Environmental Protection (Single-use Plastic Products) (Scotland) Regulations 2021: business and regulatory impact assessment - final

Final Business and Regulatory Impact Assessment (BRIA) for the introduction of market restrictions on problematic single-use plastic items as identified in Article 5 of the EU Single-Use Plastics Directive (EU SUPD).

7.0 Competition Assessment

191. This assessment follows the BRIA toolkit for the Competition Assessment, which is based on the Competition Checklist component of the Competition and Markets Authority's (CMA's) Competition Impact Assessment guidelines.[55] These guidelines recommend considering four key questions in order to assess whether a proposed policy would have an impact on competition. These are:

- Will the measure directly or indirectly limit the number or range of suppliers?

- Will the measure limit the ability of suppliers to compete?

- Will the measure limit suppliers' incentives to compete vigorously?

- Will the measure limit the choices and information available to consumers?

192. The questions are answered with reference to a set of sub-questions defined by the CMA that are considered relevant for each level of the supply chain (upstream, distribution and downstream).

7.1 Identifying relevant markets

193. The markets and stakeholders that may be affected by the restrictions can be divided into three levels of the supply chain:

Table 10. Identification of relevant markets

Supply chain level : Upstream

Definition: Firms that support the manufacture and import of single-use plastic products to be restricted and alternative items, as well as suppliers of raw materials, equipment, and plastics additives.

Example of stakeholder types: Manufacturers, importers.

Supply chain level : Distribution

Definition: Firms involved in distributing single-use items to those that need them. This includes packaging wholesalers as well as high street retailers.

Example of stakeholder types: Catering wholesalers, supermarkets, convenience stores.

Supply chain level : Downstream

Definition: Firms that use single-use items in their provision of goods and services. There may also be a small number of innovative firms that convert plastic products for other uses that may be affected.

Example of stakeholder types: Hospitality sale of food and drinks, chain restaurants, cafes, mobile food services, and catering businesses.

7.2 Overview of markets affected by single-use plastic restrictions

194. This section looks at the value chain of the Scottish market for the relevant single-use plastic products, and for their most-likely alternatives. It presents data, to the extent that it is available, on whether Scottish businesses are active stakeholders at each stage of the value chain, enabling the identification of the stakeholders which are most likely to be impacted by the policy change.

195. Upstream: The manufacturing of single-use plastic products in Scotland takes place within the wider manufacture of plastic and rubber products sector. This sector is tracked by the Scottish Government and has aggregate data published in the annual "Businesses in Scotland" publication (2020). More granular data on the production of specific single-use plastic product types are not available.

196. A summary of the available data showing trends in the Scottish plastic and rubber products sector is provided in Figure 1, below. The number of Scottish firms in this sector declined sharply between 2010 and 2012 before levelling off and beginning a slower decline to 2020. The size of the workforce has decreased somewhat in step with the reduction in firms.

Source: Europe Economics analysis, based on Scottish Government (2020) "Businesses in Scotland"[56]

197. The following analysis looks at three main segments: producers of polymers which could be used as inputs for the relevant single-use plastic items; producers of the single-use plastic items excluding EPS products; and producers of EPS products.

198. Producers of polymers for single-use plastics: In 2017, Scotland was responsible for approximately 30 per cent of relevant polymers made in the UK,[57] though it accounted for just 5 per cent of plastics and rubber firms in the UK.[58] This raises a question around whether Scottish polymer producers could be impacted by the restrictions. According to the British Plastics Federation (BPF), just two firms in Scotland may be driving this polymer production: Ineos Olefins and Polymers (capacity: 615,000 tonnes p.a.) and PET Processors (UK) LLC (capacity: 20,000 tonnes p.a.). Both produce a range of products in addition to potential inputs to the single-use plastic items in question.[59]

199. It was not possible to find data on the extent to which polymers produced domestically are used for the production of the relevant single-use plastic items in Scotland, nor the extent to which end products produced from them are consumed domestically. However, the evidence suggests that local producers of relevant items only represent a small share of demand for locally-produced polymer.

200. First, there is only a small single-use plastic manufacturing presence in Scotland (see below: 'Producers of single-use plastic items excluding EPS'). Second, research conducted for Defra indicates that a majority of the relevant single-use plastic products consumed in the UK are imported.[60] Finally, the volumes involved are considered. According to the Strategic Environmental Assessment for this policy change, the total weight of relevant single-use plastic items used in Scotland in 2020 was 1,848 tonnes,[61] equivalent to just 0.3% of the total weight of polymers produced each year by the two domestic producers noted above. It is concluded that Scottish polymer producers are unlikely to experience significant impacts from the policy change.

201. Producers of single-use plastic items excluding EPS Recent research conducted for Defra indicated that imports of single-use plastic products into the UK as a whole accounted for:[62]

- 90% of cutlery, plates, balloon sticks.

- 95% of straws, cotton buds and stirrers.

202. Desk research identified a number of manufacturers of relevant single-use plastic items, as well as some firms that manufacture alternatives. Both types of firm are shown in the following table. This information was retrieved via online searches for manufacturers in Scotland, manually reviewing the items they produce. In all cases, the products listed in column three appear to account for a small proportion of the offering of each firm, though it is not possible to identify the precise relative importance of sales of the single-use plastic items.

Table 11. Manufacturers of single-use plastic and alternative products identified in Scotland

Company: Tri-Star

Materials: Polypropylene, cardboard, wood

Products: Cups, food boxes, and cutlery

Area: Glasgow

Company: Kimberly Watson Packaging

Materials: Plastic

Products: Trays for baked goods

Area: Livingston, West Lothian

Company: Streetfood Packaging

Materials: Plastic, alternative materials (cardboard, palm leaf)

Products: Food and beverage cups, trays and boxes

Area: Aberdeen

Company: Vegware

Materials: Wood, paper, bagasse, products coated in plastics

Products: Straws, plates, cutlery, food containers, and cups

Area: Edinburgh

Company: Cullen

Materials: Moulded pulp, corrugate

Products: Food and beverage containers

Area: Glasgow

Company: Eco Pack Scotland

Materials: Bagasse, recycled plastics

Products: Food and beverage containers

Area: Edinburgh

Company: Verona Eco

Materials: Paper, board

Products: Food and beverage containers, trays, and pots

Area: East Kilbride

203. Given that 90-95% of single-use plastic cutlery, plates, balloon sticks. straws and stirrers are imported into the UK (and we found no evidence that this differs materially for Scotland), it is concluded that manufacturing of the relevant products does not form a significant part of the Scottish value chain for single-use plastic products. One firm which was identified through stakeholder engagement as being affected was Vegware, which produces some lines of cutlery and straws that fall in scope of the regulations but a significant proportion of its business is production of non-EPS food and beverage containers which will benefit from the market restrictions.

204. Producers of EPS items: The Defra research cited above found that imports into the UK accounted for just 5% of EPS food and beverage containers.[63] This suggests that a large share of the relevant EPS items is produced within the UK. A 2019 Defra impact assessment found that there were just four EPS plants involved in the manufacture of relevant single-use plastic items in the UK as a whole.[64] We sought to identify whether any Scottish EPS manufacturers would be affected. This involved two main streams of research.

205. First, via desk research we explored whether we could identify relevant EPS manufacturers operating in Scotland. We did find a number of firms operating in Scotland that produce EPS products, but their product offerings covered larger items, such as EPS products for large-scale insulation, that did not fall within the scope of the restrictions.[65] It is possible that some of these firms have side-lines in producing smaller EPS items, but this could not be verified.

206. Second, we asked stakeholders to identify any manufacturers of relevant EPS products operating within Scotland. The British Plastics Federation was not aware of any producers of single-use items in Scotland and suggested that if there were any such producers, their share of total plastics production in Scotland would be very small.

207. Third, Zero Waste Scotland discussions with representatives from the Scottish EPS manufacturing sector[66] revealed that virtually all manufacturing of the target EPS containers had ceased in Scotland due to the low economic returns available for producing these items domestically and a growing acceptance that market restrictions on problematic single-use plastic items would be implemented.

208. It is concluded that the majority of in-scope EPS items are imported into Scotland from elsewhere in the UK.

209. Distribution: Further down the value chain are distributors and retailers of single-use plastic items and their alternatives to consumers, both in the hospitality trade and in private households. The table below shows a selection of distributors and retailers known to be operating in Scotland based on online research. The market includes three smaller, family-run businesses (Morrison's Food Services, Scottish Disposable Supplies and RBR Supplies) competing alongside large multinational firms.

210. The single-use plastic items in the scope of the restrictions, the majority of which are provided to customers alongside food products, tend to comprise only a small part of the catalogues of catering distributors. Many of these firms also currently sell alternatives to single-use plastic items. It is concluded that a handful of actors of different sizes at this level of the value chain in Scotland will be affected by the restrictions, though it will only affect a small part of their overall business.

Table 12: Examples of wholesalers and distributors operating in Scotland

Company: James Kidd

Description: One of Scotland's largest independent distributors of catering supplies and equipment.

Examples of items sold: Packaging made of plastic, polystyrene, and alternatives including bagasse, paper/card and moulded fibre.

Company: Morrison's Food Services

Description: A family-run business originally established to supply food items to the food service sector, since expanding to provide a variety of food containers.

Examples of items sold: Polystyrene and cardboard food trays as well as bagasse items.

Company: Scottish Disposable Supplies

Description: An independent supplier of catering disposables.

Examples of items sold: Plastic and polystyrene food containers, paper plates.

Company: RBR Supplies

Description: A family-run distributor of catering cleaning supplies based in the West of Scotland that has begun to supply disposable cutlery and crockery.

Examples of items sold: Plastic cutlery and stirrers, plastic cups, Vegware compostables.

Company: Nisbets

Description: With three locations in Scotland, the largest supplier of catering equipment in the UK sells various catering and kitchenware to all end-consumers.

Examples of items sold: Wide range of plates, containers and cutlery, both plastic and non-plastic, as well as compostable products.

Company: Bidfood Scotland

Description: A subsidiary of the international Bidfood UK company, Bidfood Scotland sources items from large multinationals and small 'artisan' producers.

Examples of items sold: Expanded polystyrene food containers, newspaper boxes, bagasse items, plastic and wooden cutlery.

211. Downstream: Other Scotland-based firms impacted by the introduction of market restrictions are those in the food and beverage service sector. These firms provide food or drinks fit for immediate consumption in traditional, self-service or take-away restaurants and cafés, whether as permanent or temporary set-ups and with or without seating.[67] Many of these provide take-away food and beverages that are likely to be served in the single-use plastic products within the scope of the restrictions: there were 3,505 take-away businesses in Scotland as of 2018.[68] The Scottish Government's Businesses in Scotland publication indicates that small and micro businesses account for 97.7 per cent of the firms in the food and beverage sector, the majority of these employing fewer than ten employees (see Figure 2).

212. Table 14 shows that take-aways account for 33% of the total number businesses supplying food and beverages in Scotland. Licensed restaurants and cafes account for 25% and unlicensed restaurants and cafes for 23%.

Source: Europe Economics analysis of Scottish Government (2020) "Businesses in Scotland". Food and Beverage Service Activities.[69]

213. Figure 2 also shows the steady growth of the number of firms in the food service sector. Prior to the Covid-19 pandemic, the takeaway food market had enjoyed significant growth in Scotland in recent years. Between 2010 and 2018, the number of takeaway firms in Scotland increased by 28 per cent, and in 2018 the average household spent £244 on takeaways consumed at home.[70] In the three years to 2019, the UK takeaway sector doubled in size.[71] It is concluded that there is a sizeable market in Scotland at this level of the value chain, some of which will be impacted by the proposed restrictions.

Table 13. Scottish food outlets and services (2018)

SIC : Sector Number

- 56.10/3 Takeaways & food stands : 3,505

- 56.10/1 Licensed restaurants & cafes : 2,725

- 56.10/2 Unlicensed restaurants & cafes : 2,440

- 56.2 Events & outdoor catering : 1,220

- 56.21 Other food services : 850

- Total : 10,740

Source: ONS, Nomis Database.

7.3 Detailed Competition Assessment

Will the measure directly or indirectly limit the number or range of suppliers?

214. This question aims to identify, and where possible quantify, potential impacts of the policy change on limiting the number and range of suppliers in Scotland, with a view to assessing potential impacts on the prices and available choices of the relevant single-use plastic items and their most-likely alternatives to consumers in Scotland.

215. The following paragraphs aim to answer this question in line with the CMA guidance. It considers the possibility of direct and indirect impacts separately, for which a set of relevant sub-questions are answered (based on the issues suggested by the CMA). The sub-questions are as follows:

216. Direct impacts

- Does the measure award exclusive rights to supply?

- Does the measure require procurement from a single supplier or a restricted group of suppliers?

- Does the measure create a licensing scheme that limits the number of suppliers?

- Does the measure create a licensing scheme for quality standards?

217. Indirect impacts

- Does the measure significantly raise the costs of incumbent firms, causing them to exit the market?

- Does the measure significantly raise the costs of new suppliers (including small businesses) relative to existing suppliers?

- Does the measure significantly raise the costs of some existing suppliers relative to other existing suppliers?

Upstream

Direct impacts

218. The Scottish Government is restricting manufacture of all the relevant single-use plastic items except for straws and balloon sticks. However, neither the proposed restrictions on supply, nor any potential restrictions on manufacture, explicitly aim to restrict the number or range of manufacturers of any specific item through:

- Awarding exclusive rights of supply;

- Requiring procurement from a single supplier or a restricted group of suppliers;

- Introducing a licensing scheme for suppliers or quality standards.

- It is therefore concluded that there are no direct competition impacts

Indirect impacts

Does the measure significantly raise the costs of incumbent firms, causing them to exit the market?

219. The market restrictions are unlikely to significantly raise the costs of incumbent firms, causing them to exit the market. There may be some costs for adapting production to alternatives, but the small number of single-use plastic-producing firms in Scotland suggests that this would not affect many firms. These points are explained in what follows.

220. The high import share in the single-use plastic market in the UK, and the market overview in Section 6.2, suggests there are not many manufacturers of single-use plastic products in Scotland that would be affected. We can estimate the extent to which this is the case by combining the aforementioned import proportions with estimates of annual consumption quantities of the various single-use plastic products. We find that 19.8 per cent of domestically consumed single-use plastic products may be produced domestically, the majority of which are EPS containers (see table below). However, the EPS containers account for less than 15 per cent of the single-use plastics consumed in Scotland, and – given the research finding of there being zero manufacturers of EPS single-use plastics in Scotland – excluding them reduces the estimated proportion of consumed single-use plastics to 6.2 per cent. Moreover, these domestically produced single-use plastic products represent just 0.29 per cent of the turnover of the plastics and rubber manufacturing sector in Scotland in 2020 (when EPS are excluded, this drops to only 0.1 per cent).[72] Therefore, it is reasonable to suggest that knock-on effects of a drop in demand for single-use plastic products would affect only a small number of Scottish manufacturers. These firms could choose to exit the market or adapt processes to alternative products.

| Single-use plastic products | Estimated consumption in Scotland (million, per year) | Share of single-use plastics consumed in Scotland (%) | Estimated number produced domestically (million, per year) | Estimated number produced domestically (million, per year) assuming zero EPS/XPS manufacturers |

|---|---|---|---|---|

| Balloon sticks | 1.7 | 0.2 | 0.17 | 0.17 |

| Straws | 300 | 38.6 | 15 | 15 |

| Cutlery | 276 | 35.5 | 27.6 | 27.6 |

| Stirrers | 9.9 | 1.3 | 0.495 | 0.495 |

| Plates (incl. trays and bowls) | 50 | 6.4 | 5 | 5 |

| EPS food containers | 66 | 8.5 | 62.7 | 0 |

| EPS drinks containers | 45 | 5.8 | 42.75 | 0 |

| Produced domestically (% of consumed single-use plastics) | - | - | 19.8 | 6.2 |

221. The restrictions are likely to indirectly accelerate the market for alternative products by encouraging existing manufacturers of single-use plastic items and alternatives to maintain their position in the production of these types of products by adjusting production towards alternatives more exclusively. Some existing manufacturers of single-use plastics may be able to adapt production to satisfy the demand for alternative products – at a cost. Two stakeholders who responded for the Scottish Firms Impact Test suggested that the cost impacts associated with changing manufacturing and production processes are likely to be the biggest potential impacts of the restrictions. Three studies for Defra on the impact of similar restrictions in the UK have estimated the total costs to business of implementing them over a ten-year period, during which manufacturers of single-use plastics experience a gradual reduction in sales. These are reported in Table 15 below.

222. The business implementation costs include the annual cost of implementing the restrictions over the period, as well as one-off capital costs for all but the EPS products (for which costs are reported separately in the table as significant capital investments). The annual costs of implementing the restrictions would be expected to involve the following for manufacturers:[73]

223. Transition costs: costs involved in refocusing production towards alternative single-use items, which may be low and involve relatively short timescales for existing suppliers of alternatives.

224. Overproduction costs: The costs of manufacturers sitting on redundant warehoused single-use plastics upon the implementation of restrictions, which could be minimised if clear timescales are provided in advance.

225. Scale costs: the costs involved in scaling-up production of non-EPS single-use items (these costs were not reported in the Defra study of EPS products, so we assume that they are not applicable to EPS producers; moreover, the lack of EPS single-use plastics producers in Scotland suggests that they are not relevant). Research for Defra suggests that economies of scale would be possible in the event of the single-use plastic ban being considered in England.[74] Consulted stakeholders did not indicate the nature of additional costs (e.g. labour, materials)

226. It has been previously highlighted that EPS single-use plastics are produced domestically in the UK (but not in Scotland), whereas the other single-use plastic items in scope are largely imported. The modelling for the UK assumed that a one-off capital investment would be needed to convert existing EPS packaging manufacturing capacity or establish new packaging production capacity for EPS-free products. Stakeholders suggested that capital costs could amount to £30m per plant.[75] The capital costs are displayed separately for the EPS product categories in the following table.

| Item | Business implementation cost for all types of businesses NPV 2019-28 (£m) | One-off capital investment for manufactures (£m) |

|---|---|---|

| Cutlery | 3.1a | |

| Plates | 0.8a | |

| Straws | 2.3b | |

| Drink stirrers | 1b | |

| Balloon sticks | 0.2a | |

| EPS food containers | 2.4c | 47.7c |

| EPS beverage containers | 1.7c | 68.1c |

227. Based on the figures presented in Table 15, the cost to the few manufacturers of single-use plastics in Scotland of transitioning to alternative products is likely to be relatively low. This is because the business implementation costs are generally low (considering that the figures are spread across all businesses in the UK) and no EPS manufacturers have been identified in Scotland (so the one-off capital investment costs do not apply).

228. Furthermore, that plastic polymer production in Scotland does not appear to contribute to the Scottish manufacture of single-use plastics suggests that firms involved in polymer production would not face costs due to the market restrictions.

Does the measure significantly raise the costs of new suppliers (including small businesses) relative to existing suppliers?

229. The market restrictions are unlikely to significantly raise the costs of new suppliers relative to existing suppliers.

230. Recognising the potential profit to be made in the market for these types of products upon the market restriction of the single-use plastic variants, there may be market entry of new manufactures of alternatives. This may also offset any potential indirect reduction in the number of manufacturers caused by the restrictions. Scotland does not currently have a particularly large wood and paper products industry (it is the smallest manufacturing subdivision in terms of 2018 gross value added)[76] – a sector that could be expected to satisfy the demand for alternative packaging products when the restrictions begin. The sector is however nearly twice as productive per manufacturing sector worker as the same sector in England,[77] potentially giving it a competitiveness advantage over English manufacturers in satisfying the demand. And the current existence of successful eco-friendly packaging firms in Scotland, such as Cullen and Eco Pack Scotland, suggests that opportunities for new market entries could arise.

Distribution

Does the measure significantly raise the costs of incumbent firms, causing them to exit the market?

231. There would be a degree of familiarisation costs associated with the restrictions. The introduction of the legislative restrictions would cause a period of adjustment to the new regime for all firms involved in the sale of single-use plastic products domestically. This is unlikely to threaten the number of distributors in the market.

232. The number of wholesalers and distributors of single-use plastic products is unlikely to be significantly impacted by costs unless (directly or indirectly) any of these deal predominantly in the restricted single-use plastic products and face issues in sourcing alternatives or significant cost increases that they cannot pass on to customers. This assessment has identified a number of Scotland-based manufacturers of alternative products for food service activities, so difficulties in sourcing alternatives may stem from alternative manufacturers' capacity constraints rather than from difficulties in locating manufacturers. Balloon sticks may be harder to source, as the market overview did not identify any domestic manufacturers of them (plastic or otherwise), but the small number consumed annually suggests that this may not threaten the revenues of distributors to a great extent.

233. The single-use plastic items in the scope of the restrictions, the majority of which are provided to customers alongside food products, tend to comprise only a small part of the catalogues of catering distributors. Many of these firms also currently sell alternatives to single-use plastic items. It is unlikely that such firms would be significantly affected by the restrictions.

Downstream

Does the measure significantly raise the costs of some existing suppliers relative to other existing suppliers?

234. Downstream firms, unable to produce the single-use products themselves, would be indirectly affected by any price and availability issues that emerge further up the supply chain. It is possible that the costs of some firms will rise relative to other existing suppliers.

235. In the study for Wales[78] it was reported that smaller downstream hospitality outlets and charities who are less able to absorb any cost increases caused by a move towards alternatives may be disproportionately affected. But that the overall impact (to these disproportionately affected groups and to larger companies alike) will be negligible because the price differential between the plastic product and the alternative is relatively small or non-existent in some cases.

236. Research[79] by Zero Waste Scotland on the price impact of market restrictions on single-use items looked at how additional costs are shared or passed along the supply chain with evidence from stakeholders suggesting that the first differentiation occurs when considering the relationship between the individual or entity purchasing the item and the individual using it.

237. Where the individual buying the item is also the person who will be making use of it, the additional cost is normally passed directly to the consumer. For example, when an individual purchases a box of paper straws for their personal use, they are directly impacted by the increased cost of the paper-based product. Stakeholder communication with one mid-range supermarket as well as an interview with a representative previously involved in another supermarket's sustainability strategy confirmed this finding. The latter added that when the sale was business-to-consumer, product price was heavily dictated by profit margin and there was therefore little scope for absorption of any additional costs.

238. The exception, however, was presented by a low-cost supermarket with a business built on ensuring that its product lines remain cheaper than those of its competitors. Its aim was to prevent customers from noticing any increases in price as a result of changes in the supply chain. As such, the representative of this supermarket stated that it absorbed any additional costs associated with transitioning to a new alternative product. This suggests that people shopping in low-cost supermarkets may be less likely to experience price increases as a result of the policy change than people shopping in mid-range or premium retailers.

239. In contrast, when an item is provided as an aspect of a service, for example a stirrer in a tea at a coffee shop or a straw in a drink from a takeaway outlet, the distribution of the additional costs becomes more varied and complex. In these scenarios, the product is passed through a greater number of nodes in the value chain, and there is therefore more opportunity for variation in approach.

240. The relatively large number of takeaway outlets in Scotland (3,505) suggests that the market is very competitive. Whereas cost shocks for individual firms or groups of firms could be disruptive to competition, a cost rise experienced by all firms – which could be expected among the smaller firms given the restrictions and a move towards some more costly alternative products – may be simply passed on to the final consumer in the price they pay for takeaway food products. On the other hand, more high-end and larger outlets might be more willing/able to absorb additional costs. Without detailed information on the distribution of cost margins across Scottish food outlets it is not possible to fully assess the extent to which any potential additional costs to businesses will be absorbed or passed on.

241. Table 16 below sets out the average prices for single-use plastic items and the most likely non-plastic alternatives. Plastic cutlery, stirrers and straws are, on average, the same price as non-plastic alternatives. Non-plastic plates and cups are 1-2 pence more expensive than equivalent plastic items. Non-plastic balloon sticks are 3 pence more expensive than plastic balloon sticks but the number of these in circulation is relatively small, accounting for 0.01 per cent of all items in scope. Compostable/bagasse food containers are on average 3.7 pence more expensive than EPS containers.

| Product | Material | Item Price £ | Material | Item Price £ |

|---|---|---|---|---|

| Cutlery | Plastic | 0.04 | Wood | 0.04 |

| Plates | Plastic | 0.06 | Paper | 0.07 |

| Beverage stirrers | Plastic | 0.01 | Wood | 0.01 |

| Straws | Plastic | 0.01 | Paper | 0.01 |

| Balloon sticks | Plastic | 0.07 | Paper/card | 0.10 |

| EPS Food containers | Plastic | 0.08 | Bagasse | 0.12 |

| EPS Beverage cups | Plastic | 0.03 | Paper/card | 0.04 |

242. Research by Spice[81] found that the average Scottish household spends £244 annually on takeaway food resulting in a total market[82] for takeaway outlets of £579 million.

243. It has not been possible to present data on typical turnover or gross profit margins in the food takeaway sector but Table 17 below indicates the scale of additional costs that may arise as a result of switching all single-use plastic items to non-plastic. The relevant non-plastic items identified as currently being more expensive than their single-use plastic counterparts are plates, food containers and cups.

| Plates | Food Containers | Cups | |

|---|---|---|---|

| Number (million) | 50 | 66 | 45 |

| Price Difference (£) | 0.01 | 0.04 | 0.01 |

| Cost (£ million) | 0.5 | 2.64 | 0.45 |

244. Under this approach, total additional costs to the takeaway sector are estimated to be around £3.6 million which represents 0.6 percent of the total £579 million Scottish takeaway food market. It should be noted that the prices of alternative single-use products may be too high, particularly in the later part of the time period under consideration. This is because as market demand for alternative single-use products rises, their prices are likely to fall owing to economies of scale and product innovations for non-plastic alternatives.

Does the measure significantly raise the costs of incumbent firms, causing them to exit the market?

245. Incumbent firms may experience a small but insignificant cost rise through a degree of familiarisation costs associated with the restrictions. Smaller hospitality outlets without the resources to maintain close observation of legislative developments may be disproportionately affected,[83] but this alone is unlikely to threaten their number. Moreover, a programme of public engagement, as well as the transition period for the introduction of market restrictions, is likely to mitigate the extent of familiarisation costs.

Will the measure limit the ability of suppliers to compete?

246. This question investigates whether the market restrictions could affect the ability of firms to influence the characteristics that make their products stand-out relative to their competitors. Such characteristics may include: the price, quality, level of innovation, marketing strategy and sales channel. Inhibiting the ability of firms to establish their own combination of these characteristics can in turn hinder competition between them.

247. For this question, the CMA guidance suggests that the following sub-questions should be addressed, where relevant:

- Does the measure control or substantially influence the price a supplier may charge and/or the characteristics of the products supplied?

- Does the measure limit the sales channels a supplier can use, or the geographic area a supplier may supply in?

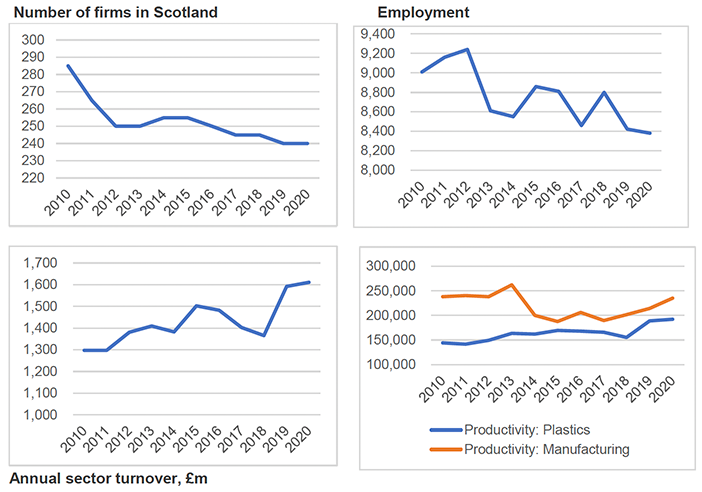

- Does the measure substantially restrict the ability of suppliers to advertise their products?

- Does the measure limit the suppliers' freedom to organise their own production processes or their choice of organisational form?

248. Discussions of the first and third sub-question for are considered relevant for the market restrictions on single-use plastics.

Upstream

249. Does the measure limit the sales channels a supplier can use, or the geographic area a supplier may supply in?

250. Rest-of-UK manufacturers of single-use plastic items will no longer be competing for the sale of single-use plastic items in Scotland. Manufacturers that currently focus predominantly on exports to markets beyond the jurisdiction of the EU SUPD may thus be in a better position to compete than other manufacturers since they would be partly shielded from the restrictions. The high proportion of imported single-use plastics, however, suggest that the UK's share of the export market is not large and that this line of argument is unlikely to apply to many firms in Scotland. Therefore, there may not be any significant competition impacts on geographical areas of supply for manufacturers.

251. Does the measure controls or substantially influence the characteristics of the products supplied?

252. The characteristics of single-use items could be influenced by the restrictions. If alternative products are intrinsically different such that they require certain equipment to produce and significantly higher capital expenditure, this could pose a barrier to entry to smaller firms wishing to transition to non-single-use plastic production. It has not been possible to determine whether capital expenditure costs are significantly different between single-use plastics and non-plastic alternatives.

Distribution

253. Does the measure control or substantially influence the characteristics of the products supplied?

254. The market overview exercise noted three smaller distributors of single-use items in Scotland. Observing their catalogues of products currently on offer suggests that single-use plastics comprise a material proportion of their historic sales of single-use items for the food takeaway trade. These smaller firms may therefore experience greater frictions of transitioning to non-plastic alternatives than the larger multinational distributors that are more likely to be able to procure them, both domestically and from overseas. That larger firms can source inputs at lower prices than smaller ones is routinely noted in the literature (for example, larger firms can benefit from greater buyer power and can have teams of employees devoted to negotiating with suppliers).[84] However, this exercise also shows that the smaller distributors have managed to stock alternatives, suggesting that the competition impact would be minimal.

Downstream

255. Does the measure control or substantially influence the characteristics of the products supplied?

256. The restrictions would directly control the characteristics of the single-use items that downstream firms can provide with their food services. However, research conducted for Defra concluded that despite stakeholder concerns, alternatives with equivalent functionality for consumers exist for single-use plastic cutlery and plates, and for EPS food containers and cups.[85],[86] Wooden alternatives to single-use plastic beverage stirrers are already widely in use and do not affect functionality.

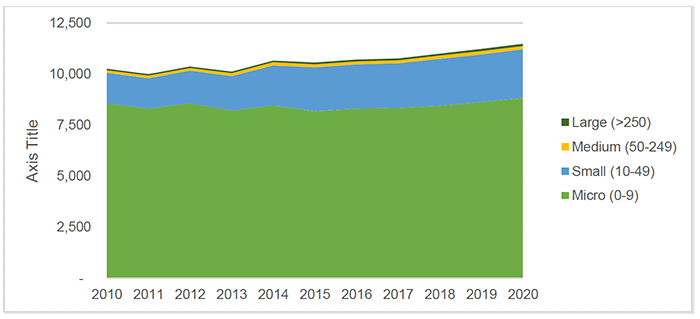

257. Card-based alternatives to single-use plastic balloon sticks are available. While these may be less durable than their single-use plastic equivalents, there will not be a significant impact on consumers given the short, in-use life of the items. An exemption exists for plastic balloon sticks used and collected for re-use by businesses and professionals.

It is acknowledged that no alternative to single-use plastic straws has exactly equivalent functionality—though innovation in this area is ongoing. A study for the Welsh Government identified a lack of readily-available alternatives to single-use straws capable of piercing through the film on drinks cartons/pouches.[87] However, at least two multinational manufacturers in Europe are introducing paper alternatives that are capable of piercing through drinks cartons.[88]

Will the measure limit suppliers' incentives to compete vigorously?

258. The purpose of this question is to ascertain the extent to which firms may be incentivised to mutually agree to stop or reduce the extent of competition between them (e.g. in terms of the price and/or quality of a product, or the type of customers). In other words, firms may or may not be incentivised to coordinate their behaviour.

259. The CMA guidance suggests the following sub-questions may be answered in response to this question:

- Does the measure incentivise suppliers to coordinate their behaviour?

- Does the measure exempt suppliers from competition law?

- Does the measure introduce or amend and intellectual property regime?

260. The restrictions are unlikely to facilitate or encourage the coordination or collusion of firms in the manufacturing, distribution or downstream market segments. The market restrictions do not exempt suppliers from competition law nor introduce or amend an intellectual property regime.

261. The remaining sub-question is whether the measures would incentivise suppliers to coordinate their behaviour. The market restrictions would serve to create a new, but level, playing field for all participants in the supply chain, which does not present clear incentives for participants to coordinate. The downstream food service sector is especially competitive and extremely unlikely to experience any coordination of firm activity as a result of the restrictions.

Will the measure limit the choices and information available to consumers?

262. The choice of product consumers make is key to driving competition between firms. A consumer making a decision informed with the relevant information of a firm's product will either reward the firm (by purchasing its product) or send a signal to the firm that its product does not meet the consumer's preferences. This question investigates whether consumers may become limited in their ability to make these choices.

263. The following sub-questions may be considered based on the CMA guidance:

- Does the measure limit the ability of consumers to decide from whom they purchase?

- Does the measure change the information available to consumers but does not improve their ability to make informed decisions?

- Does the measure reduce the mobility of consumers by increasing the cost of changing suppliers?

264. Of these sub-questions, the first is considered to be potentially relevant for the upstream, distribution and downstream levels of the supply chain.

Upstream

265. Does the measure limit the ability of consumers to decide from whom they purchase?

266. Consumer choice would be limited by (a) the unavailability of restricted single-use plastic items and (b) if the choice of manufactured most-likely alternatives was more restrictive. Possibility (a) is largely unavoidable given the restrictions. Possibility (b) would only emerge if, for example, manufacturers were limited in their capacity to produce the quantity of alternatives required, but as we have discussed above, it seems likely that the range of alternatives available would expand. As discussed previously, there are a number of alternative products already being produced and distributed in Scotland, and it is likely that market incentives would encourage manufacturers to produce a greater variety of alternatives in the longer-term. The end-consumption of existing single-use plastic products is generally not for its own benefit since these products are provided to consumers as complementary goods with other products, such as takeaway food and beverages. Their consumption choices are unlikely to be affected by the single use plastic material type. Therefore, if it were restricted at all, consumer choice would only be limited by alternative manufacturing capacity in the short-term, and this is unlikely to disadvantage consumers.

Distribution

267. Does the measure limit the ability of consumers to decide from whom they purchase?

268. Factors that might lead to consumers in certain areas being limited in choice including questioning whether distributors of alternatives have the geographic distribution capacity to reach all downstream firms across Scotland. A question asked of stakeholders was whether consumers of takeaway food in the islands may be limited in their choice of food products if the food outlets are limited in what containers they have been able to procure.

269. Stakeholder responses indicated that alternative items could be sourced through existing supply chains, including the more remote areas of Scotland.

Downstream

270. Does the measure limit the ability of consumers to decide from whom they purchase?

271. To the extent that downstream firms increase prices to match the increase in the costs of single-use plastic alternatives, this could limit the affordability and choice of certain end products for consumers. Assuming single-use plastic alternatives do increase the cost of end-products (with, for example smaller food outlets with tight margins), and if enough consumers turn away from them, downstream firms could, theoretically, experience a reduction in demand.

272. We can investigate whether consumers may turn away from the end-products with which single-use plastics are provided using price elasticities. Price elasticities measure the extent to which a change in price is associated with changes in demand for a product. In the case of "own-price elasticities" (changes in the product's own price), values of less than -1 indicate elastic demand; between 0 and -1 indicate inelastic demand.

273. Research conducted for Defra in 2012 on the elasticities of different food products suggests that takeaway food is generally inelastic – that is, demand is relatively unresponsive to price. For example, a 10 per cent increase in the price of takeaway poultry would be expected to decrease demand by a proportionately-smaller 8 per cent.[89] The same increase applied to other takeaway meat would result in just 2 per cent lower demand. (Please refer to the Appendix for further detail of these elasticities.)

274. The elasticity estimates reported above relate to only takeaway meat items, and so the picture may be different for other popular takeaway foods. The booming takeaway market in the UK, and its expected steady growth in future years,[90] suggests that overall demand is unlikely to fall, and so any small price increments caused by the cost of single-use alternative items may be offset by overall revenue growth.

275. Zero Waste Scotland research on transfer of change in item costs found that some food outlets and retailers (higher-end ones) may instead absorb any cost increases,[91] thus leaving consumer prices unchanged.

276. Overall, the evidence from the elasticity estimates available suggests that if the additional costs of sourcing suitable alternatives to takeaway food packaging items are passed on to consumers in full, then downstream takeaway firms may not experience dramatically reduced demand given consumers' relative insensitivity to takeaway price changes.

277. In the case of balloon sticks, consumers could face a slightly more limited choice if a range of non-plastic alternatives are not forthcoming. However, exemptions exist for those used for industrial/professional uses.

Contact

Email: supd@gov.scot