Snowsports sector 2022 - economic, social, and cultural impact: research

This report presents the findings of research into the economic, cultural and social value of the Scottish snowsports sector.

3. Overview of the Scottish snowsports sector

Key findings

The sector is made of a diverse range of stakeholders with different structures and priorities. This can lead to challenges around establishing a clear and shared vision for the future. All mountain centres are account managed by an enterprise agency and benefit from capital investment.

Income levels vary between mountain centres. Several factors are at play, including differences in: visitor numbers; snow levels; days when skiing is available; and the level of dependency on snowsports activities.

Cost pressures, such as fuel costs, staff costs, repair and maintenance, coupled with poor snow conditions and the cost of living crisis, are creating very challenging financial conditions for the mountain centres. Artificial slope operators were reasonably optimistic about the future, but also acknowledged cost pressures.

Mountain centres are seeking to diversify and create demand for alternative activities throughout the year that will ultimately reduce their level of dependency on snowsports activities. Those centres that have successfully diversified and are less dependent on snowsports have been able to maintain levels of income.

Recruiting and retaining employees is challenging. There are also a range of investment needs across the snowsports sector (such as infrastructure, ancillary facilities, and services).

3.1 Introduction

This chapter provides an overview of the Scottish snowsports sector, detailing the governance, finance, and investment, and staffing, and the ongoing challenges associated with each.

It should be noted that the findings within this chapter were heavily dependent on availability and quality of data provided by the mountain centres and artificial slope operators. While some data was provided by the five mountain centres, limited data was forthcoming from the artificial slope operators. This limited the analysis, particularly in areas such as finance, demand, staffing and investment.

3.2 Governance

A range of governance structures are in place across the snowsports sector in Scotland. Although collaboration across the sector continues to improve, there are still elements of the sector working in isolation. As such, the range of stakeholders with varying degrees of commitment to, and focus on, snowsports is creating a fragmented landscape which could benefit from greater co-ordination.

Mountain centres

Glencoe, The Lecht, Glenshee, and the Nevis Range are all privately owned, limited companies. Cairngorm is a wholly owned subsidiary company of HIE.

In most (but not all) cases, assets (including buildings and uplift infrastructure) are owned by the operating company. The land that the centres occupy is leased from several different estates on a long-term basis which provides security of tenure to plan and invest for the long-term.

In the case of Glenshee, the lease period is nearing its final years and will need to be extended or renegotiated. Although not assumed to be problematic, lease renegotiations can be a challenging process and can lead to increased costs and more onerous conditions which could create an environment where future snowsports operations could be compromised.

Artificial slopes

The governance structures of the artificial slopes are varied:

- Six are owned by local authorities, five of which are operated by the local authority and one by a charitable trust.

- Two are owned and operated by private limited companies.

- Two are owned and operated by snowsports clubs.

- One is owned and operated by a small independent charity.

- One is owned by sportscotland and operated by its trust company which is also a registered charity.

- One is owned and operated by the Ministry of Defence.

- One is owned by a private company and operated by a separate private company via a tenancy agreement.

At the time of the research, the tenancy agreement in place at Snow Factor (Glasgow) was under review with the landlord indicating that the lease may not be renewed. This could result in the only indoor artificial snow centre ceasing operations. Snow Factor went into administration in November 2021, and appointed a voluntary liquidator on 7 November 2022.

Enterprise agencies

Both HIE and SE are engaged with, and have a significant interest in, the snowsports sector in Scotland through the five mountain centres. Of the five mountain centres, four lie in the geographic area covered by Highlands and Islands Enterprise (HIE) and one centre lies in the area covered by Scottish Enterprise (Glenshee).

Enterprise agency involvement is mainly through a dedicated account management approach for ambitious companies with which there is a strategic relationship. These strategic relationships have been crucial and will continue to be going forward.

The account management service provides access to a range of support, including:

- Developing business strategies.

- Advice and support to help build strong and effective leadership and management practices.

- Tailored support packages.

- Connecting companies with, and maximising available funding from, business support partners.

- Introducing companies to like-minded businesses and industry networks relevant to companies' future ambitions.

- Introducing companies to specialist advisors who can help businesses plan and implement changes.

Cairngorm Mountain (Scotland) Ltd (CMSL), which operates the Cairngorm centre is a wholly owned subsidiary of HIE and receives funding from HIE through submission and agreement of an annual business plan. CMSL also receive capital funding from HIE through the submission and agreement of formal business cases.

The Lecht, Nevis Range and Glencoe also operate within the geographic area covered by HIE but do not receive revenue funding from the enterprise agency. They do, however, benefit from capital investment from HIE periodically in support of a range of capital projects.

Glenshee operates within the geographic area covered by SE but do not receive revenue support from the enterprise agency. They also benefit from capital investment from SE periodically for capital projects.

Snowsport Scotland

Snowsport Scotland is a company limited by guarantee and supported by sportscotland to act as the Scottish Governing Body (SGB) for snowsports in Scotland. It is a membership-based body with around 10,500 members. Members include 33 clubs, organisational members (such as snowsports centres and Disability Sport UK), and individual members.

Snowsport Scotland plays a pivotal role in working with and collaborating closely with operators on a range of initiatives designed to develop and enhance sporting pathways, promote and increase snowsports participation, improve facilities and events, and build capacity in the sector. During the COVID-19 crisis, the governing body played a central role in securing valuable financial support for the sector to ensure its survival.

Other sporting governing bodies that have an interest in the snowsports sector include Scottish Disability Sport, Disability Snowsport UK, Mountaineering Scotland, and Scottish Cycling.

Other agencies

Other agencies and organisations that play a role in the snowsports sector include:

- Environmental agencies, which are concerned with how land and the environment is used, maintained, and developed around mountain centres.

- Tourism agencies, which focus on Scotland as a domestic and international tourism destination and the range and quality of the tourism offer.

- Local organisations, such as chambers of commerce and local authorities. These engage closely with centres to develop local participation, improve the quality and range of the offer, attract investment, and improve promotion and marketing.

3.3 Finance

The financial analysis of the sector was limited by the lack of data available from the mountain centres and artificial slopes. Of the five mountain centres, three were able to provide complete financial information. Of the 14 artificial slopes, only one was able to provide a complete and reliable financial data set. For confidentiality reasons, these centres are not named in the analysis.

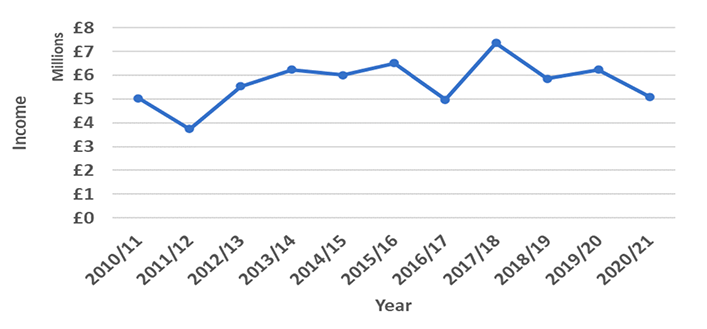

Income

Income levels vary between mountain centres. Some of this variation is most likely due to differences in visitor numbers, levels of snow, and days when skiing was available. Different income levels may also be due to the varying dependency on snowsports and non-snowsports activities for generating income.

Figure 3-1 shows that income for three of the five mountain centres has been maintained over the last ten years with a slight upwards trend. A dip in income was experienced in 2016/17 when levels of snowfall were very low. As anticipated, levels of income dipped substantially during the COVID-19 pandemic years (2019/20 and 2020/21), when most businesses had to shut down fully for a prolonged period.

Source: Data provided by mountain centres.

The mountain centres that have successfully diversified and are less dependent on snowsports have been able to maintain levels of income. It should be noted that the extent to which each mountain centre can successfully diversify and attract more visitors from outside the domestic market will vary. Factors include: location, existing provision, visitor numbers, levels of available investment, and land and suitability for development.

No analysis has been carried out on levels of income for the artificial slopes due to the absence of any reliable data.

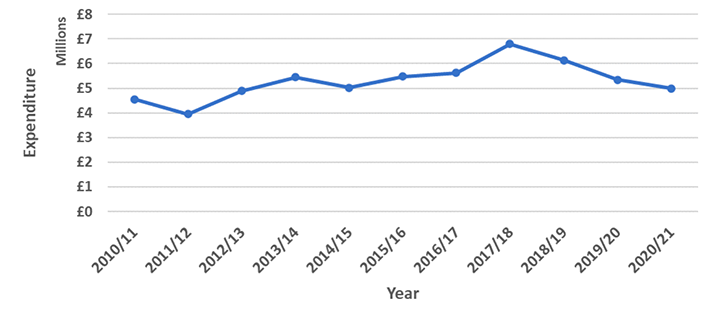

Expenditure

Figure 3-2 shows that for three of the five mountain centres, expenditure levels increased between 2010/11 and 2017/18, from £4.6 million to £6.8 million. However, since 2017/18, costs have been decreasing steadily.

Source: Data provided by mountain centres.

Some of the decrease in costs are aligned to years with reduced snowfall and therefore reduced levels of business. The years 2019/20 and 2020/21 reflect the significant downturn in business, and therefore costs, due to the COVID-19 pandemic.

No analysis has been carried out on levels of expenditure for the artificial slopes due to an absence of reliable data.

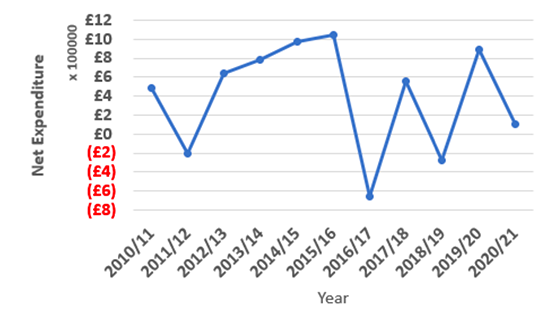

Net expenditure

Net expenditure is the difference between income and expenditure and determines the extent to which the mountain centres made a profit or loss. Figure 3-3 shows the years the net expenditure of the mountain centres between 2010/11 and 2020/21. It shows that in 2011/12, 2016/17 and 2018/19, the centres incurred an overall loss. These losses correspond to years with fewer snow days and lower visitor numbers.

Note: Negative net expenditure, i.e. a loss, is denoted in red and brackets on the y-axis.

Source: Data provided by mountain centres.

From stakeholder consultations, snowsports centres considered the current financial position as reasonably stable. In part, this reflects the positive impact of the Scottish Government COVID-19 funding. However, most stakeholders also acknowledged significant concerns for the future.

For the mountain centres, snow levels have affected their financial position. 2019/20 was one of the best snow years in recent times. Under normal circumstances, that year would have allowed the mountain centres to generate enough income to provide a cushion to sustain them through more challenging years. However, due to pandemic this did not happen.

Investments in snow-making, online ticketing, improvements to uplift and machinery, and diversification have all helped to financially strengthen a number of the centres. However, all centres are forecasting significant cost pressures in the future, primarily due to the increase in fuel costs, staff costs, repairs and maintenance, amongst others.

These pressures will be felt across the sector. Poor snow conditions and the cost of living crisis could create very challenging financial conditions ahead. Some centres felt that in five to ten years, it is unlikely that the current five centres will continue to deliver snowsports activities.

COVID-19 funding support provided by the Scottish Government has undoubtedly ensured the survival of many organisations through the pandemic. Without this, it is likely that some centres would have ceased trading. However, in some cases, this support was in the form of loans which could create longer-term pressures as companies must service these debts and manage other financial challenges.

For the artificial slopes, the financial climate has been less volatile as levels of demand for activities are much more consistent, predictable, and not dependent on snowfall. Most operators were reasonably optimistic about the future but again expressed concerns over current and future cost pressures.

In some cases, artificial slopes have been more successful in attracting levels of external funding particularly to support programmes and activities aimed at under-represented groups, including those who live in deprived communities.

3.4 Investment

The analysis of investment has again been limited by the lack of data made available both by the mountain centres and artificial slopes. Of the five mountain centres, three provided partial data. Of the 14 artificial slopes, four provided partial data.

The sector has benefited from at least £7.6 million in investment between 2016 and 2022.[3] This includes funding from a range of sources, including Highlands and Islands Enterprise (HIE), Scottish Enterprise (SE), LEADER, Local Authorities, Lottery Funding, Scottish Council for Voluntary Organisations (SCVO), and the European Regional Development Fund (ERDF).

Appendix A provides a summary of investment that has been made in some of the mountain centres and artificial slopes over the last few years.[4]

Key points to note:

- Among other activities, this funding has supported diversification, uplift infrastructure, and snow-making capability. Much of this investment has focussed on improving the customer experience and improve operational efficiency and environmental sustainability. For example, the Nevis Range now offers a year-round range of activities and has invested considerably in a new hotel and conference facilities to diversify their income.

- The level of investment in the artificial slopes over the last few years has understandably been less than the mountain centres and has focused on ski matting replacement and ski tow maintenance/replacement. When compared to the mountain centres, the artificial slopes appear to have been more successful in attracting investment from a wider range of sources, for example, LEADER, SCVO, Lottery and other sources.

HIE investment

Since 2014, HIE has made significant capital investment into the four mountain centres that sit in their region (excluding Glenshee which is account managed by SE). Funding is generally provided based on the submission of individual business cases with the intervention rate sometimes as much as 75% of total costs. HIE has indicated that this is now reducing to a maximum of 40%. Table 3-1 below shows the levels of approved investment by HIE in mountain centre projects. It should be noted that some projects did not spend their allocation in full, and so the amounts shown do not necessarily reflect actual expenditure.

| Year | Investment Approved |

|---|---|

| 2014 | £2.74m |

| 2015 | £0.21m |

| 2016 | £0.01m |

| 2017 | £0.09m |

| 2018 | £0.36m |

| 2019 | £1.44m |

| 2020 | £0.73m |

| 2021 | £3.31m |

Source: HIE.

Note: This is capital and not added to revenue expenditure so does not feature in net expenditure calculations.

Appendix A shows a more detailed breakdown of HIE and SE investment for each of the mountain centres. As shown in Table A-10, Cairngorm Mountain centre received the highest levels of funding from HIE between 2021-22.

Future investment priorities

Our consultations identified several priorities for future investment:

- Diversification of activities was identified as an important factor to enhance future sustainability. This includes undertaking feasibility studies of a broad range of opportunities and implementing those projects that are viable/most likely to be successful, and that can be operated all-year round.

- The development of staff accommodation to address the shortage of affordable housing in local communities was also considered important. Environmental sustainability, reducing carbon footprint and maximising operational efficiency were other areas mountain centres identified for future consideration and investment.

- Due to the age of much of the uplift equipment across the five mountain centres, there is a continuing need for investment in upgrading and replacing ageing infrastructure.

- There may be a need to invest in better snow-making facilities that can ensure a consistent seasonal offer at each of the mountain centres. However, the scale of investment would be significant as it would be required to be environmentally sustainable.

- All centres are engaged in projects to enhance the quality of the customer experience. Investment priorities include improving toilet facilities, catering, and car parking infrastructure.

- Priority investments for the artificial slopes were mainly focused on replacement of ski slope surfaces and tow infrastructure. However, in a few cases some facilities are looking to expand their activities and services. Hillend (near Edinburgh) has plans and funding in place to extend facilities to include zip wires and indoor climbing to create a destination venue where visitors can experience a range of activities alongside skiing. Alford Ski Centre plans to undertake refurbishment of the building and create a new community room, social area and potentially a gym/ fitness room.

In addition, the Scottish Ski Industry Strategic Review (May 2019) makes several comparisons with the snowsports industry in other countries, most notably New Zealand, which has seen strong growth in its snowsports sector in recent years with a similar number of snowsports centres and population to Scotland. The most notable difference was the high level of investment in marketing of the snowsports industry in New Zealand compared to Scotland, where there is "…a chronic low level of investment in marketing in respect of the Snowsports Sector".

3.5 Staffing

The mountain centres and artificial slopes provide a valuable source of full-time, part-time, and seasonal employment opportunities for people who live within local or neighbouring communities and for those who are visiting the area and are employed on a seasonal basis.

The centres are significant employers which between them employ around:

- 120 full-time staff,

- 35 part-time, and

- 200+ seasonal staff (this can vary significantly based on how good the snow conditions are and how long it lasts for).

This is the equivalent of 185 Full Time Equivalents (FTE)[5].

The limited data provided by the artificial slopes allows for only indicative employment figures to be estimated. This would suggest that the artificial slopes employ around:

- 80 full-time staff,

- 270 part-time staff, and

- 200+ sessional or casual employees.

This accounts for approximately 269 FTE.

Appendix A shows the range of employment opportunities within the sector.

The snowsports sector is experiencing significant staffing challenges, some of which are fundamental to the longer-term sustainability of the snowsports sector. The themes covered below were raised through our stakeholder consultations.

Recruitment and retention of staff

Like many other sectors of the economy, the snowsports sector is experiencing significant challenges with the recruitment and retention of staff. These issues have been further amplified by the pandemic with many staff, particularly those on casual and zero hours contracts choosing to leave the sector and seek more stable employment opportunities. This was identified as a particular issue with ski instructors although most organisations that were consulted expressed significant concerns about the recruitment and retention of staff across the full range of employment positions.

Year-round employment

Increasing unpredictability in terms of weather and the impact of the EU Exit, removing the freedom for individuals from the UK to work across Europe, is making the sector increasingly unattractive to many who are entering the employment market or seeking more stable employment. These changes are also weakening career paths within the snowsports sector which again makes the sector less attractive.

Businesses within the sector that have successfully diversified, or which are larger in scale, have been able to offer more secure, year-round employment opportunities. However, several centres are experiencing challenges in recruiting and retaining staff where they are not able to offer year-round employment.

Qualification structure and costs

Several stakeholders expressed concerns about the structure/suitability of coaching qualifications within the sector, the availability of training opportunities and the relative high cost of obtaining qualifications.

For some of the artificial slope operators that deliver basic learn to ski activities, it was felt that the current qualifications required to coach were too onerous and expensive, which makes it more difficult to recruit qualified coaches/instructors. There was also considered to be insufficient training courses available for individuals to become qualified.

A lack of coaches/instructors that are qualified to deliver activities for disabled people is also having a detrimental effect on engaging groups that are under-represented in snowsports.

Succession planning

Much of the mountain centre provision is owned and operated by small privately owned companies. This means that they typically rely on a few highly motivated and hands-on individuals. Resources and time are therefore often at a premium within these centres, making future planning a challenge.

Such a reliance may make these businesses more vulnerable, for example, if key individuals were to become ill or were not able to fulfil their roles for a period, etc. Thought needs to be given to how these businesses are supported to build resilience and capacity to ensure continuity in the longer-term.

Cost of living

The current cost of living crisis is likely to have a significant impact on the sector which is already characterised as a low paid sector of the economy (for example, many jobs are at minimum wage or marginally above it). The cost of fuel for those travelling significant distances to and from work, particularly for those working at more remote centres, may also force some people to seek alternative local employment. Access to affordable housing in many areas is also an issue which will affect some mountain centres' ability to recruit and retain staff.

In addition, the cost of living crisis, in addition to events such as the COVID-19 pandemic, have placed increased pressure on Scottish public finances. It remains a challenging financial environment, and it will likely be difficult for the snowsports sector to secure the levels of public funding required to address all future investment priorities.

3.6 Sustainability and net zero

Scottish Government is committed to taking action to reach net zero emissions by 2045. Global temperatures continue to rise and weather patterns are less predictable. The 2021 International Report on Snow & Mountain Tourism reports that over the last 50 years there has been no significant shift in winter temperatures at summit location in the Alps. While there has been some warming, this has been limited to the spring and summer seasons, with autumn and winter only seeing mild increases.

However, a number of studies highlight the risks of climate change to the ski market in the future, which has potential to: reduce snow reliability (Vulnerability of ski tourism towards internal climate variability and climate change in the Swiss Alps); destabilise the winter tourism system (The impact of climate change on ski season length and snowmaking requirements in Tyrol, Austria); and reduce the length of the skiing season (Effects of Climate Change on Alpine Skiing in Sweden).

In a Scottish context, a recent forecast by The James Hutton Institute and Scotland's Rural College (SRUC) (2020) into the impacts of global warming for Cairngorm Mountain found that there is "likely to be a decline in snow cover days per year from the 2030s [including at Aviemore which] will continue through to the 2080s". By 2080, there is a "likelihood of some years with very little or no snow" (Climate Xchange, 2019).

Other key findings from the same report, which are in line with results from the UK Meteorological Office and Inter-governmental Panel on Climate Change, include:

- "Large variation between years" with less frequent years that are comparable with past amounts of snow cover.

- Temperatures are projected to continue increasing, with a higher probability of having more days when the temperature is above a threshold of 2°C for snow formation.

- There is an increasing probability of more heat energy input on ground surfaces with an increasing snow melting affect.

The report concluded that "warming will continue meaning snow cover and depth is likely to decrease on Cairngorm Mountain from the 2030s". This raises serious challenges for snowsports both in Scotland and beyond as these findings are reflective of global challenges.

There is a degree of uncertainty with these forecasts as ongoing efforts to mitigate climate change may reduce the severity of impacts. The report also emphasised that these predictions are subject to a large amount of uncertainty, with snow being particularly complex to model. However, "even higher emissions rates (for example, due to ecosystem carbon releases) may further increase impacts" (The James Hutton Institute and SRUC, 2020; Climate Xchange, 2019).

Consequently, the timing and volume of snow in Scotland throughout the winter season is reducing and is now much less predictable than it used to be. This is a clear threat to the viability of mountain centres (as in, there is a greater risk of less snow in future years as temperatures rise).

Greater investment in snow-making machines could help to mitigate the impacts of climate change on both Scottish and international snowsports businesses. The use of snow-making machines to mitigate the impact of shorter and more inconsistent seasons has been used in Austria, for example, which invested €1 billion in snowmaking over the past decade. The US government has also provided grants to purchase snow-making equipment to a variety of snowsports centres.

The Scottish Ski Industry Strategic Review report therefore argues that an uplift in investment in marketing and snow-making equipment is necessary to boost the Scottish snowsports industry. Snowsport Scotland's National Facilities Strategy (2020) also suggests all five mountain centres should invest in further snow-making facilities.

The negative impact of snow-making is well documented as it relies on a significant amount of water and energy. Some organisations have looked to 'greening' their snow production. For example, the Lecht relies on water supplies from its own sources and power supplied through its own wind turbines for producing its snow.

In addition, there are opportunities to explore newer, innovative snow-creating alternatives which use significantly less energy. Efforts are being made to make the sector more sustainable. For example, the Nevis Range has achieved Carbon Neutral Status and is attempting to achieve net zero. It is doing so by: installing a Hydro Plant which provides the majority of the mountain centres' energy; banning single use plastics from cafes; composting left over food; and installing Electric Car points in its carpark.

However, such efforts are inconsistent across the sector. Some mountain centres may be better placed than others to explore and adopt such opportunities. Feedback from the consultations undertaken as part of this research confirms that information on best practice is shared between operators. There are also likely to be examples of where a more cautious approach is taken to information sharing (such as, where information or data is regarded as commercially sensitive).

3.7 Conclusions

The mountain centres and artificial slopes have benefited greatly over the years with investment from a range of sources, including from the Scottish Government and Enterprise Agencies. The strategic relationships with the Enterprise Agencies will continue to be key, and given the pressure on public sector finances, securing the significant funding required to address future investment priorities will remain challenging. This means that the Scottish snowsports sector must:

- Prioritise actions and identify which investment priorities are the most important and which have the biggest impact.

- Continue to explore ways to diversify, become less reliant on public support, and aim to become self-sustaining.

The mountain centres also face wider significant challenges, including:

- unreliable snowfall,

- the level of dependency on snowsports,

- cost pressures,

- staffing pressures, and

- the ongoing cost-of living crisis.

Climate predictions pose challenges for the Scottish snowsports industry, with lower overall amounts, and greater infrequency of snow likely over the coming decades. Greater investment in snow-making machines could help to mitigate these impacts to a certain extent.

The mountain centres continue to explore options to diversify and create demand for alternative activities throughout the year to reduce, in some cases, a high level of dependency on snowsports activities. Those centres that have successfully diversified and are less dependent on snowsports have been able to maintain levels of income and attract people from further afield.

However, the five mountain centres are at different stages in terms of diversification, and the extent to which they can successfully diversify and attract more visitors from outwith the domestic market will vary due to a range of factors. This includes: location, existing provision, visitor numbers, levels of available investment, and land and suitability for development.

Contact

Email: socialresearch@gov.scot