Publication - Research and analysis

Scottish economic bulletin: July 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Conditions

Business activity and optimism improved in June, however demand and cost pressures remain challenging.

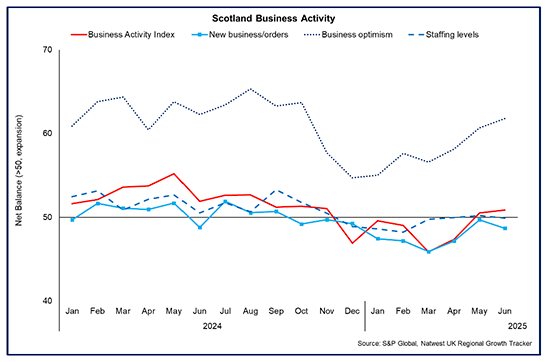

Business Activity

- The RBS Growth Tracker business survey reported that private sector business activity grew for a second consecutive month in June following a six month period of contraction. The Business Activity Index rose to 50.9 (a reading above 50 indicates growing activity) indicating that the pick-up in growth remains modest.[7]

- Furthermore, demand conditions remain challenging, particularly in the manufacturing sector, with businesses continuing to report a fall in new work orders (48.7) while staffing levels remained broadly unchanged (49.9). Despite this, business optimism improved for a third consecutive month (61.8), rising to its highest level since October last year.

Business Concerns

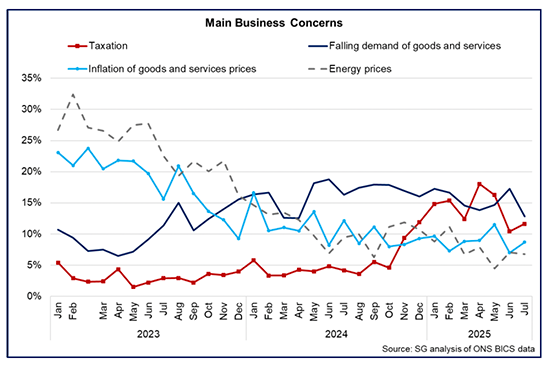

- Key business concerns during 2025 have been falling demand and taxation, followed by inflation and energy prices. The latest Business Insights and Conditions Survey (BICS) for July shows that demand for goods and services continues to be the most commonly cited main concern by businesses in Scotland (12.8%), though its share fell from 17.3% in June to its lowest level since April 2024.[8]

- Taxation as a main concern rose from 10.4% in June to 11.6% in July, and while it is lower than its recent peak of 18% in April when the increase in employer NICs was implemented, it remains higher than its general level during 2023 and 2024. This elevation in concern regarding taxation is broadly consistent with the Scottish Chambers of Commerce (SCC) Quarterly Economic Indicator business survey for Q2 2025, which reported that taxation remained the key concern among Scottish businesses with 70% citing increased concern from taxation, up 40% over the past year.[9]

Box: Modelling the Economic Impact of US Tariffs on Scotland and the rest of the World

- US tariff increases are expected to have a significant impact on the global economy. The Scottish Government’s Office of the Chief Economic Adviser (OCEA) has carried out detailed trade modelling based on the structural gravity framework using our in-house Scotland-specific model. This allows us to simulate the effect on international trade from the tariff increases implemented or proposed by the US and retaliating countries.

- The tariff scenario modelled is based on the tariffs in place as of June 2025. This includes a suite of measures imposed against China, Mexico and Canada; product specific measures (steel, aluminium, cars and car parts); 10% additional tariff applied by USA on imports of most products from most partners; as well as hypothetical 25% tariffs on pharmaceuticals and semiconductors. Bilateral agreements to reduce tariffs are not modelled. For the full description of the tariff scenario, as well as more details on the methodology and results, please see the accompanying technical note.[10]

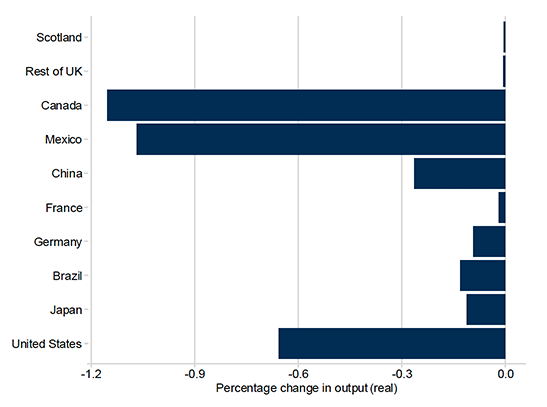

- OCEA modelling finds that global output and global trade could be 0.3% and 7% lower in the long run (roughly 10–15 years) as a result of the increased tariffs. We find Scotland and the rest of the UK to be less exposed than many other countries, with overall output not expected to be significantly negatively impacted.

Chart: International Output

- Directly targeted countries (Canada, Mexico, China) tend to be hardest hit. The USA is also one of the worst affected countries. The graph above includes retaliation by China and Canada, but even without this retaliation, the USA’s economy is impacted negatively. This is consistent with economic theory: while high tariffs can protect domestic industries, they are likely to have wider negative impacts in terms of disrupting supply chains, increasing prices and reducing consumption.

- Of the countries not directly targeted, some fare worse than others – the UK is less affected than Germany, Brazil, and Japan. These results don’t include the effect of the UK–US Economic Prosperity Deal, which might be expected to reduce the impact on the UK further, or could even result in positive results for the UK, as the UK may be able to benefit from reduced competition from other countries facing higher tariffs.

- The impact of the increased tariffs on Scotland is expected to be relatively limited, but can vary between different sectors of the economy and between individual businesses. Total export value is found to be 0.2% lower, but exports of metals and metal products are found to be 1.6% lower, while exports of textiles, clothes, and leather are found to be 1.4% higher than without the modelled tariff increases. Other sectors showing a potential for increased exports are computer, electronic, optical, and electrical equipment, as well as rubber, plastic, and non-metallic minerals. All other sectors show either no effect or a reduction in exports.

- This modelling is not a forecast of future changes but a counterfactual analysis of a world with the higher tariffs compared to a world with the pre-2025 tariff baseline. It assumes that the modelled tariffs will be in place for several years and the economy has time to find a new equilibrium. It does not take into account changes in investment decisions, supply chain effects, or short-term disruption caused by uncertainty.

- The tariffs implemented by the US have changed several times in recent months and this uncertainty is likely to continue. Some details of this modelling may become less relevant as the landscape continues to shift, but the following key takeaways are likely to continue to apply:

- Scotland and the rest of the UK are relatively less exposed to US tariffs than other countries (although the impact on individual companies may still be significant). This is true even without a bilateral agreement cancelling certain tariff increases.

- As well as downsides, there may be some opportunities resulting from preferential tariff rates and Scotland’s comparative advantage in certain sectors. However, these tend not to be in Scotland’s top export sectors to the US and so are likely to be limited in scope.

Business Costs

- The RBS Growth Tracker business survey indicated that business input price inflation picked up slightly in June though remained lower than earlier in the year while output price inflation slowed notably to its lowest rate since July 2024. This potentially indicates that businesses are further absorbing some higher costs to maintain price competitiveness amid concerns of falling demand.[11]

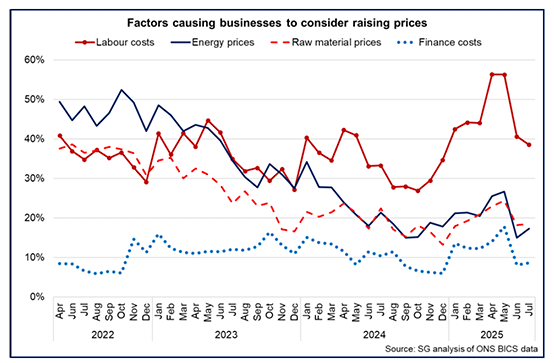

- This pattern is consistent with BICS indicators showing that the proportion of businesses considering price increases has fallen in recent months from 40.3% in May to 15.6% in July. The recent fall in the share of businesses considering price increases has been accompanied by a corresponding increase in the share of businesses reporting prices will stay the same (67.3%).[12]

- Labour costs remained the most frequently mentioned driver of businesses considering raising prices (38.6%), followed by raw material costs (18.5%). The rise in labour cost pressures remains a common theme across businesses surveys reflecting the elevated pace of wage growth over the past 18 months alongside the recent increase in employer National Insurance Contributions and National Living Wage.

- The combination of cost challenges alongside concerns of falling demand continues to present challenging business conditions for considering the extent to which to absorb increased costs or to pass them through to customers, and is sector specific. The SCC Quarterly Economic Indicator for Q2 2025 reported that an increased share of businesses (65%) anticipate that they will be increasing prices in the next quarter.[13] The Bank of England Agent’s Summary of Business Conditions for Q2 2025 reported that the pass-through of higher labour and Extended Producer Responsibility costs introduced in April is, to date, more advanced in goods than in consumer services at a UK level.[14]

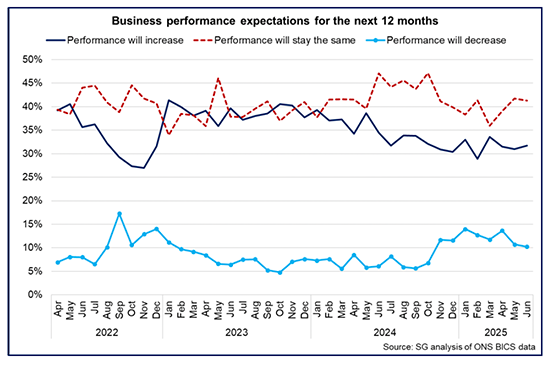

Business Optimism

- Business optimism continues to be impacted by elevated global economic uncertainty and key concerns regarding demand and taxation, although there are indications that it remains resilient. Despite the recent weakening in growth, the RBS Growth Tracker business survey reported that business optimism improved for a third consecutive month in June (61.8) and to its highest level since October last year.[15]

- Furthermore, latest BICS data for June shows that the greatest share of businesses (41.3%) continue to expect their business performance to stay the same over the next 12 months while the share of businesses expecting their performance to improve increased slightly in June to 31.7% while the share of businesses expecting performance to decrease (10.3%) continued to ease back from higher rates earlier in the year.

Contact

Email: economic.statistics@gov.scot