Fiscal framework outturn report: 2025

The Fiscal Framework Outturn Report 2025 publishes outturn and reconciliation information for Scottish Income Tax, Scottish Landfill Tax, Land and Buildings Transaction Tax and devolved Social Security benefits, as well as updates on borrowing and the Scotland Reserve.

3. Income Tax

22. Since April 2017, the Scottish Parliament has had the power to set rates and bands for non-savings, non-dividend Income Tax. This includes earnings from employment, self-employment, pensions and property. The responsibility for defining the Income Tax base, which includes the setting or changing of Income Tax reliefs and exemptions, and the tax-free Personal Allowance, remains reserved to the UK. For any income people get from savings or dividends, the rates and bands are also set by the UK Government. Scottish Income Tax is therefore a partially devolved tax.

23. For Scottish Income Tax, outturn data is normally available around 16 months after the end of the financial year and a single reconciliation is applied to the following Budget, three years after the original Budget was set. For example, the reconciliation relating to Income Tax raised in the 2019-20 budget year was applied to the 2022-23 Budget.

24. Final outturn data for 2023-24 Income Tax was published by HMRC on 10 July 2025[7]. This data has been used to calculate the reconciliations to the Scottish Government’s Block Grant, which will be applied to the 2026-27 Budget. Table 3 shows the data, together with the net effect on the Budget.

| 2023-24 Income Tax | Revenues | BGA | Net effect on Budget |

|---|---|---|---|

| Forecast as of Scottish Budget 2023-24 | 15,810.0 | -15,485.2 | 324.7 |

| Outturn | 17,092.6 | -16,362.2 | 730.4 |

| Outturn against forecast | 1,282.6 | -877.0 | 405.7 |

25. This translates into a £405.7 million positive reconciliation that will be applied to the 2026-27 Budget (see section 8 for a full breakdown of reconciliations for the 2026-27 Budget).

26. The forecast for 2023-24 Income Tax revenue compared to the corresponding BGA was originally expected to have a positive net effect on Scotland’s finances at the time of setting the 2023-24 Budget, with revenues forecast to exceed BGAs by £324.7 million. The outturn data shows the revenues exceeded the BGA by £730.4 million. This translates into a £405.7 million positive reconciliation, which will correct for the forecast error at the 2023-24 Budget. This is a normal part of the Fiscal Framework and the application of reconciliations should not be interpreted as a reflection of the underlying performance of the Scottish or equivalent UK tax base. The overall benefit of Income Tax devolution to the Scottish Budget in 2023-24 is the aforementioned £730.4 million.

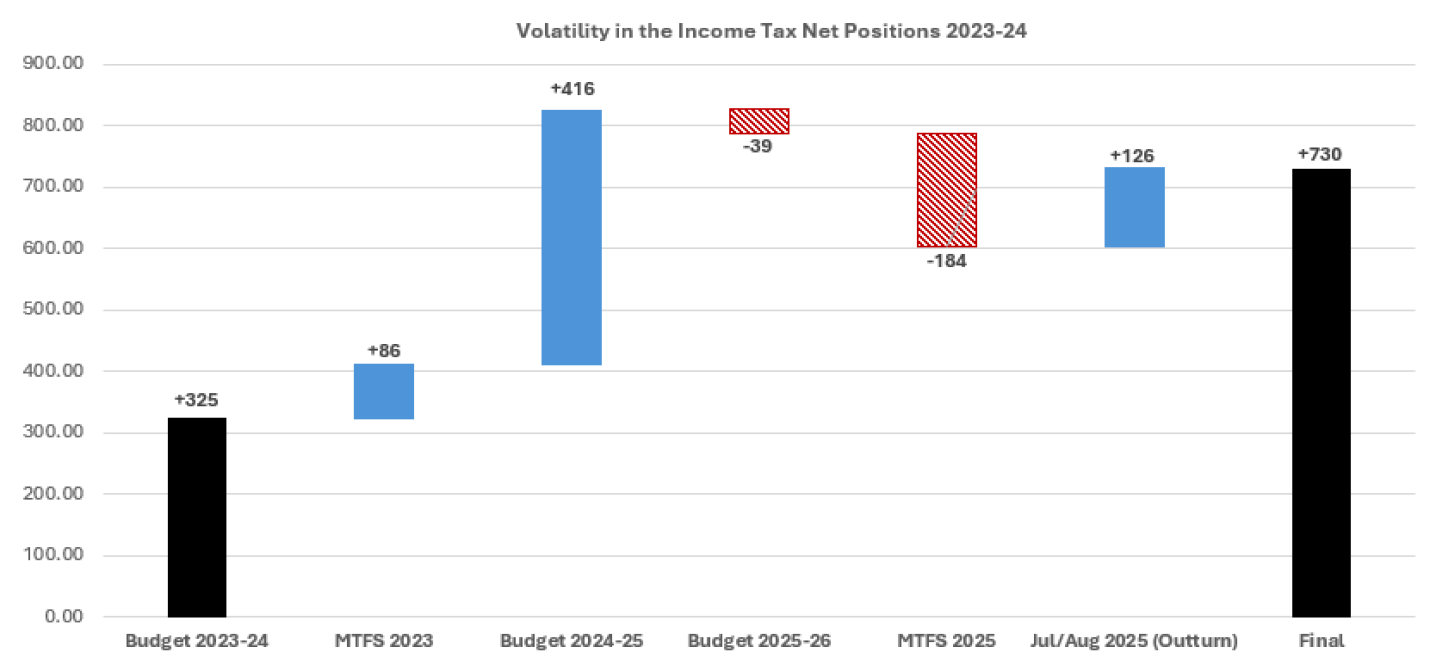

27. Like last year’s reconciliation, there is significant volatility between the forecast-based Income Tax expenditure/BGA net position when the Budget was set and the final outturn-based net position. This will in part reflect that the net position is the difference between the forecasts of two large numbers (Scottish income tax and the BGA), and, therefore, small changes in either forecast can result in large changes in the net position.

28. The forecasts were revised up largely as a result of macroeconomic drivers such as inflation and earnings growth, provisional information about Income Tax paid through Self-Assessment reduced the Scottish Income Tax forecast at MTFS. The majority of the increase at outturn was due to the BGA being lower than previously anticipated. Outturn BGAs also factor in revisions to the comparable Scotland/England and Northern Ireland population growth rate. This is illustrated in Figure 1.

29. The outturn data for Income Tax 2024-25 and 2025-26 should be available in summer 2026 and 2027 respectively, with reconciliations then being applied to the 2027-28 Budget and 2028-29 Budgets.

30. Estimates of future reconciliations for the financial years 2024-25 and 2025-26 are directly derived from latest SFC and OBR forecasts. They have a bearing on the Scottish Government’s multi-year funding envelope as they inform plans on future resource borrowing and spending.

Contact

Email: rory.mack@gov.scot