The Environment Strategy for Scotland: Delivering the Environment Strategy Outcome on Scotland's Economy - Evidence Base & Policy Levers

This report presents evidence and initial recommendations on how the Scottish Government could use the available policy levers to support the transformations in Scotland’s economy needed to help tackle the climate and nature emergencies.

3. Section A: Evaluating Scotland’s progress in driving a just transition to a net zero, nature positive and circular economy

3.1 Overview

There is no comprehensive source of evidence on how Scotland is performing towards achieving the goal of a just transition to a net zero, nature positive, circular economy. Scotland is not alone in this regard. It is not straightforward to make assessments about the sufficiency of individual or collective policies, due to the uncertain nature of the impact of policies, and constraints around the availability of data to track progress. Indeed, the formal evaluation process for many policy levers will not have started or may take years to be fully informed. Separately, many policy levers, such as within skills, may not directly be linked to environmental outcomes but provide ancillary effects to support or hinder the transition. Separately, in other fields, like biodiversity, there may be a lack of baseline data or accepted mechanisms for measuring change or the impact of individual policies.

Nonetheless, and noting the methodological challenges, this section of the research seeks to draw judgement-based conclusions on a range of policies currently in place within Scotland’s economy, with a view to making assessments on how well different components of the SG are considered to be performing towards achieving the Environment Strategy ‘economy’ outcome.

Given the breadth of the Scottish economy, and the range of policies which impact it, the assessments are necessarily high-level at this stage. Where evidence gaps exist and judgements are made, these shine a spotlight on areas in which the SG may wish to target monitoring and evaluation resource to develop better informed and better evidenced policies.

3.2 Overall performance summary towards a net zero, nature positive and circular economy

3.2.1 Net zero economy

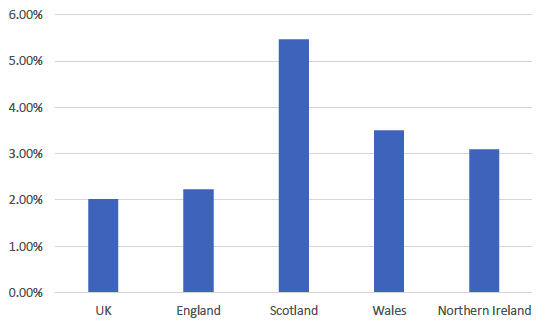

Although significant further economic transformation is needed, the net zero economy is relatively strong in Scotland in comparison to other UK regions as nations,[12] (Figure 1). Based on a narrow definition focusing on low carbon and renewable energy, Scotland’s net zero economy formed over 5% of the country’s economy in 2021, generating £8.7bn in turnover and employing over 28,000 people across Scotland.[13] Scotland currently being ahead of other parts of the UK is required, given its target for reaching net zero greenhouse gas emissions five years earlier than the UK: in 2045 compared to 2050.

Source: Office for National Statistics, Low Carbon and Renewable Energy Economy Survey

Based on the size of its labour market, Scotland has the highest concentration of green jobs in the UK.[14] In 2022, 3.3% of all job adverts in Scotland were for jobs that have a positive impact on the environment, up from 1.7% in 2021. This helped Scotland retain first place among 12 nations and regions of the UK in the Green Jobs Barometer developed by the consultancy PWC.[15]

Meeting the SG’s target to reduce emissions by 75% by 2030 (and by 90% by 2040) requires annual reductions of 8% from 2021 onwards, which is over 3 times the rate from 1990-2020.

Greatest progress towards Scotland’s net zero targets has so far been achieved in the energy sector. Emissions from electricity supply have fallen by almost 90% since 2010 due to a rapid rise in renewable generation which increased nearly threefold between 2009 and 2019. With ever higher generation of clean energy, new sub-sea links will channel excess supply from Scotland to England.

The emissions reduction pathway in Scotland’s updated Climate Change Plan aims to achieve zero emissions from electricity supply by 2029, which is six years earlier than the rest of the UK. At the same time, Scotland’s electricity supply will need to accommodate increased demand, particularly from heating (heat pumps), transport, or electrification in industry. Earlier this year, the SG published a Draft Energy Strategy and Just Transition Plan with more details on specific goals including the ambitions to deliver an additional 12 GW of installed onshore wind capacity and to achieve 8 to 11 GW of offshore wind capacity by 2030.[16] Specific targets are currently missing for renewable energy storage, albeit the pipeline of storage projects is robust.

The SG is aiming for the energy sector to spearhead a huge inward investment drive[17] with ambitions of creating an additional 20,000 jobs, increasing Scottish GDP by £4.2bn, boosting exports by £2.1bn, and adding up to £680m in additional government revenues per annum.[18] By 2050, nearly 80,000 are projected to be employed just in the low carbon energy sector as a result of the just energy transition.[19]

However, in its latest progress report, the Climate Change Committee (CCC) noted that, across a range of other areas largely devolved to SG – such as domestic heating, transport, land use and agriculture – Scotland has set relatively high ambition in cutting emissions but remains significantly off track from its own targets for the short and medium term, highlighting issues with policy delivery.[20] As summarised below, urgent, transformative action in these areas is required:

Domestic heating: The decarbonisation of heating is one of the most complex challenges facing the Government. Emissions from Scotland’s buildings have fallen only slightly over the past decade, highlighting the slow pace of change vis-à-vis the energy sector. The emission reduction pathway in Scotland’s updated Climate Change Plan sets out to reduce annual emissions from buildings to 2.6 MtCO2e by 2030, a 71% reduction on the sector’s emission in 2021.

The Government has laid out specific goals to meet this ambition that includes a commitment to zero emissions heating systems in all new builds from 2024, zero emissions heating systems to account for 50% of new systems installed each year by 2025, and 50% of all buildings to be converted to a low or zero carbon heating system by 2030.[21]

Transport: Emissions from transport account for the largest share of Scotland’s territorial emissions and are yet to start falling considerably over the last decade, reflecting a similar lack of progress relative to targets observed in the rest of the UK. Surface transport is the single biggest contributor to carbon emissions with a gradually increasing share from aviation and shipping. The emission reduction pathway in Scotland’s updated Climate Change Plan projects annual emissions falling to 6.5 MtCO2e by 2030, a 44% reduction on the sector’s emissions in 2021. Specific goals to meet this ambition include a 20% reduction on 2019 car kilometres, phasing out the need for petrol and diesel cars and vans by 2030 and petrol and diesel HGVs by 2035, ensuring that 30% of state owned ferries are low emission by 2032, decarbonisation of passenger rail by 2035 and the decarbonisation of flights within Scotland by 2040.

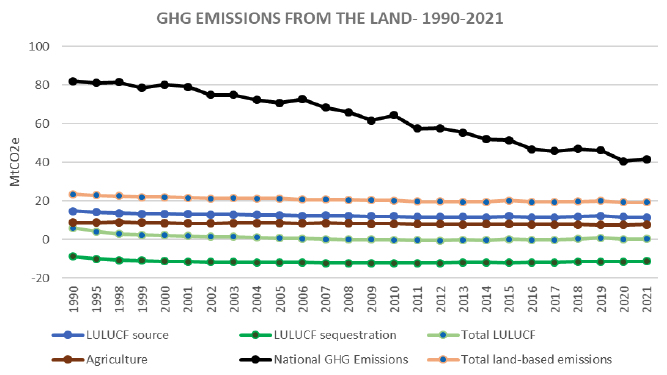

Land use and agriculture: Total net emissions in Scotland were 41.6 MtCO2e in 2021 and land-based emissions represented nearly half of this total, with agriculture at 7.8 MtCO2e and land use change and forestry at 12.3 MtCO2e. As shown in Figure 2, while total net emissions have approximately halved since 1990, land-based emissions have remained relatively constant over this period, highlighting the scale of the challenge ahead in reducing emissions in this sector. Soil health and widespread nature restoration, including woodland creation and peatland restoration, are key priorities for creating a net zero and nature positive economy. Woodlands constitute 19% of Scotland’s land area, which is higher than the UK average but lower than Europe at 37%.

Woodlands including commercial forestry and semi-natural woodlands sequestered 7.3 MtCO2e in 2021, including over 1.5 MtCO2e sequestered in broadleaved woodlands. Most woodlands in Scotland are commercial conifer plantations. New woodland creation is considerably off track to meet the SG’s own targets for 2024/25 of 18,000 hectares annually. Similarly, peatlands are contributing to significant carbon emissions with 80% of Scottish peatlands damaged and emitting 6.6 MtCO2e a year based on 2020 data. Current restoration targets and delivery are well below what is necessary.

Source: NatureScot, using figures from the NAEI for England, Scotland, Wales and Northern Ireland, 2023.[22]

Sectors like cement, iron and steel, chemicals, and the extraction and refining of oil and gas, alongside fuel supply, contribute one fifth of Scotland’s territorial emissions. The SG is aiming to reduce emissions from industry by 38% between 2020 and 2030, but policy in this area is largely reserved to Westminster. The CCC was not able to fully assess progress on decarbonisation of industry in its 2022 progress report for Scotland due to a lack of data, benchmarks and metrics, although there has been a slight improvement in energy efficiency over the past decade. Key gaps in reserved policy identified included a lack of medium to long-term plans from the UKG for industrial energy efficiency and electrification.

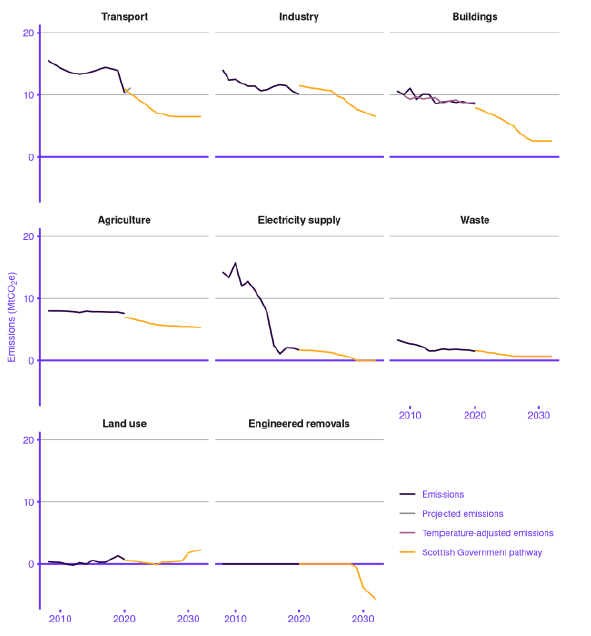

As shown in Figure 3, the Government is currently relying on carbon removal technologies to deliver its 2030 emission targets, particularly in industrial sectors, with an ambition of removing 3.7 MtCO2 every year from 2030 or an equivalent of removing 1.7 million cars from the streets. If this scale of emissions removal does not materialise to offset continued positive emissions forecast for sectors such as industry, transport and agriculture, then Scotland will miss its net zero targets unless further emissions reductions are secured in the aforementioned sectors. The UKG has also set itself a bullish target of 20-30 MtCO2 captured every year by the mid-2030s. Existing global capacity in carbon removal is currently far below the level expected to be needed by 2030 and beyond, meaning that the technologies are unproven at the required scale. Global commercial carbon capture capacity was just 45MtCO2 in 2022.[23] Bioenergy with carbon capture and storage (BECCS) captured 2 MtCO2 in 2022, of which less than half was stored,[24] while global direct air capture (DAC) capacity in the same year was just 0.008 MtCO2 per annum.[25] It is worth noting that there are currently no carbon capture or removal sites in Scotland, though the geography and the existing industry offer considerable potential. Specific proposals currently under development are awaiting approval and funding, posing an inherent risk of achieving rapid scale in these technologies within a short span of time. These removal technologies will only be effective in helping to achieve net zero if combined with very large reductions in emissions across the economy.[26], [27]

Source: Climate Change Committee, Progress in reducing emissions in Scotland 2022 report to Parliament.[28]

Just transition is a key objective for the SG and the recent budget allocated its first tranche of £20m towards projects in the North East and Moray as part of a £500m decade long Just Transition Fund. There is no universally agreed definition of a just transition but the Just Transition Committee (JTC), set up by the Government, is working with stakeholders across all economic sectors in better defining the concept of just transition and to inform practical policy design (their working definition is included in the ‘Definitions’ section, above). Although the JTC have so far focused primarily on the just transition to a net zero economy, these issues are also relevant to the transformations needed to achieve a nature positive and circular economy, and a holistic approach should be adopted when considering how to achieve these goals in a just way.

3.2.2 Nature positive economy

Nature positive refers to a world where species and ecosystems are being restored and regenerated rather than in decline. For the purposes of this project, we have defined a nature positive economy to be one that halts biodiversity loss by 2030 and creates an increase in and restoration of biodiversity levels after that point, in line with its definition in the international literature.[29]

The 2019 Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) Global Assessment highlighted the scale and pace of global biodiversity loss, identifying five direct drivers of biodiversity loss: changes in land and sea use, direct exploitation, climate change, pollution, and invasive alien species. The report also highlighted that these direct drivers result from a range of demographic and economic indirect drivers, including unsustainable production and consumption patterns.[30]

The James Hutton Institute (JHI) has recently published a report on how these indirect drivers apply in Scotland, categorising drivers as socio-cultural (i.e. the values people hold and how that makes them behave), demographic (i.e. population growth, patterns of migration and urbanisation, and education and local knowledge relating to the environment), political and institutional (i.e. public investment and subsidies, taxation, property rights, the political system, inequality, and local and global coordination), technological (i.e. new technologies for energy and agriculture, the externalities of this, and traditional local knowledge) and economic.[31] Three of the economic indirect drivers are international (relating to global trade, remittances, and tax havens) and hence outside of the scope of this project.[32] Their recommendations for addressing the remaining economic indirect drivers include:

- reforming regulations and incentives in sectors that affect land use and nature such as farming, fishing and forestry;

- reducing inequality and poverty to allow more of society to benefit from sustainably produced food;

- moving towards a zero-waste society and a circular economy to reduce Scotland’s global biodiversity footprint, including through certification schemes for Scottish produce;

- habitat restoration managed in a way that avoids exporting the negative biodiversity impacts via consumption of unsustainable alternatives (e.g. timber or food) from abroad, including by reducing overall material consumption in Scotland;

- ensuring that carbon markets contribute to improved biodiversity rather than worsening it; and

- adopting new indicators of sustainability and wellbeing instead of GDP.

While they do not assess Scotland’s progress on biodiversity, JHI advise that substantial change in values, behaviours, education, investment, production and consumption will be needed to reverse biodiversity loss.

Evidence on Scotland’s progress towards a nature positive economy is limited. It is more challenging to assess progress towards a nature positive economy than progress towards net zero, for several reasons. Biodiversity loss cannot be summarised as easily through a single indicator in the same way as greenhouse gas emissions. The evidence base can tell us which aspects of the economy negatively affect biodiversity, but it lacks the level of detail of the Climate Change Committee’s net zero research. It does not give a clear picture of the contribution of each sector of the economy to the problem nor has a clear plan been produced for what a nature positive economy will look like and how to get there.

The SG intends to explore options for measuring progress towards a nature positive economy through the further development of the Environment Strategy monitoring framework. The Initial Monitoring Framework, published in 2021, sets out an initial set of indicators for tracking progress towards the ‘economy’ outcome – including the Natural Capital Asset Index and Natural Capital Accounts, as described below. However, it noted that these indicators alone are not sufficient, and that further work will be undertaken to identify ‘meaningful and robust measure of progress towards this outcome’. It noted that this will include, for example, considering indicators relating to investment in natural assets, jobs in green industries and the scale of green finance.

In this section, we approach the task of evaluating Scotland’s progress towards a nature positive economy by exploring evidence on the key pressures on biodiversity in Scotland and how these relate to specific sectors of the economy. Further work is needed to explore, in greater detail, what a nature positive economy will look like in practice in Scotland, and how to measure progress towards this. However, the evaluation below provides a starting point for understanding Scotland’s progress towards a nature positive economy, which the SG can build on when developing the pathway for the ‘economy’ outcome and exploring indicators for the monitoring framework.

- Status of Scotland’s biodiversity

Existing evidence indicates that global trends of biodiversity loss are mirrored in Scotland. The 2019 State of Nature Scotland report concluded that there has been ‘no let up’ in the net loss of nature in recent decades, with the 2023 version of the report confirming that 11% of species in Scotland are threatened with extinction.[33] The draft Biodiversity Strategy summarises the evidence on ‘Scotland’s biodiversity crisis’.[34] For example, the Biodiversity Intactness Index indicates that Scotland has retained just under half of its historic land-based biodiversity, ranking in the bottom 25% of nations around the world.[35] Terrestrial and freshwater species abundance fell by 15% between 1994 and 2020 and saw a decline of 9% in the decade from 2010 to 2020.[36] The draft Biodiversity Strategy sets out ambitions for halting the loss of Scotland’s biodiversity by 2030, and restoring and regenerating biodiversity (and hence becoming nature positive) by 2045. Scotland’s consumption of imported commodities also has a significant impact on the natural environment overseas – this is the focus of a separate Environment Strategy outcome[37] and is not explored in detail through this project.

- Key pressures on Scotland’s biodiversity

According to the State of Nature report, key pressures on biodiversity in Scotland include the impacts of agriculture, development of the built environment, fishing, climate change and pollution.[38] This indicates some of the key economic sectors where transformation is therefore needed. The paragraphs that follow give an assessment of the available evidence on the biodiversity impacts of the Scottish economy – focusing on the above areas, as well as other key issues including protection of areas of nature, peatland restoration, forest cover, and invasive non-native species.

i) Protection of areas for nature

Protecting and restoring areas of land and ocean for nature will be an essential part of any mission to restore biodiversity and create a nature positive economy.[39],[40],[41] This will require a set of interventions to stabilise and then reduce the impact of agriculture and fisheries on the country’s land and oceans, and to increase the natural areas that are protected, restored and returned to nature.[42] Estimates of the proportion of land needing protection to achieve biodiversity goals vary, from the emerging consensus of conservation scientists to target protection of half of all land globally to other targets suggesting a minimum of 20% or 30% protection for a functioning landscape.[43],[44], [45] It is also important to ensure that protected areas are well managed to realise the full benefits. There is a substantial net benefit to protecting and restoring large areas for nature, in terms of nature positive and net zero missions and other social outcomes.[46]

The SG is aiming to protect 30% of Scotland’s land and seas for nature by 2030 under the 30x30 goal,[47] which is one of 23 targets of the Kunming-Montreal Global Biodiversity Framework, adopted by 196 states at the COP15 conference in 2022.[48] In practical terms, Scotland’s land area is 77,910km2, of which 18% (c. 14,000 km2) is currently protected and a further 5% (c. 3,900 km2) is national parks.[49] Scotland’s seas cover an area of 462,315 km2 and Marine Protected Areas cover 37% of this (228,118 km2)[50], albeit not all of these areas have the fisheries measures in place at present to ensure that they are well managed. This shows that a major increase is needed in the protected land area between now and 2030. The biodiversity impact of this protection will also depend on how effectively it is implemented; in marine areas, for example, biodiversity outcomes are still at low levels (albeit with some recovery) in spite of a higher rate of notional protection.

ii) Peatland restoration

Scotland’s extensive peatlands are in particularly urgent need of restoration to meet both the net zero and nature positive missions. Their condition is poor, with 80% being degraded, and as a consequence they are a large source of emissions rather than being a net carbon sink.[51]

iii) Forestry

Scotland is among the most deforested countries in Europe[52] and had lost most of its woodland by 1800[53] or earlier,[54] but the country has also made significant progress in increasing forest cover in the past century, from 4.5% in 1905 to 19.1% in 2022.[55] Forest cover in Scotland remains substantially lower than many EU countries, where the average forest cover is 39% and 20 member states have forest cover greater than 29%.[56] Not all forest cover is of equal benefit to biodiversity. Certain types of mixed or semi-natural woodland are likely to be of high biodiversity value, whereas areas used for commercial forestry do not necessarily provide the same level of biodiversity benefit. Nonetheless, given the potential for forests to contribute to the nature positive mission, and to capture and store carbon for net zero,[57] there is a need for further ambition to restore forest cover in Scotland to move closer to the EU average.

iv) Agriculture

More than 70% of Scotland’s land area is used for agriculture, making it the predominant land use in the country.[58] Of this agricultural land, 55% is used for rough grazing, 23% is grass, 10% is used for crops or fallow, 10% is woodland, and 2% is other land.[59] Around 85% of agricultural land in Scotland is in Less Favoured Areas, with lower productivity for agricultural uses.[60] The capability of Scotland’s land is an important constraint to what sort of agriculture is possible in different parts of the country: while arable land (8% of area) can support a wide range of crops and a further proportion of Scotland’s land (20%) can support mixed agriculture with a moderate range of crops, the agricultural potential of large parts of the country is limited to rough grazing (51%) or improved grassland (18%).[61] Among the largest crops by area in Scottish agriculture, barley and wheat, the majority of output is used either for whisky production or animal feed.[62] Food production and supporting biodiversity are not mutually exclusive, but given the finite amount of land available for uses such as conservation and forestry in Scotland, a reduction in the land footprint of agricultural uses such as livestock and dairy and non-food production could allow more land to be used for biodiversity while maintaining a secure food supply.

Agriculture is one of the largest contributors to biodiversity loss, through its direct effects on nature (intensive use of soil and land, pollution via pesticides and fertilisers) and through the use of land that could otherwise support higher biodiversity, for example as semi-natural habitats or under conservation measures.[63],[64] In particular, increasing intensification of agriculture has driven biodiversity losses in Scotland, a trend which had some forms of impact for more than a century but has been more pronounced in the past 50 years.[65] Certain forms of agriculture such as meat and dairy production have a particularly strong impact on emissions and land use requirements, as they are inherently less efficient at converting energy into calories.[66] On the other hand, certain lower intensity forms of farming can benefit biodiversity: for example, a certain amount of grazing in upland areas can prevent the negative biodiversity effects of undergrazing.[67] A 2011 study estimated that 40% of Scotland’s agricultural land is used for ‘High Nature Value’ farming (i.e. where rough grazing occurs on more than 70% of the farmed area and livestock density per hectare of forage is below a certain threshold).[68] These forms of farming are more likely to support biodiversity, albeit it is unclear whether this is sufficient to achieve an increase in biodiversity relative to the status quo, as required for a nature positive economy. The same 2011 study estimated that livestock-focused forms of farming in Scotland (crofting, sheep systems, beef cattle systems, combined sheep and cattle systems) were likely to make up the bulk of the country’s ‘High Nature Value’ farming whereas other forms (arable systems, dairy systems, mixed arable and horticulture systems, horticulture systems, pig systems, poultry systems) were unlikely to meet the ‘High Nature Value’ definition because they were managed very intensively in the vast majority of cases.[69]

Data from the Natural Capital Asset Index 2023 shows that fertiliser use in Scottish agriculture fell by 31% between 2000 and 2010, before remaining roughly constant until 2019, and falling slightly further in 2020 and 2021.[70] In the same period, pesticide use in Scottish agriculture rose significantly during the 2000s, was on average 32% higher in the decade from 2008 to 2017 relative to its 2000 baseline, but has declined slightly to a level 23% above its 2000 baseline during the period from 2018 to 2020.[71] The abundance of farmland bird species in Scotland rose by 24% between 2000 and 2008, but has since fallen steadily and as of 2021 stood at a level 13% above its 2000 baseline.[72]

The complex relationship between Scottish farming and biodiversity poses a challenge for assessing the impact of the sector over recent decades and what a hypothetical nature positive agriculture sector would look like. There is clear evidence that intensive agriculture is a key driver of biodiversity loss in Scotland, and that management interventions such as agri-environment measures and regenerative farming approaches can mitigate some negative impacts on biodiversity. However, there is a need for further evidence on the impact of existing farming practices on biodiversity – and on the broader land use transformations needed to achieve multiple goals for climate, nature and food production – to give greater clarity to SG policies on the sector’s contribution to the nature positive mission. The 2022 Vision for Agriculture sets an ambitious direction of travel and acknowledges the need for change in the sector, but frames farming almost exclusively in terms of its positive contribution to biodiversity.[73] The draft Scottish Biodiversity Strategy presents evidence of a substantial decline in biodiversity on land and the effects of agriculture as a driver of this,[74] and aims to achieve farmland practices that result “in a substantial regeneration in biodiversity, ecosystem and soil health and significantly reduced carbon emissions while sustaining high quality food production” by 2045.[75] However, it is unclear from reading the strategy as a whole whether the outcomes targeted will be sufficient to transform the agricultural sector’s impact to the extent that biodiversity decline is effectively reversed. The post-Brexit replacement of the Common Agricultural Policy (CAP) will be a critical tool in putting Scotland on track to meeting its biodiversity goals.

v) Aquaculture

Aquaculture is an important primary sector of the Scottish economy, with farmed salmon making up over one third of national food exports in 2021 following strong growth in the previous decade.[76], [77] The sector has the potential to form an important source of sustainable food supply in a nature positive Scotland, with the caveat that it will have to overcome several issues with its current environmental impact.[78] In the salmon farming subsector these include disease management among farmed fish such as sea lice (which have been shown to have negative spillover effects on the adjacent marine ecosystems),[79] the use of pesticides and antibiotics with knock-on effects to adjacent areas,[80] an increased risk of eutrophication arising from the nutrient input from fish farms,[81] sourcing sustainable feed for farmed fish that doesn’t put further pressure on wild fish stocks or land use,[82] and pollution from the solid waste arising from farmed fish.[83] There appears to be an evidence gap on the environmental impact of finfish farming in Scotland (especially in light of the recent growth of the subsector).[84]

vi) Fisheries

As in many countries, Scotland’s fisheries have been subject to overexploitation in past decades, leaving stocks at reduced levels[85] and having negative knock-on effects to the abundance of other marine species.[86] Scotland’s Marine Assessment 2020 took a detailed look at the available data on different commercial fish stocks.[87] The proportion of key commercial stocks subject to overfishing (where mortality was above the level required for maximum sustainable yield (MSY)) was high, albeit it fell slightly from 54% in 2016 to 46% in 2018. There was substantial variation by species, however: while hake and herring stocks made some recovery in recent decades, stocks of whiting and cod stocks did not. Between 1985 and 2016 there was some recovery with increases in abundance among demersal species (using data that covers only the 9 to 11 most commercially important species) in the Greater North Sea and Celtic Seas, from a very low baseline. There were also increases in the abundance of pelagic fish species in the same seas over that period.[88] The National Performance Framework indicator for the proportion of commercial fish stocks that are being fished sustainably (an average of stock and fishing mortality metrics for certain commercially important fish species) has improved substantially since the 1990s, from an average of 33% for the period 1991-2000, to an average of 63% in the decade from 2011 to 2020, an average of 65% from 2016 to 2020, and a level of 72% in 2021. There is still much room for improvement, given that 28% of the most important commercial stocks were not being fished sustainably (i.e. were being overfished) in 2021.

It is important to note that the data referenced above focuses on a small number of economically important species. As noted in a recent survey of evidence on Scottish nature, “very little is known about the vast majority of unmonitored and unregulated fish populations.”[89] The 2020 Marine Assessment found no trend changes in the diversity of deep-sea fish in the past two decades, albeit with substantial data gaps in certain areas.[90] The same assessment could not discern a trend for the wider fish community (a larger sample of 167 species including many non-commercial fish) due to lack of evidence, albeit the available data suggested an improvement in the proportion of large fish in Scottish waters and a reduction in species richness and diversity in offshore waters.[91]

An indicator of the mean numbers of 11 seabirds in Scotland has fallen sharply in recent decades, so that the breeding numbers in 2019 were at 49% of their 1986 level.[92] Fisheries are one of the key drivers of this change (together with climate change and invasive non-native species) and the reduction in prey due to fishing is considered to be a high threat to six of the 11 species measured by the data.[93]

vii) Pollution

Pollution can negatively impact biodiversity through chemicals and waste deposited in the natural environment and through air, light and noise pollution. The 2019 State of Nature report noted that the farming, transport, energy and industry sectors were key sources of pollution and that pollution continues to have an impact in Scotland, in spite of some progress since the 1990s.[94] While the levels of key air pollutants have fallen significantly in recent decades, there is continued pressure on nature from new agrochemical and pharmaceutical products, plastic pollution, and diffuse pollution arising from the forestry and agriculture sector, roads and urban areas.[95] Pollution has had an impact on the Scottish distributions of lichen, more than half of which have declined since 1980, albeit there has been some recovery from the high levels of sulphur deposition observed in the 1970s.[96] Monitoring by SEPA found that in 2020, 66% of Scotland’s water environment was in good or better condition based on a combination of water quality, flows and levels, physical condition and barriers to fish migration, an improvement from a figure of 63% in 2015.[97] The proportion of river length classed as polluted declined from 7% in 1998 to 3% in 2018.[98]

viii) Invasive non-native species and climate change

According to Great Britain level indicators for Invasive and Non-Native Species (INNS) cited in the 2023 State of Nature report, there has been an increase in the spread of existing INNS and no reduction in the establishment rate of new INNS since the 1960s, meaning that the impact and threat from INNS is intensifying significantly in Scotland.[99] Climate change, which will continue to put direct pressure on biodiversity as it worsens on a global scale, is also reinforcing the negative impact of INNS in Scotland.[100]

Ultimately, transitioning to a nature positive economy will mean ensuring that the economy’s demands on nature do not exceed its supply. The 2021 Dasgupta Review on the Economics of Biodiversity emphasised that the economy is embedded in nature i.e. it is fundamentally dependent on the resources and services nature provides, and its capacity to absorb wastes, including greenhouse gas emissions.[101] The Review concluded that humanity’s demands on nature currently far outstrip its capacity to supply, eroding nature’s capacity to meet people’s needs into the future and to sustain other life. For example, globally, while produced capital per person doubled between 1992 and 2014, the stock of natural capital per person declined by nearly 40%.

In Scotland, the Natural Capital Asset Index measures the capacity of Scotland’s terrestrial ecosystems to provide benefits to people. Although the index has improved slightly over the past 20 years, a back-casting exercise highlighted that this followed a significant deterioration between the 1950s and 1990s.[102] The Environment Strategy monitoring framework therefore notes that ‘natural capital in Scotland is at low levels when considering long term trends’.[103] The biggest declines in the NCAI between the 1950s and 1990s were in moorland, grassland, cropland and coastal ecosystems. A NatureScot study attributes these declines to a range of factors, including peatland drainage and bracken encroachment on moorland; afforestation of grassland; loss of hedgerows and excess nitrogen application on crop land; and pollution of coastal ecosystems.[104] To restore Scotland’s natural capital and reverse past declines, significant economic transformation will be required – including investment in and sustainable management of Scotland’s natural capital assets by land-based and marine industries. As noted above, Scotland’s consumption of imported products also places unsustainable demands on natural capital in other countries, and this is a focal point of another Environment Strategy outcome.

There is growing understanding of the economic risks posed by the degradation of nature. In a 2020 study, the World Economic Forum and PwC estimated that $44 trillion of economic value generation – over half the world’s total GDP – is moderately or highly dependent on nature and its services and, as a result, is exposed to risks from nature loss.[105] This estimate was updated to $58 trillion in a 2023 PwC analysis.[106] While in the broader sense, all economic value generation is ultimately dependent on nature, these studies highlight the reliance of a wide range of economic sectors on nature, and the material risks posed by its decline.

The importance of nature to Scotland’s economy is illustrated by the 2023 Natural Capital Accounts, which estimate that Scotland’s stocks of natural capital have an economic value of £230 billion and provide an annual flow of benefits to society worth £15 billion.[107] Drawing on this data, the Environment Strategy monitoring framework includes an indicator on the annual flow of benefits from Scotland’s natural capital, excluding fossil fuels: estimated at £4.0 billion.[108] However, as emphasised in the Natural Capital Accounts, these estimates do not cover all services from nature, and should therefore be interpreted as a partial or minimum value of Scottish natural capital. The asset values are also not an absolute "value" of nature, since ‘its collapse would precipitate our own, implying infinite value’.[109] It is important to recognise that natural capital stocks and flows may show different patterns in the short term, e.g. when a resource is being extracted at unsustainably high levels, creating a large temporary flow of value but a reduction in the stock of natural capital and its capacity to produce flows of value in future years.

3.2.3 Circular economy

Recent estimates suggest that Scotland’s economy is only 1.3% circular – meaning that only 1.3% of the resources that Scotland uses are circulated back into the economy after use, and Scotland’s economy relies almost exclusively on virgin materials. By comparison, the global economy is 8.6% circular and the Netherlands’ economy is 24.5% circular.[110]

Scotland’s annual consumption of virgin materials (around 21.7 tonnes per capita), its material footprint, is nearly double the global average. The rate of domestic resource extraction per capita, at 22.8 tonnes, is more than four times the UK average - largely owing to the extraction of fossil fuels in the North Sea. Addressing the question of future North Sea oil and gas extraction is of significant import both at the national and international level. The 2023 Circularity Gap report for Scotland notes that ‘while high per capita extraction and consumption rates are common for a high-income economy, Scotland rests near the top of this classification.’[111]

The report also highlights that, since Scotland represents 0.073% of the world’s population, yet consumes 0.1% of the globe’s virgin material use, ‘the Scottish economy is largely driven by overconsumption’. Scotland’s large material footprint stems from significant levels of waste generation; reliance on fossil fuels for transport and heating; and geographic, demographic and climatic factors, with Scotland’s low population density meaning that materials needed for infrastructure, amenities and services are used less efficiently.

Scotland’s large material footprint is strongly linked to Scotland’s consumption of imported materials and finished products, which accounts for more than two-fifths of its total material consumption. This is also reflected in Scotland’s consumption-based carbon footprint, which exceeds territorial emissions by 42%, meaning that much of Scotland’s carbon footprint results from emissions embedded in imports.

Focusing specifically on waste management, the Government set a range of targets, including a 15% reduction of all waste by 2025 against 2011 levels; a 33% reduction of food waste by 2025 on 2013 levels; a minimum of 60% recycling of all household waste by 2020; a minimum of 70% recycling of all waste by 2025; a maximum allowance of 5% of all waste to reach landfill by 2025 and a ban on all biodegradable waste going to landfill by 2025. The Government is currently underperforming on all of these targets while missing the 2020 household waste recycling target, acknowledging that “it is unlikely that waste and recycling targets or emissions goals will be met in full without large-scale, and rapid system change”.[112]

The recently published Circular Economy Bill will provide the necessary legislative underpinnings for the Government to implement more systemic solutions to the challenge. The Government has also published a 2025 route map document, laying out some of the key interventions and actions it is considering which have since been consulted upon.

Historically, measures such as the carrier bag charge and ban on plastic cotton buds have had a positive impact with a significant reduction in their reported use across the country. Scotland has also met its EU targets for limiting the amount of biodegradable waste going to landfill and enhanced recycling of construction and demolition waste. Furthermore, a £70m local authority recycling improvement fund to improve reuse and recycling practices; banning the supply and manufacturing of some of the most environmentally damaging single-use plastic items; a plastic packaging tax and other measures in reducing waste from sectors like textiles and construction have all been introduced in the past few years.

The initial consultation on the route map to 2025 highlighted several new measures across different packages, targeting specific areas ranging from household recycling to circular construction practices. The approaches suggested in the route map are comprehensive but governance and delivery will pose significant challenges – as is evident with the attempts to roll out the deposit return scheme which has already been deferred by several months.

3.2.4 Conclusion on performance towards a net zero, nature positive and circular economy

As demonstrated in the section above, Scotland’s progress towards a net zero economy is a mixed picture, with some progress accompanied by several significant gaps. The country’s net zero targets are ambitious relative to the rest of the UK. The evidence on progress by economic sector, drawing primarily on the more detailed assessment by the CCC, is as follows:

- Emissions from electricity supply are being sufficiently addressed, with a sharp reduction recorded since 2010.

- There has not been much reduction in emissions from buildings in the past decade, but a major fall in emissions will be required in the sector between now and 2030. Although there have been some encouraging policies in this sector, they are not yet sufficient to deliver the reduction in emissions needed according to the CCC’s recent progress assessment.

- Scotland is falling behind on transport decarbonisation, especially when it comes to the distance travelled by cars and aviation, with more ambitious policies needed to achieve 2030 targets.

- More progress is needed in agriculture and land-based sectors, with the CCC identifying a particular need for low-carbon agriculture policy and a shift to healthier diets. Peatland restoration and tree planting are short of the targeted rates needed for net zero.

- There is a lack of data to give a clear picture of progress in decarbonising industry, but a significant further reduction in emissions will be needed by this sector, in which many important policy levers are reserved to the UKG.

- Engineered removals are forecast to play a substantial role in achieving net zero, but at present no removals are occurring in Scotland. Although this is largely a devolved policy area, there is a significant risk of not scaling up capacity quickly enough to meet net zero targets.

Progress towards a nature positive economy cannot be assessed with the same precision as in the case of net zero, but the evidence in the previous sections does allow us to make a broad assessment of whether the key drivers of biodiversity loss are being reduced and whether metrics of biodiversity are getting better or worse. This broad assessment suggests the following:

- Biodiversity metrics

- Nature in Scotland is starting from a depleted baseline, with biodiversity intactness being among the bottom 25% globally and half of Scotland’s historic land-based biodiversity having already been lost. There have been some promising signs of modest improvement since the 1990s but some key drivers of biodiversity loss are still getting worse and significant transformation is needed across the economy to become nature positive.

- Indicators of species abundance continue to show a mostly negative trend. Terrestrial and freshwater species abundance fell by 15% between 1994 and 2020, with a decline of 9% in the past decade alone. There has been some improvement in farmland bird abundance since 2000, but this has varied significantly by species. There has been a large decline in the abundance of 11 seabird species, which fell by 51% between 1986 and 2019. As mentioned below, key commercial fish stocks exhibit a mixed picture, with some stocks having recovered since the 1990s and others remaining at very low levels.

- Drivers of biodiversity loss (as defined by the 2019 IPBES Global Assessment)

- In terms of land and sea use change, there has been a significant increase in forest cover over the past century but the present level is still well below EU average. Protected areas on land will need to increase substantially (from 23% to 30% of Scotland’s land area) to meet the 2030 target for biodiversity. Large areas of seas are designated as protected (38% of Scotland’s territorial waters), but this hasn’t always translated to better condition in these areas.

- Pressure from resource use and exploitation appears to remain high in key nature-related sectors. The impact of farming on biodiversity has worsened with intensification in the past 50 years, though the impact varies significantly between intensive farming (e.g. arable, dairy, horticulture, poultry, pig farming) and higher nature value forms of farming (low intensity livestock, primarily in areas of lower land capacity). Agricultural policies have become somewhat more aligned with biodiversity goals but this has been insufficient to halt biodiversity decline, suggesting that realignment measures to date have not been sufficiently ambitious. Fisheries have been subject to overexploitation in past decades. The proportion of key commercial stocks being overfished remained high at 28% in 2021, but has fallen substantially from 67% in the 1990s. There has been some recovery of abundance in commercially important fish species since the 1980s but key stocks such as cod and whiting remain very low relative to levels several decades earlier and discards of these species have not fallen.

- There has been some reduction in air pollution since the 1990s but pollution from agriculture and forestry (via pesticide and nutrient run-off), transport (contaminated drainage and acid pollutants in the air) and plastic pollution (including in seas and soils) are still present, and the condition of the water environment is improving only slowly. Since 2000, fertiliser use has fallen but pesticide use has risen.

- The remaining two direct drivers of biodiversity loss, climate change and invasive and non-native species, are increasing and working in synergy.

Evidence on progress towards a circular economy suggests significant further action is needed to move Scotland closer to its peers:

- Scotland’s economy was estimated to be 1.3% circular in terms of its resource use in 2022, well below the level of circularity estimated for the global economy (8.6%) and the leading economy, the Netherlands (24.5%).

- The rate of domestic resource extraction per capita, at 22.8 tonnes, is more than four times the UK average and relatively high among high-income economies, largely owing to the extraction of fossil fuels in the North Sea.

- Waste management and reduction targets are ambitious in Scotland but performance is behind on these and large-scale, rapid system change is needed to hit these targets.

3.3 Wider economic model and transformational change

Before reviewing the economic policy levers currently used by the SG to drive progress towards a net zero, nature positive and circular economy, it is necessary to reflect on the wider economic model and policymaking framework as they currently exist, and how these affect Scotland’s ability to achieve these missions.

There are a number of features of the wider economic model that apply in Scotland and other advanced economies that will hinder efforts at rapid transformational change to reduce emissions and restore biodiversity. Permanent, continual growth in economic production is an embedded feature of capitalist economies and poses a challenge to addressing the aforementioned environmental crises. Economic output and similar measures such as GDP are highly correlated with energy, greenhouse gas emissions and material use and there is much debate over whether it will be possible to decouple these factors from growth to the extent that a net zero, nature positive and circular economy can be achieved while still continually growing the economy.[113], [114] This suggests that a move away from prioritising economic growth may be necessary to achieve the three missions, but this will be challenging to achieve in an economic system that is based on growth and where many interests benefit economically from continued growth without having to absorb its full costs yet. One approach to achieving this would involve shifting to an economic system that is growth-agnostic, targeting improvements in wellbeing rather than GDP. This could allow a just transition to achieve the three missions while enhancing people’s wellbeing. An economy that is not shaped with growth alone as the goal can still be the kind of wellbeing economy that the SG aims to foster.[115]

The Dasgupta Review, commissioned by HM Treasury, emphasises that conventional economic thinking sees the environment as external to the economy, rather than framing the economy as embedded within the environment, and the former view can encourage suboptimal policies in response to environmental crises.[116] The Review emphasises that economies are underpinned by finite but regenerative natural resources and ecosystem services, so that a truly sustainable economy is one that fully accounts for its impacts on nature and consciously limits its demands on nature until they balance what nature can sustainably supply. The fact that the economy is embedded in the natural environment suggests that policies sufficient to achieve a net zero, nature positive and circular economy will need to prioritise these missions first and foremost: it will not be enough to focus narrowly on the subset of green interventions that are profitable or where nobody loses out.

Climate and nature are typically not factored into market prices, meaning that decision-making that prioritises financial return does not take these factors into account. Neither do market prices capture the tipping points inherent in the natural environment that could create runaway negative impacts if reached,[117] such as changes to ocean currents or permafrost thawing.[118] This is one of the reasons why the existing economic model drives continued activity and even growth in a number of highly environmentally destructive economic activities that are profitable in a narrow financial sense and whose producers and consumers do not bear their full environmental costs, such as oil and gas extraction, fast fashion, disposable products and packaging and unnecessary air travel. Various policy responses to environmentally harmful economic activity are discussed in the sections that follow, including the use of more holistic natural capital accounting or eco-labelling to more fully incorporate these costs and benefits into decision-making, the use of taxation to discourage certain activities or the use of regulation to prohibit them. Similarly, our existing economic system and market mechanisms have proved incapable of reducing the damage of excessive consumption among the very wealthiest, with the top 0.1% of income earners worldwide being responsible for 6% of total global growth in carbon emissions between 1990 and 2015 and emitting 45 times as much per capita as the global average person in 2015.[119]

Within our present economic model, certain policy frameworks and paradigms have become dominant in recent decades, which also pose challenges to achieving a just transition to a net zero, nature positive and circular economy. The dominant neoliberal economic policy approach that emerged in the 1980s and has remained prominent tends to favour the market sphere of an economy, which is seen as efficient, over delivering economic activity in the public sector, which is characterised as inefficient. This has created a legacy of privatisation which has made it more difficult for the SG to exert direct control over aspects of the economy such as housing energy efficiency, public transport and power generation, even in cases where policies have recently been reversed such as Right to Buy and the nationalisation of ScotRail. Given the rapid transformation needed to respond to the climate and biodiversity crises and the lack of profitability of some of the investments needed, the public sector is likely to be required to take a more active role in the Scottish economy (in a configuration more similar to the mid-20th century economic model than the neoliberal model) to achieve the three missions. This may come into conflict with the prevailing ideas that have taken root under the neoliberal economic paradigm, such as the presumption that private firms should not be subject to significant regulation, that taxation should be kept low or that delivery of key economic services by public sector organisations is inherently inefficient. Neoliberal economics has also created a deep-rooted presumption in many advanced economies that one of the primary functions of governments is to encourage private investment (through policy measures that subsidise these investors with public funds, socialise their investment risk or reduce the investors’ social or environmental obligations). Allowing such an approach to dominate in the transition to net zero, nature positivity and circularity would put a just transition at risk, by directing both the decision-making power over what kind of transition occurs and the financial returns from the subsequent investments to a small number of investors rather than the public at large. While there are signs of this way of thinking being challenged in recent years through initiatives such as the Scottish National Investment Bank, the SG will need to carefully consider the roles of public and private delivery models in achieving a just transition and how the shortcomings of previous neoliberal economic policies can be avoided.

The policy levers covered by the subsequent assessment and recommendations are not on their own sufficient to transform every aspect of the economic system in Scotland. Nonetheless, if the recommendations are pursued they could have some impact in counterbalancing the tendencies within the current economic and policymaking systems that continue to contribute to the climate and biodiversity emergencies.

3.4 Reviewing and assessing policy levers

The economic transformations needed to tackle the climate and nature emergencies will require a whole-of-government approach, with strong alignment across a range of public policy levers. However, as a devolved nation, Scotland does not retain full control of its economic policy (e.g. tax, monetary policy, specific aspects of industrial policy which are retained competencies of UKG). Furthermore, since Brexit, the UKG has not matched the scale of public investment received by Scotland from the EU – in particular through the UK shared prosperity fund which is estimated to fall short by £337m over the next three years in comparison to the EU’s structural funds.

Noting these constraints, this sub-section of the research provides a high-level overview and synthesis of a very broad range of policy levers currently deployed or proposed in Scotland. The synthesis of existing policies is valuable in itself by providing a clear mapping of the extensive and overlapping areas of public policy through which the economy and the environment link together.

Wherever existing data and evidence allow, the research goes further by presenting an assessment of the success or expected sufficiency of the policies set out. However, in many areas this is simply not feasible due to a lack of evidence, or indeed, mechanisms, for measuring success. In these areas, the research team uses its own judgement to make assessments where reasonable. Where such assessments are not possible, the lack of evidence enables the SG to identify areas for further research and investigation – or indeed, consultation, where political or economic opinion may be an essential factor in policy making – for example, in areas of contention such as the ability for markets to solve problems, or the need to trade off pace of change considerations, or micro vs macro impacts on communities and the national economy.

Nonetheless, it is the view of the research team that delivering the Environment Strategy ‘economy’ outcome will require all of these levers to point in the same direction while matching the urgency of the climate and nature emergencies.

3.4.1 Policy lever domains

In the box below, we set out a list of policy lever ‘domains’ within which we group known policies relevant to the ‘economy’ outcome.

Policy lever domains

Below, we set out a list of policy lever ‘domains’ within which we group known policies relevant to the ‘economy’ outcome.

I. Public investment (including investment designed to leverage private investment)

II. Public procurement

III. Direct and indirect taxes

IV. Regulation and legislation

V. Industrial product and process standards

VI. National planning framework

VII. Research and innovation

VIII. Enhancing human capital through upskilling, retraining

IX. New forms of ownership to distribute economic value fairly

These levers are not exhaustive because of the aforementioned breadth of policies which impact both economy and environment, but capture some of the key, priority policy levers that the SG could deploy. In the analysis that follows we review existing policies under the headings of these domains for each of the three missions of net zero, nature positive, and circular economy. It is important to note, that not every domain sits under each of these missions.

As mentioned, where possible, we also evaluate these levers in terms of their efficacy and sufficiency in driving the transition to a net zero, nature positive, circular economy i.e. whether they provide sufficient economic signals and impact to put Scotland on track to meeting its short and medium term targets. We also evaluate where possible how policy levers help to deliver the broader socioeconomic outcomes required of a Just Transition, such as green job creation, local economic development and fair distribution of costs and benefits.

A preliminary observation that can be made here is that a lot of these levers have been used more effectively towards climate mitigation and net zero with limited interventions so far on the nature positive and circular economy missions, albeit that new legislation and policy is currently under development in relation to the latter two missions.

3.5 Current use of levers for a net zero economy

With an ambitious target of reaching net zero by 2045, Scotland will require an economy-wide transformation. The aforementioned economic policy levers will need to be strongly aligned to trigger the necessary change in private investment and consumer behaviour whilst developing existing and building on emerging low carbon industries and sectors. In the following section, we discuss each of these levers that SG may be able to utilise. The recommendations in Section C then delve deeper into ways the Government can use these levers more effectively.

3.5.1 Public investment

Public investment and private finance

The SG allocated £4.4bn (or 8% of the total budget) in December 2022 to the net zero, energy and transport portfolio.[120] Just over half of it, £2.5bn, is capital spending, with the rest largely contributing to the day-to-day expenditure of the Government. Extrapolating the CCC’s recommendation of spending 1-2% of GDP on climate action, SG’s investment would fit within that range: £4.4bn is equivalent to 2.1% of Scotland’s estimated 2022 nominal GDP of £210.7bn.[121] However, some sectors like transport and buildings are under-funded, while energy faces a heavy reliance on private investment without significant imposition of additional conditionality obligations, such as investing in worker skills, local supply chains and/or in particular communities with the aim of securing wider socioeconomic outcomes.[122] ScotWind is a good example of an organisation that has conditionality imposed to its private investment to support local supply chains, but more could be done in future leasing rounds.

SG’s own estimate reveals emissions of 8.8m tonnes of carbon dioxide equivalent (MtCO2e) that are attributable to the 2023-24 budget, based on the Government’s Environmental Input-Output model.[123] The Fraser of Allander institute has challenged some of the carbon impact assessment calculations and the Government has acknowledged the limited value of these estimates in informing public policy choices.[124] However, such attempts at calculating the environmental impact of budget decisions are useful and a SG and Parliament Joint Budget Review has been set up to improve the exercise.

Public investment is informed by the Government’s Infrastructure Investment Plan (IIP) (2021-2026) which provides the strategic framework for the next 5 years’ pipeline of projects and programmes – with expected value of around £32 billion over 5 years to attract inward investment. For instance, the Government has identified renewable hydrogen production as a new market opportunity with an ambition to make “Scotland a leading nation in the production of reliable, competitive and sustainable hydrogen”.[125] The first tranche of investment focuses on driving technological progress and advancing innovation and cost reduction within the emerging sector. Concurrently, the Inward Investment and Capital Investment plans and Scotland’s Green Investment Portfolio operate alongside the IIP with the primary aim of attracting private investment in sectors where Scotland has a competitive advantage (e.g. energy transition, transport decarbonisation).

The Government acknowledges the limitations of public investment in achieving its outcomes and is inviting greater amounts of private capital.[126] The Scottish National Investment Bank, for instance, is already playing a key role in crowding-in and leveraging private investment. Capitalised with £237m for 2023/2024, the bank is providing crucial capital to a variety of businesses, both small and large, alongside private funds managing natural assets in Scotland sustainably.[127] The bank has a clear mandate to offer capital to projects that carry risks which are beyond the appetite of private capital, in other words, which are not deemed to generate high returns in a short period of time. However, the investment portfolio remains relatively small, at £415m (alongside an additional £680m from third party investors), compared to the tens of billions required for achieving SG’s goals for a net zero, nature positive, circular economy.

Public funding is useful in the early delivery of policy when private capital is harder to secure, and there are also scenarios and objectives where continued public investment is most appropriate. In that context, the SG has allocated comparatively (i.e. to the rest of the UK) higher amounts of public investment in growth areas such as electric vehicle charging, active travel infrastructure and natural capital markets. However, there are a few important areas where public investment is significantly lacking in Scotland, as outlined below.

Public investment in transport

Emissions from transport account for the largest share of Scotland’s territorial emissions and have fallen only very slightly in the past decade. In 2021, emissions from transport were 11.6 MtCO2e (27.9% of Scotland’s territorial emissions), compared to 14.9 MtCO2e in 2009 (or 24.1% of Scotland’s territorial emissions in 2009).[128] [129] The main sources of Scottish transport emissions include passenger road transportation (42%), heavy and light goods vehicles (25%), domestic maritime transport and shipping (14%), international aviation and shipping (14%), and domestic aviation (5%).[130]

The emission reduction pathway in Scotland’s updated Climate Change Plan sets out to reduce annual emissions from transport to 6.5 MtCO2e by 2030, a 44% reduction on the sector’s emission in 2021. Specific goals to meet this ambition include a 20% reduction on 2019 car kilometres, phasing out the need for new petrol and diesel cars and vans by 2030 and petrol and diesel HGV’s by 2035, ensuring that 30% of state owned ferries are low emission by 2032, decarbonisation of passenger rail by 2035, and decarbonisation of flights within Scotland by 2040.[131]

Scotland has made significant investments per capita on active travel, buses and rail decarbonisation but is underestimating the associated behaviour change necessary in reducing personal vehicle mileage, thereby risking its ambitious 2030 target of reducing car kilometres by 20% against a 2019 baseline. Public transport in Scotland – and bus services in particular – has struggled with increasing passenger fares and declining patronage. Lack of reliable and affordable bus provision is forcing many to use cars and has negative distributional consequences. On the other hand, the Government has invested billions in road infrastructure that is not compatible with the Climate Change Plan targets.

The SG has made small but strategic investments in supporting the uptake of electric vehicles (EVs) with a mix of grants, interest free loans, match funding for public EV charging and funding bus operators to electrify their fleet. The Government is also investing billions in building new roads and upgrading existing road infrastructure with high direct and indirect emissions but there are no clear plans for mitigating them.

The SG has also made very little investment on micro-mobility, last-mile and shared transport options that could also contribute positively to decarbonisation. The latest National Transport Strategy commits to local pilots and to co-develop the legal framework with the UKG.

Transforming towns and cities – from active travel infrastructure to 20-minute neighbourhoods – will play an important part in reducing transport emissions. Concepts such as 20-minute neighbourhoods, where the majority of day-to-day services can be found within a 20-minute walk, cycle or public transport journey of home, have gained some traction in Scotland but there is no public investment to back such proposals. For example, the latest National Planning Framework urges local development plans to incorporate 20-minute neighbourhoods but there is no meaningful capital outlay to develop and implement these proposals, or to retrofit existing car-dependent areas or areas typified by urban sprawl. Place-based intervention funding, such as community-led regeneration and reviving town centres, that could be used for such purposes has an inadequate budget of £50m a year.

Such city level transformations can be instrumental in reducing reliance on private transport while inducing wider co-benefits for public health, air quality, and access to social and economic opportunity. Similarly, while there has been investment in active travel infrastructure, the current scale of public investment in place-based transformation is incommensurable with the change required. The active travel budget is expected to rise to £320m in 2024/25, however, based on a commitment in the Programme for Government.

On aviation and shipping decarbonisation, progress has been slow with little emphasis on demand reduction, i.e. reducing passenger demand for flying. Significant investments are being made in the country’s ferry services but clean shipping infrastructure targets are weak with no clear delivery strategy in place. The UKG has however committed £685m of R&D funding to support the development of low-emission aircraft technology via the Aerospace Technology Institute Programme over the next three years. In aviation specifically, ambitious targets such as creating the world’s first zero aviation emission region have been set by the SG, in partnership with the Highlands and Islands Airport Limited (HIAL). However, they remain necessarily in the demonstration and pilot phase, funded by UK Research and Innovation (UKRI). The Government is yet to publish its aviation strategy following a consultation last year. As a potential future hub for hydrogen generation through excess renewables, shipping is a positive use case for these emerging technologies which Scotland could exploit.

Public investment in buildings

The majority of buildings’ operational emissions result from the use of fossil fuels for heating and hot water,[132] and they have fallen only slightly over the past decade. In 2021, emissions from buildings were 9.0 MtCO2e (21.6% of Scotland’s territorial emissions), compared to 10 MtCO2e in 2009 (or 16.2% of Scotland’s territorial emissions in 2009).[133] [134]

In relation to buildings and heat decarbonisation, the SG has made noticeable investments in tackling fuel poverty, in social housing & public sector decarbonisation, and in investing in heat networks. The investment for fuel poverty is £465m for a period of 5 years, an additional £200m for social housing and £200m for public sector decarbonisation to 2026. The SG recently committed to funding of £1.2m to enhance services for people seeking advice on energy bill management and energy efficiency through agencies like Citizens Advice, Advice Direct Scotland and Home Energy Scotland.

Warmer Homes Scotland, the Government’s flagship grant funded energy efficiency programme so far has benefited over 32,000 households. However, energy efficiency measures for the non-fuel poor housing stock are significantly behind with a lack of regulation or investment. Although loans and grants from Home Energy Scotland are available to homeowners to help to fund energy efficiency improvements,[135] the proportion of owner-occupied homes in EPC Band C or above is higher than for social or private-rented housing.[136] Emphasis is also lacking in the private rented sector where minimum standard led regulations remain the main driver of energy efficiency related private investment, despite the availability of loans to landlords for energy efficiency measures via Home Energy Scotland.

Specific targets for heat networks and for energy efficiency of multi tenure domestic and non-domestic buildings have been established but there is yet to be a coherent delivery strategy, particularly on low carbon heating, to reduce the building sector’s emissions by 70% by 2030 upon 2020 levels. The SG has allocated £300m over five years as part of its Heat Network Fund to support the development and roll out of heat networks. The speed of delivery across all policy measures needs to increase, as Scotland has more ambitious targets than England.

Overall, the SG has committed £1.8 billion of public funding for low carbon heating and energy efficiency projects to 2026, just over half of what the CCC laid out in its investment pathway. With the deepening of the cost of living crisis and the subsequent rise in levels of fuel poverty, further funding might be necessary to ensure adequate levels of support.

Public investment in energy

Emissions from electricity supply in Scotland have fallen dramatically in the past decade as renewable electricity generation increased nearly threefold between 2009 and 2019.[137] In 2021, emissions from electricity supply were 1.6 MtCO2e (3.8% of Scotland’s territorial emissions), compared to 13.4 MtCO2e in 2009 (or 22% of Scotland’s territorial emissions in 2009).[138] [139] The emissions reduction pathway in Scotland’s updated Climate Change Plan aims to achieve zero emissions from electricity supply in 2029. At the same time, Scotland’s electricity supply will need to accommodate increased demand, particularly from heating (heat pumps), transport, and electrification in industry. Earlier this year, The SG published a Draft Energy Strategy and Just Transition Plan[140] with more details on specific goals including the ambitions to deliver additional 12 GW of installed onshore wind capacity and to achieve 8 to 11 GW of offshore wind capacity by 2030.[141] Specific targets are currently missing for renewable energy storage.

A majority of the capital investment in this sector to-date has come from the private sector backed by the Contracts for Difference mechanism that guarantees developers long term revenues through competitive auctions. The high profitability of renewable energy compared to fossil fuels highlights future opportunities for further expansion on renewable energy generation in Scotland.

The SG set up the Energy Transition Fund capitalised with £75m to support businesses primarily in the fossil fuel sector to diversify their business model and help them transition to net zero.

Offshore wind is clearly a huge growth sector for the country but the Government acknowledged recently that the wider economic and social benefits have not been captured sufficiently.[142] The local content of Scotland’s offshore wind sector (i.e. inputs coming via local supply chains based in Scotland) is currently at 44%, less than the rest of the UK; and less than 1% of non-Scottish wind projects are delivered through Scottish supply chains. This represents a missed opportunity and the need for better policy design and greater collaboration between industry and government. The Government has an ambition to secure investments of at least £1bn in the Scottish supply chain for each GW of new offshore wind capacity and there is an ongoing consultation by the UKG to achieving the wider socioeconomic outcomes through changes in the Contracts for Difference scheme.

The growth of renewables has so far not met its full social value potential in terms of local supply chain and job creation, and has not translated into cheaper electricity. This presents a strong case for the SG to take an active role in shaping how Scotland delivers the next generation of renewable energy and who will benefit from it. To this effect, recent offshore wind projects leasing through ScotWind have set out substantial supply chain commitments and the Draft Energy Strategy and the Just Transition Plan reflects the potential for increasing local content of energy projects, boosting domestic supply chains and increasing community ownership. However, it only includes a general commitment to continue engaging with the UKG on these issues.[143]

Bold targets for onshore & offshore wind and hydrogen are in place but no such targets exist for renewable energy storage, however there is a strong expectation of private capital to leverage the huge storage opportunity in Scotland.

Public investment in industrial transformation

In 2021, emissions from industry were 9.6 MtCO2e (23% of Scotland’s territorial emissions), compared to 12.4 MtCO2e in 2009 (or 23% of Scotland’s territorial emissions in 2009).[144] [145] Following the Climate Change Commission reporting on Scottish emissions and methodology, emissions covered under industry include emissions from the construction industry, manufacturing, and fuel supply. Some of the key subsectors include cement, iron and steel, chemicals, and the extraction and refining of oil and gas.[146]

The emission reduction pathway in Scotland’s updated Climate Change Plan sets out to reduce annual emissions from industry to 7.3 MtCO2e by 2030, a 24% reduction on the sector’s emissions in 2021. This target reflects relative difficulty in reducing emission from industry, with the majority of emission reduction expected to happen between 2030 and 2040.[147] The plan’s vision for Scottish industry is heavily reliant on new technologies including carbon capture and storage, and the use of hydrogen in industry. The plan does not include specific goals around key factors underpinning Scotland’s transition to a net zero industry, such as improved resource efficiency, embodied emissions in materials, energy efficiency, industrial fuel switching, or specific industrial processes.

Many relevant policy levers are currently significantly dependent on the UKG, limiting the scope for intervention. The cluster approach to industrial decarbonisation (i.e. sites with multiple high carbon point sources, which represent over half of UK’s industrial carbon emissions) is appropriate but requires better coordination with Westminster and more urgent finance.[148] For instance, key decisions around financing the running costs of new industrial infrastructure such as hydrogen or carbon capture, utilisation and storage (CCUS), which are critical to industrial decarbonisation, fall largely within the powers of the UKG. The SG also cannot unilaterally decide to levy a charge on Scottish consumer energy bills to pay for long term operational costs of hydrogen infrastructure (an issue that is currently being debated as part of the Energy Bill going through UK Parliament).