Publication - Research and analysis

Scottish economic bulletin: February 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Consumer Activity

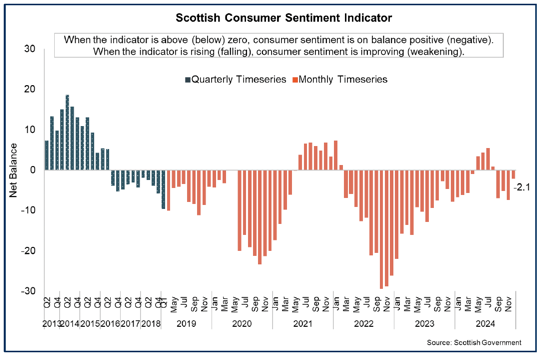

Consumer sentiment weakened in the final quarter of 2024, though monthly data points to some improvement in December.

Consumer Sentiment

- The Scottish Consumer Sentiment Indicator reflects how households think the economy is performing, how secure they feel about their household finances and how relaxed they feel about spending money.

- Consumer sentiment weakened across in the final quarter of 2024 compared to earlier in the year and re-entered negative territory having strengthened over 2023 and the first half of 2024. However, the latest monthly data show consumer sentiment rose 5.2 points in the month of December to -2.1. This is its highest level since August, when the indicator was in positive territory.[16]

- The rise in sentiment in December was driven by improvements in all five sub-indicators of sentiement regarding current and future economic performance and household financial security, and attitudes to spending.

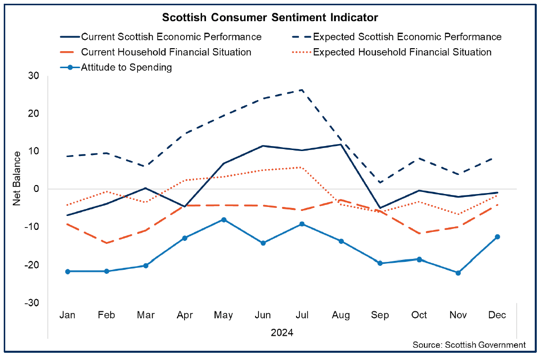

- The attitute to spending indicator saw the largest growth in sentiment in December, and increased by 9.4 points to -12.6, followed by sentiment on current household finances (up 5.8 points to -4.2) and expected household finances (up 5 points to -1.6).

- Sentiment on economic performance, also improved with respondents on balance continuing to expect economic performance to strengthen over the next year.

- The upward tick in the latest data, alongisde the weakening in sentiment during the second half of 2024, is broadly consistent with consumer sentiment at a UK level, with the GfK Consumer Sentiment Indicator rising by one point in December following a decline in earlier months.[17]

Spending and Cost of Living

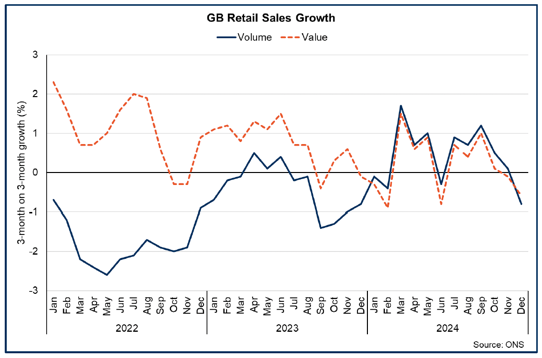

- Retail sales in Great Britain have grown over the past year in both volume and value terms (1.9% and 1.1% respectively) however latest data indicates the pace of growth slowed during the second half of 2024 with sales volumes contracting by 0.8% in the fourth quarter and by 0.6% in value terms.[18]

- Lower and more stable inflation and reductions in interest rates are providing improving conditions for consumption, though the full benefits are feeding through gradually, and higher price levels and cost of living challenges are continuing to impact households.

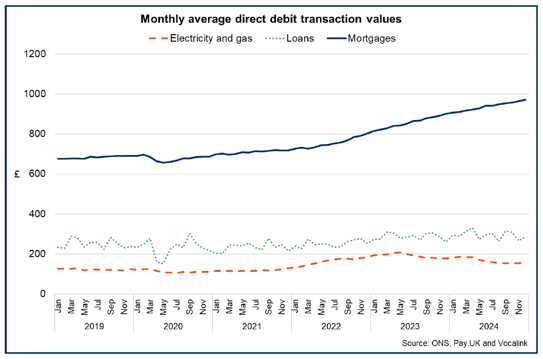

- At a UK level, average monthly direct debit transaction values rose 2.3% over the year to December 2024, driven in part by higher mortgage and loan payments. The average transaction amount for mortgages increased by 7.6% over the year to £970.98, with the pace of growth continuing to ease from earlier in the year and 2023.[19] The average transaction amount for electricity and gas fell 10% over the year to £163.31 in December. However energy payments have increased on a monthly basis at the end of the year, in part reflecting the energy price cap rise.

- Direct debit failure rates due to insufficient funds remain elevated compared to pre-pandemic levels, though have been more stable over the past year. Total direct debit failure rate in December 2024 was 2.19% (slightly above the 2024 average of 2.17%). Failure rates for water, electricity and gas and loans have all increased over the year, however direct debit failure rates for mortgages have fallen from 1% in December 2023 to 0.94% in December.

- In December, the ONS Public Opinions and Social Trends survey showed that 32% of respondents found it very or somewhat difficult to afford energy bill payments (down from a peak of 49% in 2023) while 30% of respondents said the same for mortgage and rent payments (down from a peak of 46% in 2023).[20]

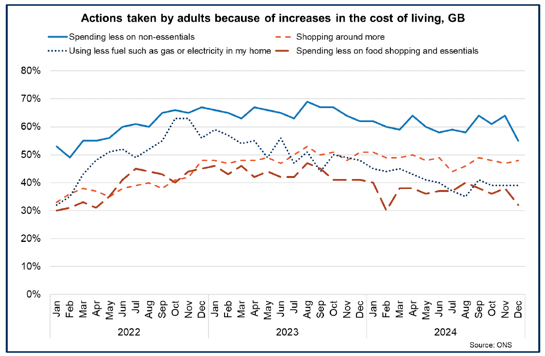

- The most common actions people are taking in response to the increased cost of living continue to be spending less on non-essentials (55%) and shopping around more (48%). A further 39% reported using less fuel such as gas or electricity in their home and 32% reported spending less on food shopping and essentials.

- These figures have remained broadly consistent over the course of 2024. However, over the longer term, following a relatively sharper uptake in these actions over 2022 and 2023, the flatter downward trajectory over 2024 indicates that cost of living continues to be a challenge to household budgets, and that it will take time for a stabilising price environment and stronger earnings growth to fully feed influence consumer behaviour.

Contact

Email: economic.statistics@gov.scot