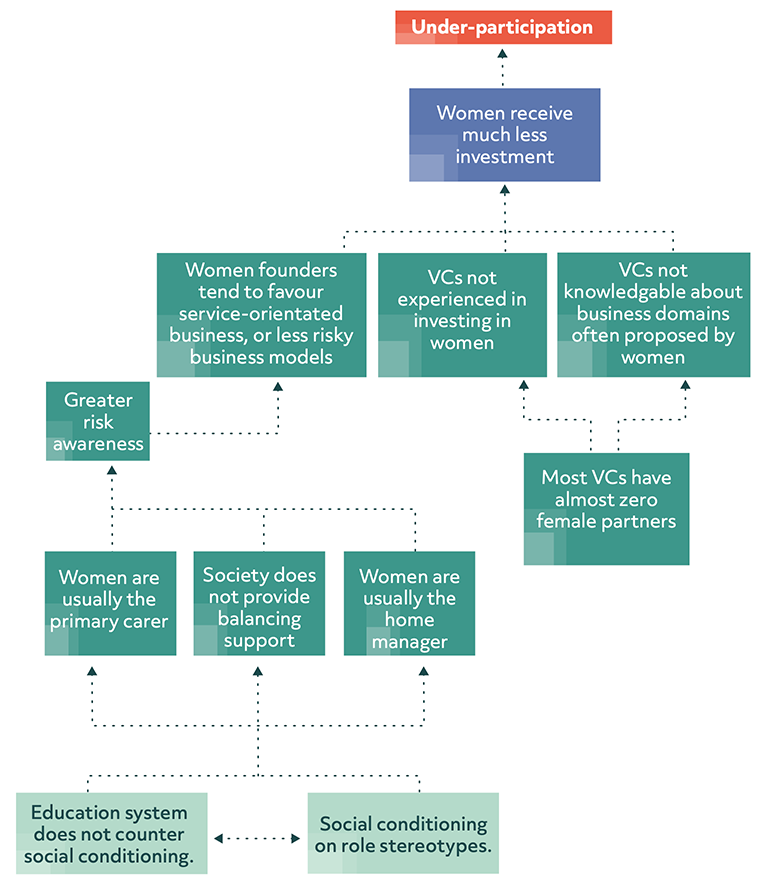

08. Women receive far less investment than men

"I did 119 pitches to VCs, mostly in London. I met only two women during these pitches...". - Rachel Jones, Founder & CEO, Snapdragon

In this chapter, we explore the following proximate cause of female under-participation in entrepreneurship:

Women receive far less investment than men from venture capital firms, syndicates and related sources.

This proximate cause is ultimately established by the same two root causes already examined in the previous analyses[74]. Recapping, from the earliest age, we experience intensive societal conditioning on what constitutes "normal" gender roles. And the education programmes – from birth to adulthood – required to intensively counter and correct this conditioning, are largely absent from our society.

In the context of our present focal area, these root causes together result in an investment industry where the overwhelming majority of venture capital (VC) and syndicate partners are male[75].

In theory, it need not follow that VCs therefore aren't knowledgeable or comfortable about investing in domains often proposed by female founders, but in practice it frequently does. As a result, potentially large opportunities in, for example, women's health (often referred to as Femtech[76]) are under-invested in relative to the market opportunity[77].

"Mention the words menopause or period app and see how quickly the room empties". - Entrepreneur, interviewee

The combination of this issue and the general existing sparsity of female founders means that investing in such founders is not the norm[78] and therefore appears to be riskier in the absence of a high number of successful prior exemplar investments.

Another factor acting to limit investment in women is a consequence of our discussion in Chapter 4 concerning the logistical constraints placed on women as a result of, on average, acting as both the home manager and primary carer. These burdens, in the absence of mitigating support, genuinely make investing in women riskier, because women in these roles have more demands on their time and energy. Further, they tend to guide women to less risky business propositions, which also carry a lower likelihood of outsized returns. Such an investment category is less attractive to investment firms, whose business model typically involves investing in a portfolio of businesses in which each has the potential to deliver a greater than 10X return. This does not equate to the category not being valuable to the economy, simply that the propositions are less aligned to the standard business model of venture capital firms[79].

"Private equity and venture capital is making progress, but a lot more needs to be done to attract, retain and develop female talent, including for senior investment roles. This will improve our industry in terms of performance, impact and culture, as well as benefitting the companies we invest in." - Calum Paterson, Managing Partner, Scottish Equity Partners

We can summarise the cause-and-effect relationships between these various mechanisms as follows (reading from bottom to top):

Addressing the Causes

We have already discussed, in Chapter 4, an approach that could start to address the underlying root causes identified above, we'll therefore focus here on actions that mitigate the issues resulting from them. In summary, from our diagram above, these are:

- Most investment firms have very few female senior investment staff, leading to an ignorance about domains often favoured by female founders, and an unfamiliarity in investing women.

- Female founders frequently present business ideas that don't match the typical investment targets of investment firms.

As we have seen from the cause-and-effect tree presented above, investment partners often lack sufficient knowledge of domains presented by female founders, which reduces the likelihood of them investing. The rarity of such investment also leads to a negative feedback loop being established: investing in women feels riskier because it is uncommon, which prolongs the rarity of investing in female founders, and so on. Morgan Stanley describe this as 'The trillion dolar blind spot', while the majority of investors perceive the funding landscape as balanced, their actual investments in multi-cultural and women-owned businesses is highly skewed[80].

The Investing in Women Code[81] is helpful to our general goals because it requires signatory companies to publish their investment demographics with respect to gender and to bring more focus to such demographics within their businesses. The most recent (2022) annual report[82] on the progress of signatories to the code shows modest performance improvements from the baseline year, 2019, though it is still too early to declare these to be a trend, especially with the arrival of Covid-19 in the middle of this sample period. The scheme is, of course, entirely voluntary, so it is not clear how non-signatories have performed over the same period.

Going beyond the Investing in Women Code, we believe that the best way to improve the investment balance is for investment firms to appoint more women as partners, and for government to create an incentive for them to do so.

The Scottish Government through its enterprise agencies and other investment channels, frequently invests alongside private investment organisations, such as venture capital firms and investment syndicates. We recommend that co-investment formally becomes contingent on participating investors having minimum levels of women employees in senior investment roles[83], subject to a grace period and specific conditions. The same should apply to fund managers where the Scottish Government invests as a limited partner.

"We must ensure that those who have historically been excluded, such as racialised women entrepreneurs, have a seat at the table in systems change, otherwise encoded bias will continue." - Pheona Matovu, Founder, Radiant & Brighter

Specifically, and to allow adaptation time, a grace period for this requirement should be instigated as follows: Enterprise agencies will only co-invest with private investment firms on the basis that at least half of the other entities participating in the investment round have at least 20% female partners within five years of the date of publication of this report. And, within 18 months of the publication of this report, participating investment firms must publish a plan indicating how they intend to reach this goal, if they wish to continue to participate in co-investment rounds.

We also recommend that, where organisations such as Scottish National Investment Bank (SNIB) acts as a Limited Partner to "cornerstone" a fund, such participation should be contingent on the fund manager having at least 20% of its senior investment personnel being women .

Again, to allow adaptation time, a grace period for this requirement should be instigated, requiring that this target be met within five years of the publication date of this report.

"We need to recognise that where we are today is simply not good enough and that setting the bar higher is essential if we are to see meaningful and accelerated change in diversity within the investment community." - Malcolm Kpedekpo, Co-Founder Panoramic Growth Equity

Would such an approach improve outcomes for female founders? Evidence from the investment/awards initiatives Scottish EDGE[84] and Converge Challenge[85] demonstrates that, as a result of efforts to diversify judging panels, selection candidate pools, finalists and winners have become more diverse, particularly in mixed-gender founder groups.

We also recommend, in the shorter term, that whilst outcomes from other root cause interventions filter through to become established practice, that co-investment models operated by Scotland's enterprise agencies, routinely invest a greater amount in start-ups with at least one female founder[86].

Specifically

VC/Syndicate investment: 50% (the baseline amount).

Co-Investment: Matches baseline amount plus '20% of baseline amount'.

For example:

VC/Syndicate investment: £100,000

Co-investment: £100,000

Female Founder Increment: £20,000

Different implementations exist as to specifically to achieve this outcome, which we leave as a matter for enterprise agencies to decide.

Earlier, in Chapter 4, we introduced the Concept Fund, available within the Pre-starts network to provide easy-to-access micro-grants to support very early-stage founders and pre-founders in testing – and gaining experience in testing - concepts.

A critical drop off in female entrepreneurs occurs from the nascent concept stage through the pre- and scaling start-up stages. This is evidenced in the low number of women-led start-ups receiving funding from syndicates and other finance sources. For example, angel syndicates interviewed for this review stated that, on average, less than 15% of the pitches they received came from women-led businesses. Even when turning to so-called friends-and-family funding, only 14% of women-led businesses receive funding from this source compared to 65% of male-led businesses[87] (a factor of five times less).

This situation is exacerbated by existing background factors such as the current phenomenon of angel capital migrating from earlier to relatively later stage investments, and the on-going poor availability of traditional debt funding facilities to early stage, high-risk start-ups.

"We need to overshoot on our diversity targets if we are to have any chance of achieving longer term equity." - Tim Allan, Founder, Tricorn Capital

"The investment landscape is generally skewed to a narrow demographic. There needs to be a concerted effort to drive changed behaviour here by adapting investment policies that promote a more diverse entrepreneur population." - Jenny Tooth, Chair UKBAA

Given this later-stage sparsity in investment available to female founders, a meaningful intervention here has the potential to be transformative. This is the rationale for the introduction of the Journey Fund, a companion fund to the Concept Fund.

The Journey Fund is designed to support under-represented founders whose business ideas are more developed than during the Concept Fund stage. The Journey Fund would make grants to qualifying founders in these under-represented demographics of up to £50,000. The intention is to provide a greater runway for product concept development and business growth readiness before requiring access to private funding.

We expect that this fund would be operated by Scotland's enterprise agencies in partnership with Scotland's private investment sector[88]. It would act as a springboard for promising early-stage start-ups as their businesses move into the more traditional investment ecosystem.

Initiatives of this nature, currently deployed in other territories such as Northern Ireland, demonstrate the viability and impact of such a fund[89]. In this example, 85% of women-led businesses that received this early-stage grant went on to successfully secured angel funding.

Multiple pathways could exist towards the Journey Fund. For example, one such pathway would be where the operator of the Pre-starts network determines that a start-up within its network is ready for Journey Fund consideration, which essentially signifies that the start-up has potential longer-term viability or scale-up potential. At this point, the start-up may enter the Scaler network or may take a different path. The grant is available in either case. Note also that the criteria for awarding this grant do not include that the start-up must demonstrate the potential for a 10X or greater return on investment.

These two grants, the Concept and Journey Funds, working in tandem, will increase female start-up participation. This, in turn, will increase the pipeline of founders successfully scaling their businesses and, consequently, will accelerate their participation rates across all later development stages.

Finally, we recommend that Scotland act strategically to establish the country as a global centre for Femtech[90] start-ups. Femtech start-ups exhibit both female and male founders, with a skew towards the former. The fund would support start-ups with high growth potential. Therefore, such an approach, if successful, would not only enable Scotland to exploit a market with vast potential - an estimated $50bn globally[91], it would also help to normalise investment in female founders. Moreover, this focal area continues Scotland's proud heritage as a leader in life sciences and healthcare innovation. With Femtech, this leadership takes the form of recognising that the vast majority of existing medical research and development activity significantly under-focuses on women's health[92].

Accordingly, the government should leverage ecosystem assets under its influence in a coordinated fashion to encourage Femtech start-ups to locate in the country, and to encourage investment in them.

"If we want to address the acute gender imbalance that exists in the finance and growth capital environment, we should encourage more women into technology-based businesses, which have the potential to become high-growth enterprises." - Anne Boden, CEO & Founder, Starling Bank

For example, the Scottish National Investment Bank should cornerstone a Femtech fund, the Scaler network should establish a Femtech specialisation within the network, and the Scottish Technology Ecosystem Fund should allocate a portion of its budget to supporting Femtech events.

"Investing in women is not a charity nor a philanthropic endeavour. Frankly, it makes good business sense." - Priya Oberoi, Founder Goddess Gaia Ventures

The above proposals are presented as specific recommendations in Chapter 10 : Consolidated Recommendations.

Contact

Email: EIDEEBSPEnquires@gov.scot