Publication - Research and analysis

Monthly economic brief: March 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Economic outlook

Forecasts expect a shallow recession in 2023 as the inflation rate falls sharply.

- Economic growth stalled through the majority of 2022, and although latest outturn data estimates that output has been more resilient than previously forecast, the growth outlook for 2023 remains extremely challenging as households and business continue to face significant cost of living pressures, despite expectations that the inflation rate will fall sharply over the year.

- Forecasts from the start of this year point to a shallow recession in 2023. In February, the Bank of England forecast the UK economy to remain in recession from Q1 2023 through to Q1 2024 with UK GDP forecast to fall 0.5% in 2023 and 0.25% in 2024.[18] This reflects a notably shallower fall in output than their November forecast, reflecting resilience in the labour market, and the rapid decline in the contribution of energy to inflationary pressures.

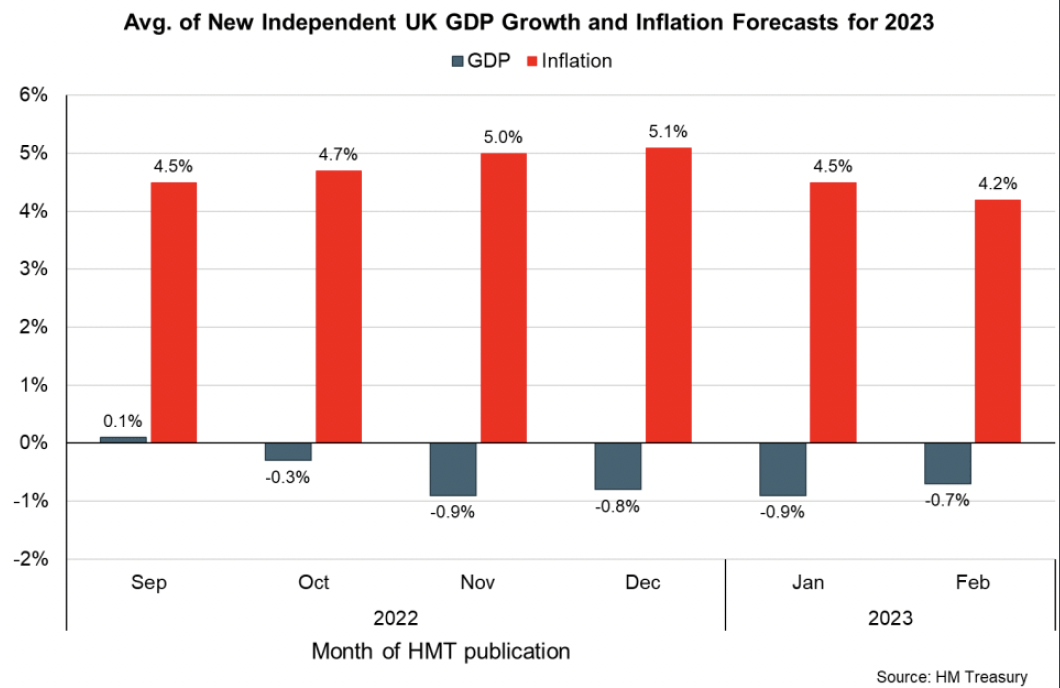

- More broadly, the average of new independent forecasts published by HMT in February indicates a contraction of 0.7% in UK GDP in 2023, which is also shallower than in recent months.[19] Alongside the fall in output, the Bank of England forecast inflation to fall to around 4% by the end of 2023. This is broadly in line with the average of independent forecasts (4.2%) which includes estimates of notably slower and more rapid falls in inflation over the year, reflecting the uncertainty and inflationary risks that persist in the outlook.

- At a Scotland level, latest forecasts in February from the Fraser of Allander Institute forecast three quarters of falling output in 2023 with output contracting 1% over the year as a whole, while EY forecast Scotland's GVA to fall 0.6% in 2023, in line with the UK as a whole.[20],[21]

- There is significant uncertainty over the depth and duration of the forecast recession, the pace at which inflation will fall back towards the 2% target, and the pace at which output will return to pre-recession peaks. This will reflect domestic and global economic developments, the impacts of fiscal and monetary policy and the persistence of the current energy supply and price shock.

- Cost of living pressures will remain significant however as the economy continues to adjust to the sharp increase in price levels over such a short period of time. The outlook for energy prices has improved in recent months as wholesale energy prices have fallen, reflected in a reduction in the Ofgem energy price cap for April to an average of £3,280 per year and latest price cap forecasts from Cornwall Insight projecting a further fall to £2,112.42 in July.[22],[23] The fall in wholesale energy prices will feed through the economy, however the scale and timing of benefit to households in the short term will be dependent on the level of government support (through the Energy Price Guarantee or otherwise) made available over the coming months.

Contact

Email: OCEABusiness@gov.scot