Scottish Income Tax: distributional analysis 2022-2023

A note on the distributional impact of the Scottish Government’s Income Tax policy for 2022-2023

Income Tax: Cumulative Impacts on Income Levels and Equality

Summary

This note sets out the distributional impact of the Scottish Government’s Income Tax policy choices on Scottish taxpayers since 2016-17, when the Scottish Parliament was first able to set a different rate of Income Tax in Scotland. The analysis shows that the Scottish Government’s decisions over this period, combined with changes in the UK-wide Personal Allowance, have been highly redistributive and have protected low income taxpayers.

The note considers the effect of Income Tax policy on taxpayers in 2022-23 compared to a counterfactual scenario where Income Tax policies announced at and since April 2016-17 were not introduced, and all thresholds and the Personal Allowance were uprated with CPI inflation instead. Compared to this scenario:

- 62% of taxpayers will pay less tax in 2022-23 than they would have done if the Income Tax policy had followed default inflationary uprating (‘the counterfactual’). On average, lower earners, women, older and younger taxpayers particularly benefit. In 2022-23, the taxpayers who are better off than they would be under inflationary uprating include:

- The lowest earning 60% of taxpayers. The lowest earning 20% will see the largest decrease in tax relative to their gross income (0.3%).

- 92% of taxpayers aged under 25 years and 83% of taxpayers aged over 75 years.

- 72% of female taxpayers, compared to 54% of male taxpayers. However, this is due to the fact that women’s earnings are, on average, lower.

- Taxpayers in the middle of the income distribution (deciles 3 to 5) will pay on average £56 less in tax in 2022-23 than they would have under the counterfactual. This is due to the introduction of the 19p Starter Rate in Scotland from 2018-19, as well as above-inflation increases in the UK-wide Personal Allowance over the period.

- The highest earning 10% of taxpayers will see the largest increase in tax, both in cash terms (£1,490) and relative to their gross income (1.6%). This is largely due to the Scottish Government’s decisions to uprate the Higher Rate threshold by less than inflation in five out of six years, and to increase the Higher Rate and Top Rate by 1p, respectively, from 2018-19.

- At a household level, taxpayers in the lowest 10% of households by income will see little change in the amount of tax paid in 2022-23, in large part because there are fewer taxpayers in the lower income deciles. Households in the top decile will see the largest decrease in income (£1,185).

- Overall, 46% of households will pay less tax, 30% of households will pay the same amount of tax and 24% of households will pay more tax in 2022-23.

- The 2022-23 policy proposal broadly maintains the positive distributional implications of the policy changes since 2016-17, which improved the progressivity of the tax system in Scotland.

The analysis does not consider the 1.9 million individuals, or 41% of adults in Scotland, who will not pay Income Tax in 2022-23 because they earn less than the Personal Allowance, or for example they are in full-time education, have full-time caring responsibilities or are retired. These individuals are not directly affected by the Scottish Government’s Income Tax policy decisions.

Policy changes since 2016-17

Since the Scotland Act 2012 and Scotland Act 2016 gave the Scottish Parliament the power to set (respectively) Income Tax rates and thresholds, the Scottish Government has implemented a series of policy changes on non-savings non dividend (NSND) Income Tax. These have sought to enhance the level of public service provision in Scotland, make the tax system more progressive, protect lower earning taxpayers and support economic growth. These significant policy changes included:

- A cash freeze of the Higher Rate threshold at £43,000 in 2017-18;

- The introduction of a new five-band system in 2018-19, and a below-inflation uplift (of 1%) of the Higher Rate threshold to £43,430;

- A cash freeze of the Higher Rate threshold at £43,430 in 2019-20;

- A cash freeze of the Higher Rate threshold at £43,430 in 2020-21;

- Inflationary uprating (0.5%) of all bands and the Higher Rate threshold in 2021-22;

- A cash freeze of the Higher Rate threshold at £43,662 in 2022-23.

As a result of these changes, there are now differences between the tax systems in Scotland and the rest of the UK. However, as Income Tax is not a fully devolved tax, any distributional impacts of the Scottish Government’s policy decisions need to be considered alongside changes to UK Government tax policy, particularly with regard to the UK-wide Personal Allowance. Over this period, the Personal Allowance increased by more than inflation, from £11,000 in 2016-17 to £12,570 in 2021-22. In the UK Autumn Budget (October 2021), the UK Government confirmed that the Personal Allowance would be frozen at £12,570 from 2022-23 until 2025-2026.

Key facts about Scottish taxpayers in 2022-23

We estimate that there will be around 4.6 million adults living in Scotland in 2022-23 and around 2.7 million Scottish Income taxpayers. This means that a significant proportion, around 41% or 1.9 million adults, will not pay Income Tax. This could be because they in work, but earning less than the Personal Allowance, or they are in full-time education, have full-time caring responsibilities or are retired.

The UK Government’s decision to increase the Personal Allowance by more than inflation over the period 2016-17 to 2021-22 narrowed Scotland’s Income Tax base, compared to inflationary uprating. However, the UK Government’s decision to freeze the Personal Allowance from 2022-23 until 2025-26 will reverse this, widening the tax base in the future.

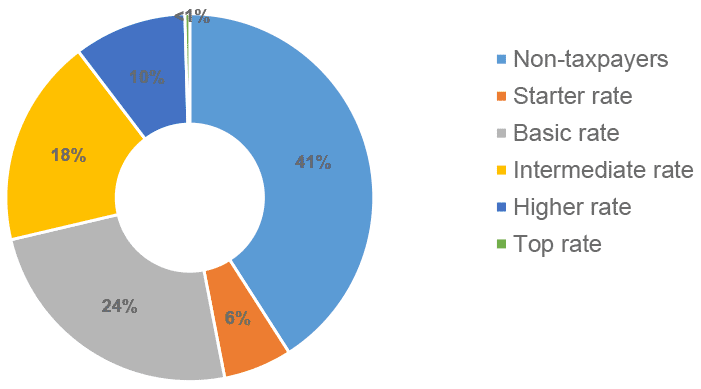

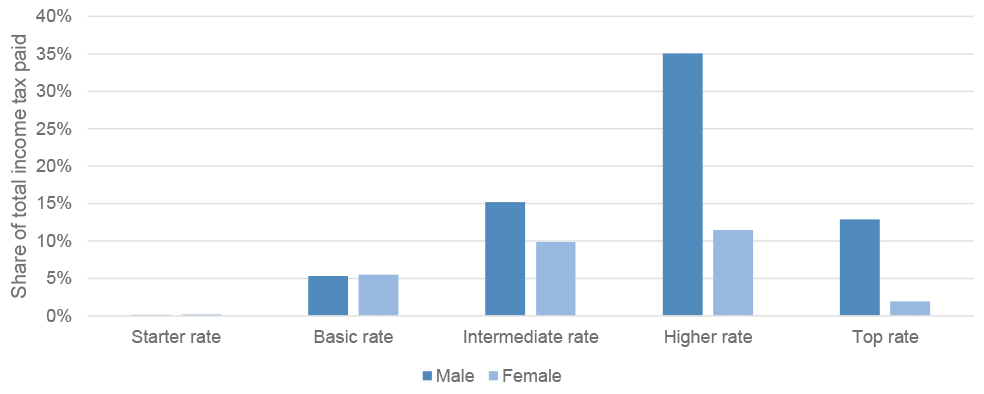

As illustrated in Chart 1, the majority of Scottish taxpayers pay either the Starter Rate (19p), Basic Rate (20p), or the Intermediate Rate (21p) of Income Tax. Only 9.9% of Scottish adults pay the Higher Rate (41p), and less than 1% of the Scottish adult population pay the Top Rate (46p).

Source: Scottish Government Analysis based on SFC forecasts

The threshold at which taxpayers start paying the Intermediate Rate is broadly aligned with the median income of Scottish taxpayers, which is expected to reach around £25,800 in 2022-23. This means that half of all taxpayers in Scotland earn below this level, and half above. Table 1 shows the estimated income distribution of Scottish taxpayers for 2022-23, split into quarters. For example, someone earning between the Personal Allowance (£12,570) and £18,200 would be among the lowest earning 25% of taxpayers in Scotland.

| Taxpayer Income Quartiles | Have annual income of less than |

|---|---|

| 75% | £39,100 |

| 50% (Median Income) | £25,800 |

| 25% | £18,200 |

Distributional analysis

People’s living standards are affected both by the performance of the Scottish economy and by the direct impact of government decisions, including on tax and public spending. Our analysis shows the effect of Income Tax policy on taxpayers in 2022-23 compared to a counterfactual scenario where Income Tax policies announced at and since April 2016-17 were not introduced, and all thresholds and the Personal Allowance were uprated in line with CPI inflation instead. The full methodology is set out in the annex.

This analysis presents only some of the factors which will drive taxpayers’ income and living standards and, importantly, does not take into account the impact of other government policies on the wider Scottish economy, including in the labour market, such as changes to the National Living Wage.

Moreover, recent evidence shows that the economic effects of the COVID-19 pandemic are not felt evenly across different income groups and groups with protected characteristics. The nature of the economic impacts of the pandemic means that customer-facing sectors, such as Retail, Hospitality and Leisure, have been hit particularly hard. Since low income earners, the young and women account for the majority of workers in those sectors, they are more likely to have seen their incomes fall, to have been furloughed or made redundant, although income losses can be observed across the income distribution.[1]

The analysis presented in this paper does not fully reflect these emerging trends as it is based on the latest available, pre-COVID, Income Tax data from the 2018-19 Survey of Personal Incomes (SPI). In order to ensure consistency with the Scottish Fiscal Commission (SFC)’s forecasts, we apply the same economic determinants and assumptions as the SFC to project the data forward to 2022-23. Our results therefore need to be interpreted in the light of these data limitations.

Impact across different levels of taxpayer income

Charts 2 and 3 present the impacts on Scottish taxpayers by income decile. This approach divides the taxpayer population into ten equal groups, with decile 1 representing the 10% of taxpayers with the lowest earnings and decile 10, the 10% of taxpayers with the highest earnings.

However as noted above, 41% of Scottish adults do not pay Income Tax and are therefore not covered by this analysis. Moreover, while Higher and Top Rate taxpayers are expected to make up the highest earning 18% of Scottish taxpayers, some of these individuals may be the main family earner, supporting a partner and/or children.

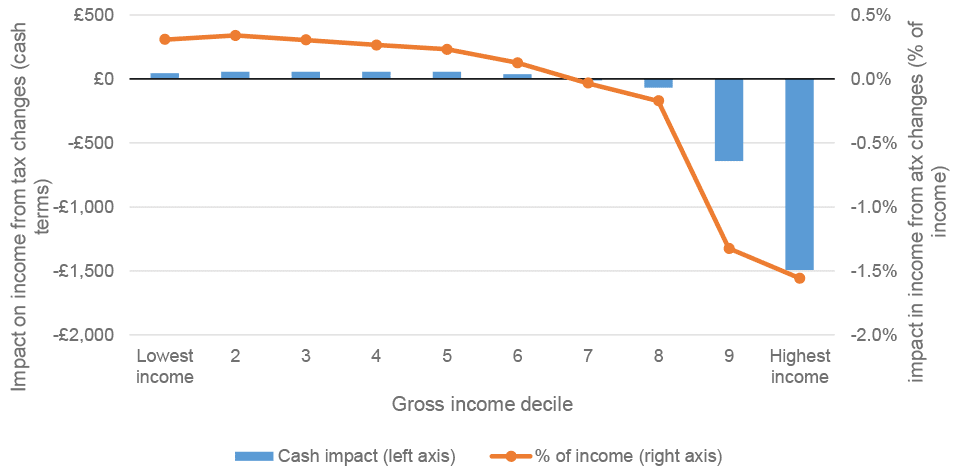

As shown in Chart 2, the Scottish Government’s decisions on Income Tax over the course of the last Parliament and the most recent Scottish Budget, combined with changes in the UK-wide Personal Allowance, have been highly redistributive and protected low and middle income taxpayers, in line with the Scottish Government’s priorities for Income Tax, as set out in The Role of Income Tax in Scotland[2].

As illustrated in Chart 2, taxpayers in the middle of the income distribution will pay marginally less in tax per person (around £56) on average by 2022-23. This is partially due to the introduction of the Starter Rate in 2018-19 which provided a tax saving of up to £21 to all taxpayers by 2022-23, although a larger portion is explained by the above inflation increase in the Personal Allowance. Relative to their gross income, the lowest earning 20% of taxpayers will see the largest decrease in tax (0.3%).

The highest earning 10% will see the largest increase in the amount of tax paid, both in cash terms (£1,490) and relative to their gross income (1.6%). This is largely due to the Scottish Government’s decisions to uprate the Higher Rate threshold by less than inflation in five out of six years and to increase the Higher and Top Rates by 1p from 2018-19 onwards.

Impact across different levels of household income

This section extends the analysis by looking at the impact of the policy changes on household incomes after tax and social security payments, accounting for the number of people in the household. This analysis therefore includes individuals who do not currently pay tax and hence are not directly affected by the tax measures implemented since 2016-17. This means that the deciles shown in the charts below are different from those above, as they cover the entire population rather than just taxpayers.

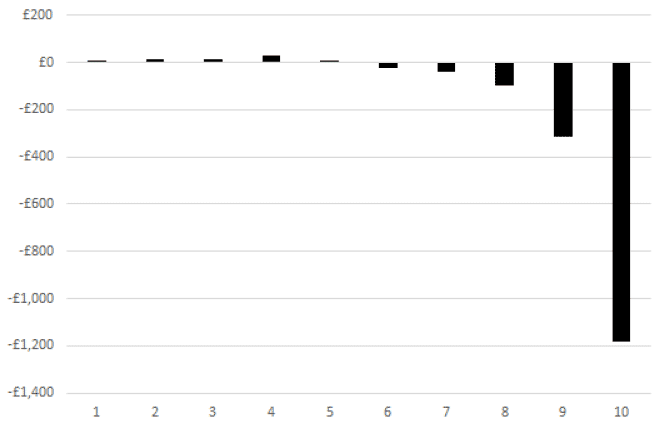

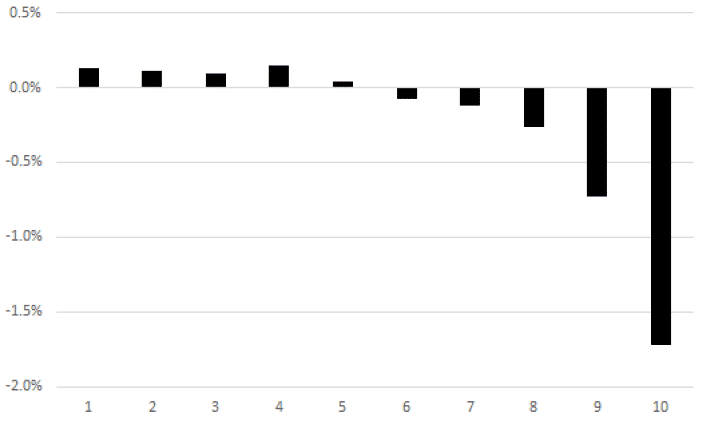

The results, as shown in Charts 3 and 4 below, broadly mirror the findings for the taxpayer population: cumulative tax changes implemented by the Scottish Government, combined with changes in the UK-wide Personal Allowance, have been highly progressive. However, since there are fewer income taxpayers in lower-income deciles, the 10% of households with the lowest incomes will see little change in the amount of tax paid. Households in the 4th decile will see the greatest increase in income, both in cash terms and relative to their gross income, while the highest earning 10% of households will see the largest decrease in income, amounting to £1,185 (1.7%).

Overall, 46% of households will pay less tax, 30% of households will pay the same amount of tax and 24% of households will pay more tax as result of the tax changes implemented since 2016-17.

Impact by equality group

This section explains the impact of the policy changes since 2016-17 on some equality groups, including gender and age.[3]

a) Gender

While women are expected to account for around 52% of all Scottish adults, only 45% are forecast to pay Scottish Income Tax in 2022-23. There are a number of factors explaining this. First, while the proportion of women in work has increased over the past decades, there are still relatively more men than women who are in full-time work. Second, women tend to have lower earnings, on average, than their male counterparts. This in part reflects the fact that women take more time out of the labour market to look after family and children, and are more often the second earners within a household. Additionally, while the gender pay gap has narrowed in the past decades, women continue to be paid less, on average, than their male counterparts for similar jobs.

It is still too early to tell how the COVID-19 pandemic will impact gender equality in the longer term although, as discussed above, initial evidence suggests that the pandemic has had a disproportionate economic and social impact on women. For example, women’s disproportionate shouldering of caring responsibilities may have made it harder to maintain or take on employment, particularly when childcare settings or schools were closed to help prevent the spread of the virus. This is particularly acute for lone parents, the vast majority of whom are women.[4] In the longer term, this might adversely affect work and career progression for mothers.[5]

The pre-COVID trends are also evident in the Income Tax data. Median income of male taxpayers is forecast at £30,400 in 2022-23, compared to £23,200 for women. In addition, men are also more likely to pay the Higher and Top Rate. As a result, male taxpayers are expected to contribute around 69% to total Income Tax liabilities in Scotland in 2022-23. About 48% of Income Tax is paid by male Higher and Top Rate taxpayers, compared to 13% by women paying the Higher and Top Rates, as shown in Chart 5.[6]

b) Impact by age

The majority of Scottish taxpayers (72%) are aged between 25 and 64 years, this is explained by a number of factors. For example, many young adults are still in full-time education or training and are therefore unlikely to earn enough to pay Income Tax. Likewise, those who are of pension age (65+) may have incomes that fall below the Personal Allowance.

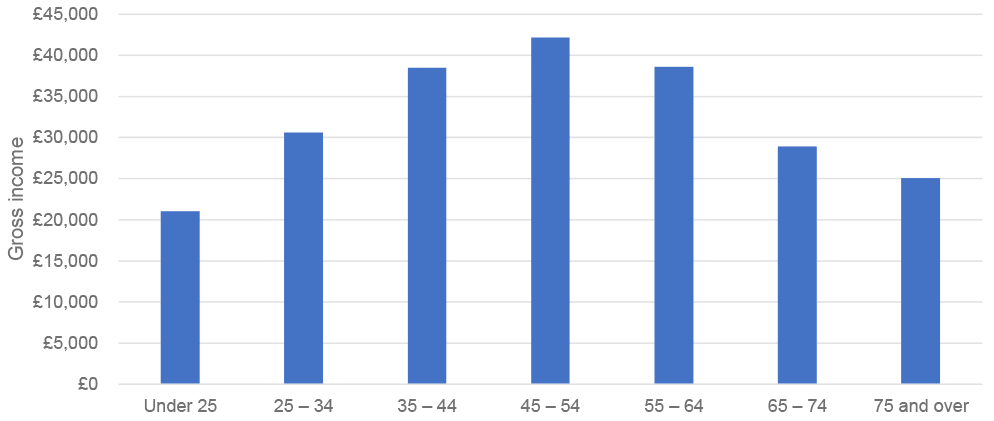

For many taxpayers, average earnings tend to peak in middle age. Taxpayers aged between 45-54 years are expected to have the highest average income in 2022-23, at around £42,000 a year, as shown in Chart 6. As a result, taxpayers in this age bracket are expected to make the largest contribution to Income Tax liabilities in 2022-23, at around 26% of total liabilities.

As noted above, these projections are based on pre-COVID trends and young people have borne the brunt of the economic impacts of COVID-19. Our analysis is consistent with the SFC’s forecasts which assume that labour force participation rates amongst the 16-24 year olds will decrease as a result of COVID-19.

c) Disability

The evidence base on the incomes of, and Income Tax paid by, disabled people is limited. However, there is some evidence that poverty rates remain higher for households with a disabled adult.[7]

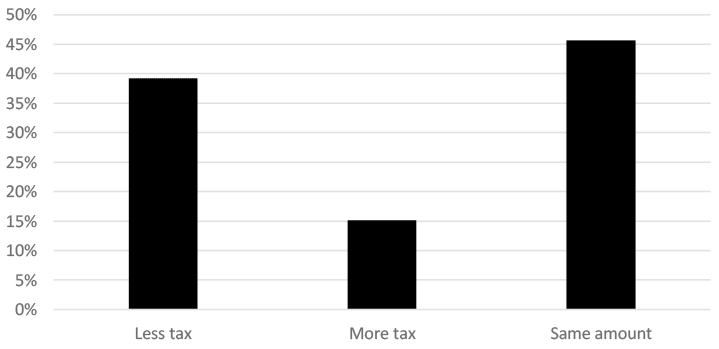

It is possible to report the impact of the Income Tax policy according to households with and without disabled adults (see Chart 7). For households with disabled adults, 39% will pay less tax, 46% will pay the same amount and 15% will pay more tax as a result of changes in income tax since 2016-17. The higher proportion of households with a disabled adult that will see no change in Income Tax reflects the fact that a higher proportion of such households do not contain anyone who earns above the Personal Allowance and are therefore not subject to Income Tax. Note that this analysis uses the core definition of disability as per the Equality Act.

Contact

Email: ellis.reilly@gov.scot