Green Freeports Programme: business and regulatory impact assessment (BRIA)

Business and regulatory impact assessment (BRIA) of the Green Freeports Programme, assessing the costs, benefits and risks of the programme for public, private and third sector as well as regulators.

Section 4: Additional implementation considerations

Enforcement/ compliance

32. In order to ensure Green Freeport incentives translate into the intended policy outcomes, Scottish Government and UK Government have designed the policy to include a range of programme level and local delivery controls. As Green Freeports can only be delivered as a targeted intervention in select locations, these controls help provide assurance that the incentives will be applied in the best available contexts, to achieve the most impact with public investment, whilst mitigating key risks.

Programme controls – 3 phases:

- selection phase: a competitive bidding phase is established, with local coalitions of partners in Scotland invited to join and submit bids to government for Green Freeport status. Bids are assessed on their ability to deliver each of the four core objectives, along with ability to deliver the proposal at pace and the level of private sector involvement in the proposal. The selection phase ran in 2022 and early 2023

- setup phase: following selection, a business case development process is established – with clear requirements for outline and full business cases, where selected Green Freeport coalitions establish operational plans – including approaches to mitigate key risks - which are then appraised by both Governments before approval and unlocking of benefits. This two-stage process allows the governments to further scrutinise and validate this evidence (and, where necessary, mandate changes to the selected Green Freeport’s plans, including proposed geographies and expected beneficiaries)

- delivery phase: following business case approval, Green Freeport sites become operational and the incentives become available. The plans outlined in their business cases are then upheld by a range of local controls, with oversight from Scottish Government and UK Government. At the same time, outcomes are measured by an independent programme of monitoring and evaluation. This includes bi-annual data collection to monitor performance of the Green Freeport and its designated sites, along with annual performance management and assurance processes

- local delivery structures :

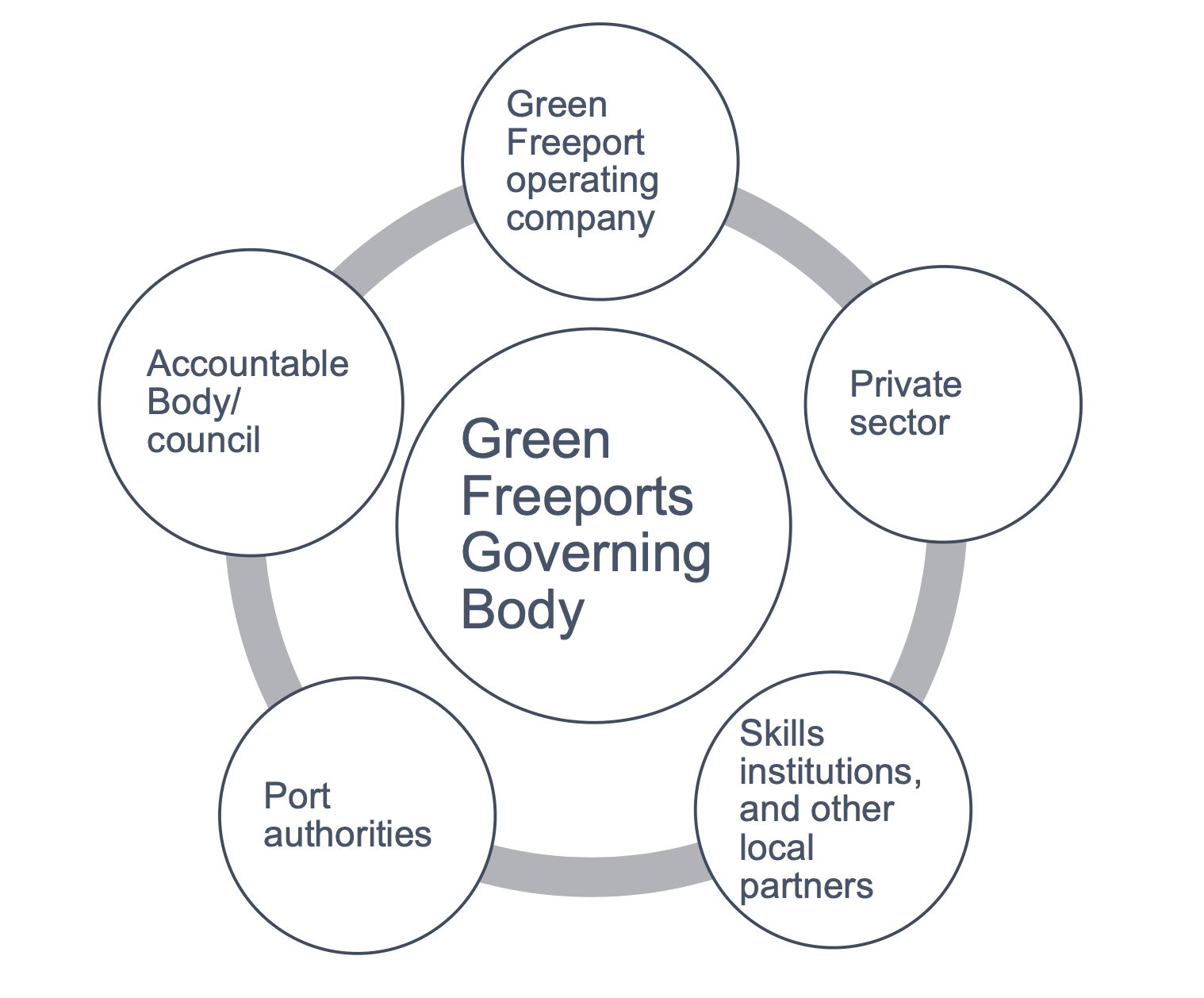

- key local growth partners form a coalition, which collectively develop and deliver a vision for the Green Freeport and its place in regional economy. Into delivery these partners become constituent parts of the Green Freeports Governing Body

Green Freeports Governing Body

- Ensures democratic accountability, transparency and inclusivity.

Accountable body/council

- Oversee spending and non-domestic rates retention.

Green Freeport operating company

- Green Freeport Chief Executive, and operating company support team (approx 3-7 staff), including investment and skills leads.

Private sector

- Landowners, investors, businesses including SMEs.

Skills institutions, and other local partners

- Universities, colleges, schools, and other academic bodies, job centres, innovation partners, career services etc.

Port authorities

- Operation, maintainance, and development of ports.

33. In order to support local partnership working in line with the stated business case plans, and minimise the likelihood of underperformance and the need for government to utilise performance management measures (see below), the governments have also required that two types of local agreement are put in place to ensure alignment of activity with core activity.

- grant funding agreements – seed capital is paid to the Accountable Body within the Green Freeport to support specific projects that have been approved by the governments as part of the Green Freeport business case. Seed capital is provided through the Scottish Government, which puts in place a grant offer letter outlining the specific conditions under which the grant is awarded, and the specific purposes for which it can be used. When awarding this seed capital, a local authority would then be required to put in place a grant funding agreement with the recipient, ringfencing the funding for a specific purpose and providing for clawback as required

- site-specific agreements – these are agreements between the Green Freeport partners, including the local authorities, tax site landowners and end user businesses, specifying the acceptable use of the Green Freeport tax sites. Green Freeports were selected, and their tax sites will be designated, on the basis of a particular understanding of how those sites will be delivered (in terms of timescales and end use) to maximise the realisation of the policy’s equity objective (i.e., delivering investment onto those sites that creates significant numbers of high-quality jobs, is maximally additional, and leads to sectoral clustering and agglomeration benefits). Underpinned by legally binding agreements between the partners, Green Freeports therefore subject prospective investments into their tax sites to a gateway test, which verifies that they align with the agreed use of the tax site (and so the tax subsidies are being applied as intended). These agreements will also form a framework to ensure businesses are engaging with local communities and contributing to Green Freeport funded skills programmes, and adhering to fair work and net zero commitments

Performance Management

34. Each Green Freeport will be subject to requirements to ensure the activities which take place on-site are delivered in accordance with the plans set out in their detailed business cases (approved by UK and Scottish Governments in 2024/5). Once its outline and full business cases have been approved, both Scottish Government and UK Government will jointly sign a Memorandum of Understanding with the Green Freeport and its Accountable Body. Thereafter, the two Governments will hold each Green Freeport to account on their delivery plans and for their use of public money – with the Accountable Body responsible to the Scottish Government for the expenditure and management of Green Freeports seed capital funding.

35. Green Freeports will be subject to annual performance reviews. If a performance issue arose within the Green Freeport, such as consistently poor progress against agreed delivery commitments, or evidence of misuse of public funds, or non-compliance with tax site delivery plans, then UK and Scottish Governments together will have a range of performance management measures available to ensure compliance. Any penalty measures introduced to a Green Freeport by Scottish Government and UK Government would be context dependent, however these may include: implementation of an agreed Tailored Improvement Plan (TIP), increased frequency and/or depth of assurance testing, delay or reduction of capital seed funding, withholding or delaying government support, exclusion from future government support, revoking current policy levers and benefits.

Monitoring and Evaluation

36. A key learning from previous special economic zone interventions is to have in place a robust monitoring and evaluation (M&E) approach on Green Freeports. The M&E approach will provide a key mechanism to hold Green Freeports to account as part of performance management, but also to compare progress between different Green Freeports and Freeports across the UK, and provide a detailed suite of insights and lessons learned to inform wider policymaking.

37. The M&E approach for Green Freeports will be led by an independent evaluation consortium of analytical experts. The approach will bring together quantitative and qualitative analysis, drawing upon primary data provided directly by the Green Freeports, and supplemented by wider data held by a variety of public bodies, e.g. HMRC, Department for Business and Trade (DBT) and Revenue Scotland. A baseline data report will be established at the point which the Green Freeport becomes operational. Thereafter, data will be collected at regular intervals to build an almost real-time picture of progress occurring on Green Freeport sites. Primary data collection from the Green Freeport will take place twice a year, and will capture performance data across a wide range of indicators including jobs, apprenticeships, investment, seed capital spend, retained non-domestic rates spend, innovation, and fair work. Data will be collected by the Green Freeport operating company from their on-site businesses, and be transferred to an independent monitoring and evaluation team which supports the UK Freeports programme. Green Freeports will be asked to collect the same form of data as wider Freeports in the UK, which will aid cross-comparability of progress throughout delivery.

Security and Illicit Activity:

38. The governments are committed to ensuring Green Freeports uphold the UK’s high standards for security and combatting illicit activity. Operators of Green Freeport customs sites must adhere to the OECD Code of Conduct for Clean Free Trade Zones – and the specific anti-illicit trade and security measures therein. They will also need to maintain the current obligations set out in the UK’s Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017

UK, EU and International Regulatory Alignment and Obligations

39. Green Freeports are delivered through a consistent regulatory approach across the UK, with a number of regulations laid to enable Green Freeport delivery. The Scottish Government introduced a single regulatory amendment within the Scottish Parliament to support Green Freeport delivery. This legislative amendment relates to the Land and Buildings Transactions Tax (Scotland) Act 2013, and will enable relief from LBTT for qualifying non-residential transactions within a designated Green Freeport tax site. Further information can be found in The LBTT Green Freeports Relief (Scotland) Order 2023. The implementation of this regulatory change mirrors the amendment undertaken to support wider UK Freeport delivery, through Stamp Duty Land Tax in England and Land Transaction Tax in Wales.

40. Several regulations have also been laid by the UK Government in UK Parliament. In 2021, the UK Government laid regulations which enabled reliefs for National Insurance Contributions, Enhanced Buildings Allowance, and Enhanced Capital Allowance to be claimed on all Freeport tax sites (including Green Freeport tax sites). In addition, legislation is passed in UK Parliament to activate specific tax and customs sites, and designating the exact map boundaries of these sites where the incentives are available.[10]

International Trade Implications

41. The Green Freeports has been designed to support businesses within the Green Freeport area to engage in international trade, and increase trade with other countries. Both tax and customs incentives are designed to support Green Freeports become hubs for global trade and encourage investment in their target sectors. The model builds on existing customs facilitations of tariff and nontariff benefits, making Green Freeports attractive for businesses and supporting them to boost their international competitiveness. Green Freeports and businesses within them can take advantage of the flexibility in the customs model, which permits multiple customs sites with economic links to ports. Businesses importing non-GB goods into a Green Freeport customs site will benefit from a range of tariff and non-tariff benefits.

Tariff benefits:

- duty suspension – i.e., no import duties to be paid on non-GB goods brought into a customs site, until they enter the GB domestic market

- duty flexibility – where declaring goods to the GB market, the ability to calculate import duties based on the value of inputs or finished product, whichever is most beneficial to the business (unless goods are subject to anti-dumping duties, in which case duties are calculated on inputs to avoid circumvention)

- duty exemption for re-exports – unless subject to duty drawback clauses under the relevant Free Trade Agreement, no import duty is paid

Non-tariff benefits:

- simplified import declarations - either:

- a declaration to the Green Freeport procedure at the port using a simplified declaration under a Green Freeport business authorisation. This is separate from the existing Simplified Customs Declaration Procedures

- movement from the port to the Green Freeport customs site via Internal Movements in Temporary Storage (iMiTS) with declaration “by conduct” into the site

- no supplementary declarations needed for goods declared to the Green Freeport procedure under a Green Freeport business authorisation

- movement “by conduct” between Customs sites within a Green Freeport or between UK Freeport Customs Sites where a business authorisation is held. This also includes movement between Green Freeports and Freeports in England and Wales, once operational.

- ability to move from another special procedure to the new Green Freeport procedure using declaration “by conduct”

- all covered by a single authorisation, meaning less contact with HMRC

42. For each customs site, a single ‘Customs Site Operator’ (CSO) must be authorised by HMRC before the site can operate. This will involve HMRC checks to ensure the operator is legitimate, the location is secure, and that the businesses operating within the customs site are complying with relevant security standards. Businesses must then be authorised to use the Green Freeport special procedure on the customs site. Multiple businesses can be authorised to operate under a single CSO within a customs site or the CSO can act as both the operator and the business. Green Freeports are expected to proactively engage with potential CSO and end user businesses to deliver customs sites that will contribute to the Green Freeport achieving its objectives. This should include exploring how customs sites can be used to support supply chain colocation and clustering around the Green Freeport tax sites and how they can be used to extend Green Freeport customs benefits to businesses that have not previously been able to access these trade facilitations or engage in international trade at all.

EU Alignment considerations

43. Other than increasing trade and investment from overseas (of which it is likely that European businesses would be a key commercial market for Green Freeports), the introduction of Green Freeports is not anticipated to impact the Scotland’s alignment with the EU.

Legal Aid

44. Not applicable.

Digital impact

45. Not applicable.

Business forms

46. Only businesses and operators located within designated Green Freeports sites will be subject to reporting requirements. As a set out above in the approach to Monitoring and Evaluation, businesses will be required to provide regular performance data to government, via its independent evaluation consortium. This will include bi-annual completion of a survey, provided by government, capturing key performance indicators. Submissions will be collated for individual Green Freeports and then be quality assured through data cleaning. Where returns have left gaps or are unclear, businesses may be asked to clarify / add more to their form. No businesses or operators outside of designated Green Freeport sites will be required to complete any additional forms or reporting requirements.

Contact

Email: greenfreeports@gov.scot