Delivery Assurance Group (DAG) report: quarter 3 2021-2022

Report summarising what has been achieved for customers against Scottish Water's Delivery Plan for the 2021 to 2027 period during the third quarter of 2021 to 2022

Delivery Assurance Group: Progress Report: Quarter 3 2021-2022

This document sets out how Scottish Water is progressing with the delivery of projects and sub-programmes included on the 'Committed List' and confirms the position up to the end of December 2021 (Quarter 3 2021-22). It has been prepared for the Delivery Assurance Group (DAG), a group set up by Ministers to provide assurance and report on the delivery of their Objectives.

What We Monitor

Each quarter Scottish Water reports to the DAG on its progress with the delivery of projects and programmes included in the Committed List through four lenses as follows:

Section 1: Indicator of Progress of Overall Delivery (IPOD): to provide reassurance to stakeholders on the extent to which overall progress of projects on the Committed List are in line with the forecasts set out when the projects were committed to delivery.

Section 2: Management Approaches (MAs) progress overview: to provide stakeholders with a view on the progress of delivery at Management Approach level and to highlight any areas where the progress of delivery is of concern within the overall programme.

Section 3: Large projects progress (or projects that are novel, strategic or contentious): to provide stakeholders with a view of the extent to which larger projects or projects that are novel, strategic or contentious are progressing through milestones in line with the forecasts set out when these projects were added to the Committed List.

Section 4: Summary of key projects of interest: containing a summary of the output of bilateral Scottish Water/Stakeholders sessions (e.g. Joint Development Groups) highlighting by exception those key projects of interest that may not be progressing in line with the forecasts set out when these were added to the Committed List.

The summary below also provides stakeholders with quarterly investment levels in Tier 2 and with an update of impacts of external factors on the delivery of projects on the Committed List.

Annually, to support smoothing out inevitable variations occurring at individual project level, the cost for projects or sub-programmes on the Committed List that have completed during the year are reported, comparing this to the forecast costs of these projects and sub-programmes when they were added to Committed List.

The content and format of this report is under review by the Investment Reporting Task and Finish Group and Investment Reporting Data Subgroup which in turn report to DAGWG. The amendments listed below have been made following stakeholder feedback from previous DAGWG and DAG meetings and further developments are being explored:

- The Summary section includes an update on delivery and commercial risks that may impact on the delivery of committed projects and programmes.

- All references to gate numbers have been changed to reflect the activities taking place at each gateway with the relevant gate number in brackets for reference, i.e. G100 has been changed to "Acceptance (G100)" and G110 has been changed to "Financial Completion (G110)".

- Explanatory text has been added in section 1 to better explain being above or below the baseline.

- The definition of "on track" or "not on track" has been changed to within or outwith the target range to add a level of transparency to the report and avoid confusion. The lower and upper limits of the range (previously referred to as "tramlines") remain unchanged (i.e. the upper limit is the forecast baseline from the next quarter and the lower limit is the baseline from the previous quarter).

- Appendix A (Summary of milestone attainment position) has been updated as follows:

- An additional column has been added to the original table showing the progress status in the previous quarter to provide a clearer high-level overview of progress through quarters.

- An additional table has been provided to show the forecast position at year-end and changes in status from the previous quarter.

- The column headings have been amended to maintain consistency of language.

Summary

Historically, at the start of a new investment period, Scottish Water has seen a dip in investment levels as new processes and delivery partners are bedded in. In year 1 of SR21 Scottish Water has not only maintained investment in line with that achieved at the end of SR15 but has increased it to meet the challenging targets set out in the Delivery Plan and outlined below.

Scottish Water's 2021 Delivery Plan sets out its intention to invest between £570m and £650m on projects delivering asset replacement, planned repair and refurbishment, enhancement, flooding, and growth (classed as "Tier 2" investment) in 2021-22. The Interim Prospects and Performance report revised and narrowed this range to £600m to £650m.

At the end of Quarter 3 2021-22, Scottish Water has invested £473m on projects and sub-programmes delivering asset replacement, planned repair and refurbishment, enhancement, flooding, and growth, against a forecast of £462m. This investment includes £199m of enhancement, £26m of Growth and £250m in asset replacement, planned repair and refurbishment. It also includes £75m invested on the delivery of projects that were planned to be completed in the previous period but have been delayed due to the impacts of COVID-19 and/or the realisation of other risks. Scottish Water is forecasting at the year-end to be within the revised investment range.

The total forecast year end investment is £790m-£820m including expenditure on responsive repairs and refurbishment of its assets and reasonable cost contributions.

Delivery and Commercial Risks

We continue to monitor risks that may impact delivering to forecast. These risks fall into three broad categories:

- Third Party risk: Potential delays due to unforeseen third-party issues

- Construction risk: Unforeseen delays from allowable events or poor performance on site

- Wider market risks

Key risks that are we are managing at present are:

Construction market conditions: Market conditions are driving cost pressures and availability of materials, labour and commodities continue to present challenges across the capital programme. Projections on market conditions vary with some indicating the market will be more stable in 2022, and others predicting longer periods of construction inflation circa 5%. We will not fully understand the cost or time impact at programme level until contractual notices and fully substantiated cost and time impacts reach us. In reaction to this we are agreeing adjustments to target price agreements where our delivery partners cannot commit to projects due to market pressures. These are being made based on market evidence with the provision for contract rates and prices to be applied when market pressures reduce.

COVID-19: Following the country's move to beyond Level 0, revised safe working procedures were implemented at the end of September in line with Government guidance and Construction Scotland's guidance. This guidance was reviewed in December in response to the new Omicron variant and no change to the working procedures was implemented as the safe systems of work in place were considered appropriate. The guidance and associated procedures are being well complied with, and local COVID-19 outbreaks are well managed. Our delivery partners have indicated that there continues to be a cost premium to this, and we are currently assessing this with them.

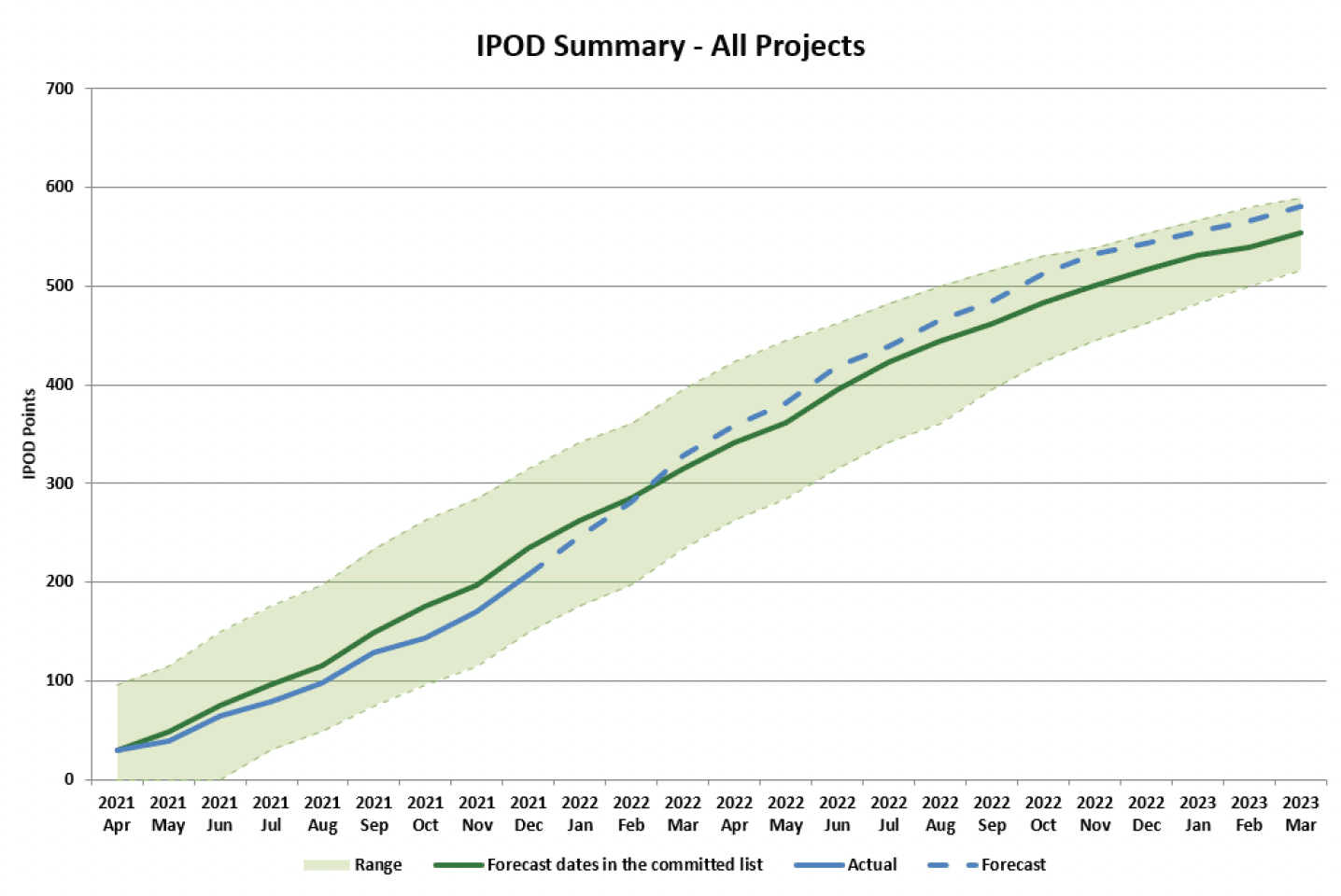

1. Indicator of Progress of Overall Delivery (IPOD)

The Indicator of Progress of Overall Delivery provides a high-level measurement of Scottish Water's progress in delivering the Committed List for projects over £1m[1]. It assesses the progress of these investment projects monitored by DAG across three delivery milestones combining this information to give an overall score. Details on the progress of the delivery of individual large projects (or projects that are novel, strategic or contentious) within the overall programme is provided in section three of this report.

When named projects[2] are added to the Committed List, each milestone is allocated a point. Each quarter, the number of points achieved by reaching milestones is assessed against the baseline[3] level for the previous quarter (lower limit) and the subsequent quarter (upper limit). These points are shown as absolute scores. Scottish Water is considered to be within the target range where the amount of points gained lies within the lower and upper limits.

The IPOD position at quarter 3 2021-22 was 207 points, within the target range of 149 to 315 points. The forecast for the year end is to continue to be within the target range and recovering towards the baseline.

Appendix A provides a summary analysis of the milestones within and outside the target range at Quarter 3 2021-22, along with the forecast year end position.

Both the 'Start on Site' (G95) and the 'Financial Completion Milestones' (G100) are currently within the target range and are forecast to remain within the range at year end. The Acceptance (G100) milestone is slightly below the target range but forecast to recover by year end. Although we have experienced some 3rd party delays and delays due to COVID-19 restrictions, the majority are a result of construction risks being realised.

2. Management Approaches progress overview

This section provides an overview of which projects, grouped by Management Approach (MA), are ahead, within or at risk of being behind the year target range forecasts. An explanation of progress, risk and how Scottish Water intends to manage the risks is also provided where relevant.

Progress is assessed by comparing the number of IPOD points forecast to be achieved at the year-end by projects in each Management Approach against the baseline level for the previous and the subsequent quarter (the lower and upper limits).

Four MAs are currently forecasting to be ahead at the year and three behind with the rest within the target range. There are no significant delays to report.

SR15 Completion

At the end of the SR15 period there were 143 enhancement projects still to achieve Regulatory Sign Off (RSO)[4]. 57 of these were planned for delivery in the SR21 period but 86 projects, originally planned for delivery before March 2021, have been delayed due to the impacts of COVID-19 and the realisation of other risks.

Of these 86 delayed projects; 8 remain in development and have yet to start on site, 40 have now achieved Acceptance (G100) and are providing benefit to customers, the remaining projects are in construction with the last project (Rockcliffe Bathing Waters) forecasting Acceptance (G100) in Q1 25-26. This project involves the construction of a new Wastewater Treatment Works. The site selection for the works has been subject to considerable community engagement. The progress of the 86 delayed projects is shown in the table contained in Appendix B.

The SR15 Completion projects remain under close scrutiny and progress is being made with all of the projects.

3. Large projects progress, or projects that are novel, strategic or contentious grouped by portfolio

This section provides an overview of the progress Scottish Water is making in delivery of projects above £3m, or those that are novel, strategic or contentious. The projects are grouped by portfolio. Progress is measured against the baseline of the Committed List for the previous and subsequent quarter. Where delivery of the projects within the portfolio is outwith these tramlines, or is at risk of being so, narrative is provided explaining the reasons and how the risk is being managed and what Scottish Water is doing to recover.

Although the IPOD position for the delivery of the whole Committed List is positive, for the large value projects reviewed in this section of the report not all milestones are within the target range. The acceptance (G100) milestone for all three portfolios is currently outwith the target range but forecasting recovery to the bottom of the range by year end. This is balanced by stronger performance in the Start on Site (G95) and Financial Completion (G110) across the three Portfolios.

A significant project that achieved acceptance (G100) in Quarter 3 and hence is providing benefits to customers is "Katrine Aqueducts". This project sits within the water portfolio and involves significant repair and maintenance work to the aqueduct which transfers raw water from Loch Katrine to the treatment works at Milngavie. A significant project that reached financial completion (G110) in Quarter 3 is "Aviemore WWTW Growth". This project sits within the Wastewater portfolio and involves the enhancement of the existing works to provide increased capacity of c3800 PE (Population Equivalent) to enable planned development.

4. Summary of key projects of interest

During discussions held as part of the regular bilateral meetings, DWQR requested that the progress of Loch Ness Regional WTW and Invercannie WTW be highlighted to the DAG as delays in delivering these are likely to impact another project, require further operational mitigation and potentially increase water quality risk. A description of and update on the progress with these projects is provided in the table below.

| Loch Ness Regional WTW | Loch Ness Regional WTW involves the construction of a new nanofiltration membrane WTW and water supply network to replace Invermoriston WTW and Fort Augustus WTW. We believe that during commissioning trials of the WTW, fine grit has damaged the membranes. The source of the grit and mechanism causing the damage is under detailed investigation and additional source, and pre-membrane treatment options are being assessed. There are few if any examples of this type of damage being sustained to these membranes at any other site. This has caused a considerable delay with Water into Supply now forecast in November 2022 and Acceptance (G100) now forecast as February 2023. These dates are dependent on satisfactory testing of the membranes following installation of an enhanced mechanical filtration stage. Options are being developed to enable water into supply by July to allow Invermoriston to be taken out of service before the peak holiday season. At this stage we are unclear if this is going to be possible. All interim risk controls remain in place at the existing two WTWs. |

|

|---|---|---|

| Project ID | 4031270000 | |

| Acceptance (G100) (Committed) | Jan 2022 | |

| Acceptance (G100) (Forecast) | Feb 2023 | |

| Invercannie WTW | Invercannie WTW is being upgraded to allow it to reliably supply 66Ml/d of water into the Aberdeen supply system which is also supplied by Mannofield WTW. The works include the installation of a DAF (Dissolved Air Flotation) pre-treatment stage for the existing membrane treatment plant and the provision of clear water tank storage. The main electrical contractor for the project went into administration part way through the project, and whilst a new sub-contract has now been let this has incurred delays of approximately 3 months with Acceptance (G100) for the overall project moving back to March 2023. Commissioning of the DAF process (forecast for Q3 22/23) is key to increasing the output from Invercannie, allowing throughput at Mannofield to be reduced and work to commence on high priority coagulation and filtration improvements to reduce water quality risks, in particular Cryptosporidium. |

|

| Project ID | 5012430000 | |

| Acceptance (G100) (Committed) | Jan 2023 | |

| Acceptance (G100) (Forecast) | Mar 2023 | |

Scottish Water will continue to monitor progress with these projects closely.

5. Conclusion

The DAG is invited to note that:

- Market conditions are driving pressures on project costs and the availability of materials, labour, and commodities. The overall impacts and their duration remain uncertain.

- By the end of Quarter 3 £473.4m has been invested on projects and sub-programmes delivering asset replacement, planned repair and refurbishment, enhancement, flooding, and growth against a forecast of £462m. Scottish Water forecasts to invest between £600m and £650m by year-end which is in the top half of the range as revised by the Prospect and Performance Report.

- Scottish Water's IPOD position at the end of Quarter 3 is 207 points which is within the target range. The forecast for the year end is to continue to be within the target range.

- At the Management Approach level, all are forecast to be within the target range at the year-end.

- Of the 86 SR15 delayed projects; 8 remain in development, 40 have achieved acceptance (G100) and are providing benefit to customers, and the remaining projects are in construction.

- Focusing on larger projects, all three portfolios were below the target range for the 'acceptance' (G100) milestone at the end of Quarter 3 and are forecasting to be at the bottom of the range at the end of the year.

- During discussions held as part of the regular bilateral meetings, two projects (Loch Ness Regional and Invercannie) were identified by stakeholders to highlight to the DAG.

Contact

Email: waterindustry@gov.scot