Council Tax for second and empty homes, and non-domestic rates thresholds: consultation

This joint public consultation with COSLA seeks views on giving local authorities the power to increase council tax on second homes and empty homes, as well as considering whether the current non-domestic rates thresholds for self-catering accommodation remain appropriate.

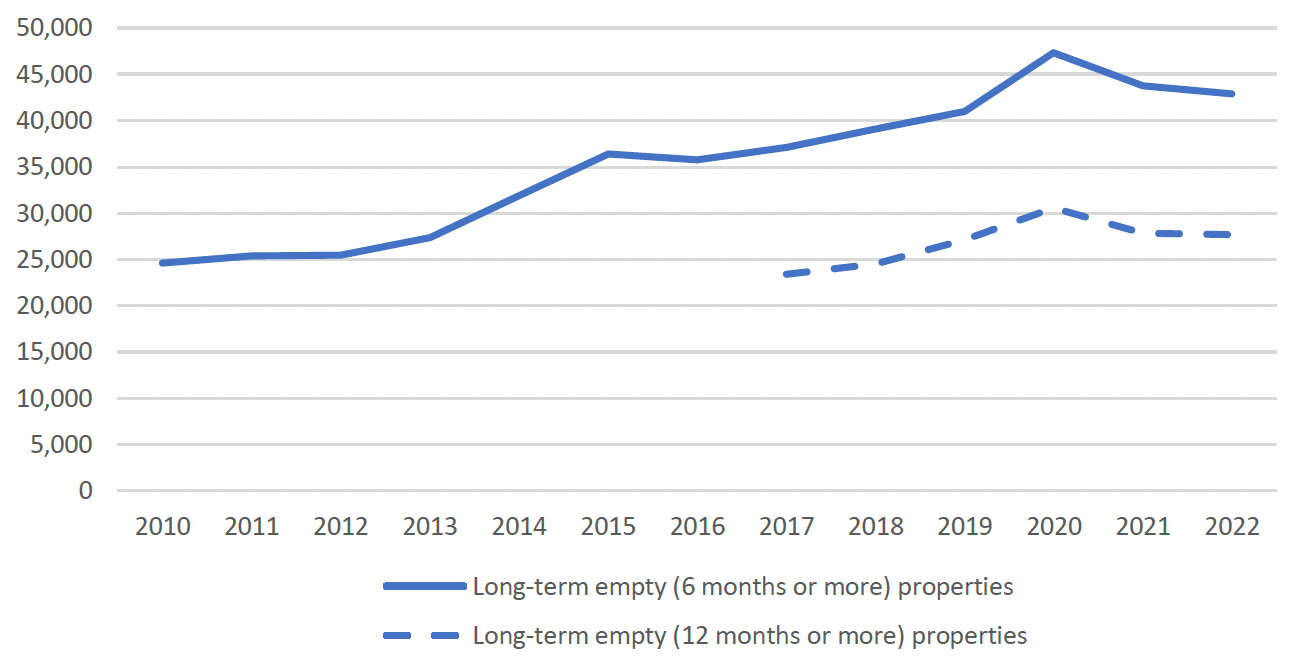

Long-term empty homes

The current position

As at September 2022 there were 42,900[8] long-term empty (6 months or more) homes (classified for council tax purposes), equating to around 2%[9] of all residential accommodation in Scotland.

Figure 2 shows the number of long-term empty homes has risen in the past decade. Some of the increase may be explained in part by the reclassification between second and empty homes in recent years. The number of councils employing Empty Homes Officers rose by almost a quarter between 2014 and 2022. This may have led to improvements in data quality and reporting resulting in further increases.

Long-Term Empty Homes – the legislative framework

An empty home is not someone's sole or main residence. It may be either furnished or unfurnished but is either not lived in at all or is lived in for less than 25 days in the council tax charging period.

The Council Tax (Variation for Unoccupied Dwellings) (Scotland) Regulations 2013 (as amended in 2016) ("the 2013 Regulations") set a 50% council tax discount as the default charge for empty homes and give councils the power to change that discount.

For empty homes this means councils can currently:

- alter the level of discount, to provide a discount of between 50% and 10% subject to certain restrictions (as set out in schedule 1 of the 2013 Regulations)

For homes that have been empty for 1 year or more councils can also:

- offer no discount

- charge a council tax increase for certain empty homes, subject to certain restrictions

Councils must ringfence some of the revenue generated from council tax on second and long-term empty homes for the purposes of affordable housing and are encouraged to do the same for revenue generated from any premium applied to long-term empty homes.

The current legislation provides a framework setting out what may be charged and when, allowing councils to take circumstances into account that could bring the home back into use.

| Status of empty home | Up to 6 months | 6-12 months | 12 months + | 2 years + |

|---|---|---|---|---|

| No work underway and not for sale or let | Owner may apply for an unoccupied and unfurnished exemption | Discount can be varied between 50 and 10% | Discount can be varied between 50 and 10% or discount can be removed or premium of up to 100% can be applied | Discount can be varied between 50 and 10% or discount can be removed or premium of up to 100% can be applied |

| If undergoing repair work to make them habitable | 50% discount cannot be changed | Owner may apply for a major repairs or structural alterations exemption. Discount can be varied between 50 and 10%. | Discount can be varied between 50 and 10% or discount can be removed or premium of up to 100% can be applied. | Discount can be varied between 50 and 10% or discount can be removed or premium of up to 100% can be applied. |

| If being actively marketed for sale or let | 50% discount cannot be changed | 50% discount cannot be changed | 50% discount cannot be changed | a premium of up to 100% can be charged |

In certain cases empty homes are exempt from council tax. These include, for example, properties where the owner is in long term residential care, in hospital or in prison. A full list of the other exemptions can be found within schedule 1 of The Council Tax (Exempt Dwellings) (Scotland) Order 1997 (legislation.gov.uk). This consultation is not proposing any changes to these.

The case for change

Even allowing for data improvements, reclassifications and the impact of the Covid-19 pandemic, there is still clearly an upward trend in the numbers of long-term empty homes.

The process to bring long-term empty homes back into use is typically complex, takes time and is often reliant on there being sufficient funds for refurbishment/ renovation. The Scottish Empty Homes Partnership Annual Report 2020-21 sets out the range of reasons homes become and remain empty.

Our Housing to 2040 Strategy commits us to take forward a number of actions on empty homes. One action is to continue to support the Scottish Empty Homes Partnership approach, which we have funded since 2010. In this time, the Partnership has worked with councils and empty home owners to help bring over 8,000 homes back into use. We are also currently undertaking another action to research the effectiveness of different ways to bring homes back into use and the findings will be used, alongside the responses from this consultation, to inform future policy decisions.

Around two thirds of empty homes are empty for longer than 12 months. This proportion has remained consistent since 2017. Taxation is one way that councils can tackle empty homes. Where used appropriately, charging a premium on long-term empty homes can be a useful tool as a disincentive for homes to be left unoccupied indefinitely. However, under the current arrangements this premium is limited to 100% (double the full rate of council tax).

Long-term empty homes proposal for consultation

Our commitment in Housing to 2040 is to provide councils with tools and powers to support them to make the best use of existing housing stock, including empty homes. This could mean providing councils with additional discretionary powers to charge more the longer homes are empty.

This consultation is seeking views on whether the current premium should remain capped at 100% or if councils should have discretion to increase this beyond 100%.

We are keen to hear views about whether, and if so how, the current discretionary powers are helping bring privately owned empty homes back into use.

As with second homes, we are interested to know what factors people think councils should consider when deciding whether to impose a premium, whether that be less than 100% or, if provision is to made for this, more than 100%.

A non-exhaustive list of potential factors might be:

- numbers, percentages and distribution of long-term empty homes throughout a local area

- potential impact on local economies and the community

- patterns of demand for, and availability of, affordable homes

- potential impact on local public services

- impact on neighbours and local residents

Councils may also decide not to use the powers or to disapply a premium for a specific period of time.

A non-exhaustive list of examples of where a council might do this include:

- where there are reasons why a home could not be sold or let

- where an offer has been accepted on a home but the sale has not yet been completed and the exception period has run out

- if the home has been empty for longer than 12 months but has been recently purchased by a new owner that is actively taking steps to bring the home back into use

- if an owner has submitted a timely planning application or is undergoing a planning appeal that is under consideration by the council or Scottish Government. This means they cannot undertake work to bring the home back into use until that process is concluded

- where charging a premium might cause hardship or act as a disincentive to bringing the home back into use e.g. where extensive repairs are actively being carried out

Contact

Email: secondemptyhomes@gov.scot