Cost of Living (Tenant Protection) (Scotland) Act 2022 - proposed extension: statement of reasons

We have prepared this Statement of Reasons to set out why The Cost of Living (Tenant Protection) (Scotland) Act 2022 (Amendment of Expiry Dates and Rent Cap Modification) Regulations 2023 (“the extension regulations”) should be made.

Annex D

Key updates to the business regulatory impact assessment (BRIA) and financial memorandum

This Annex sets out key estimates which were set out in the Business Regulatory Impact Assessment (BRIA) and Financial Memorandum which accompanied the introduction of the Cost of Living (Tenant Protection) Bill, and which require significant updating due to extending the cap by an additional six months, with different provisions applying to rent increases.

In the BRIA/Financial Memorandum, it was estimated that around 55,000 private rented properties may have increased rents in the first six months in the absence of legislation. This was based on an assumption that 50% of landlords would raise rents,[15] applied to the number of tenancies where there would be an opportunity to raise rents in a six month period.[16] High and low estimates were provided around this central estimate to reflect potential behaviour change by landlords given current economic conditions: the high estimate of 70% was designed to reflect the possibility that landlords may have been more likely than usual to increase rents due to the high level of inflation and increases in mortgage costs, and the low estimate of 30% to represent the possibility that landlords may have been slower than usual to increase rents due to the economic pressures on tenants, which gives a range of 33,000 to 77,000.

A six month extension implies that a further 55,000 properties may have seen increased rents during this second six-month period if there had been no legislation. Assuming that the landlords of the 55,000 properties where rents would otherwise have been increased during the first six months would now also wish to increase rents, that implies that around 110,000 properties may be affected by the rent provisions that apply to the six month extension. Applying the same high and low scenarios to account for behaviour change implies a range of 66,000 to 154,000 properties which may be affected.

The amount of rent foregone by landlords will depend on what rent increase they would otherwise have been able to implement. Recent data from letting agents (which relates to the latter half of last year) indicates that increases in new let rents were around double digits in Scotland (Rightmove – 13% in Q3 2022, Citylets – 8.3% in Q3 2022, and Zoopla – 11.4% in Oct 2022).[17] However, the period of extension will cover rent increase notices issued from April to September 2023. During the course of 2023, inflation is projected to fall gradually, and this may similarly be reflected in rental trends. For example, Zoopla project that rental growth may ease towards 4%-5% by the end of 2023.[18] Furthermore, the relevant rental increase affected by this legislation is in rents for existing tenants, rather than new let rents, and the gap in average rent levels between existing and new tenants suggests that rent increases for existing tenants may be lower on average than for new tenants.

We therefore cost three scenarios relating to what rental growth for existing tenants would have been in the absence of legislation:

- i. Rental growth of 3% or below – there will be no foregone rental income

- ii. Rental growth of 5% – with a permitted rent increase of 3%, the foregone rental growth is 2%

- iii. Rental growth of 10% – with a permitted rent increase of 3%, the foregone rental growth is 7%. This scenario is a very much an upper-end scenario, which assumes that new let rental growth will remain at the elevated level recorded in the latter half of 2022 despite projected falls in inflation, and also assumes that rents on existing lets grow at the same rate as new let rents.

As in the BRIA/Financial Memorandum, the impact of the rent growth cap is costed on an average two bedroom monthly rent of £722. This gives the following scenarios:

| Assumed rental growth in absence of cap | |||

|---|---|---|---|

| 3% or lower | 5% | 10% | |

| Foregone revenue per property per month | - | £14 | £51 |

The next table presents estimates of foregone rental income across the private rental sector as whole. This depends both on the assumed rental growth in the absence of a cap, as well as the number of properties which would have experienced rent increases in the business-as-usual scenario. As was explained above, the central scenario is based on 110,000 properties being affected, with a range of 66,000 to 154,000 to reflect behavioural responses by landlords.

| Assumed rental growth in absence of cap | ||||

|---|---|---|---|---|

| 3% | 5% | 10% | ||

| Number of properties which would have experienced a rent increase | 66,000 | - | £5.7m | £20.0m |

| 110,000 | - | £9.5m | £33.4m | |

| 154,000 | - | £13.3m | £46.7m | |

It should be noted that the table above only includes the impact of the option to increase rents under the general 3% provision, and does not include the alternative option to increase rents up to a maximum of 6% if prescribed property costs have increased. Where a landlord does so, then the foregone revenue will be lower than presented in the above tables.

One type of prescribed property costs where there have been significant increases is mortgage costs. It is estimated that around 19% of private rented properties in Scotland have either a variable rate mortgage, or a fixed rate mortgage which will reach its end of term during a 12 month period.[19] Applying this estimate to the central estimate of 110,000 properties where the landlord may wish to raise rents results in an estimate of around 21,000 properties where the landlord may have experienced an increase in mortgage costs and may wish to raise the rent. The average increase in mortgage costs could be in the region of £300 per month. It should be noted that data limitations mean this should be regarded as an indicative costing only, and that it also depends on mortgage rates remaining at the elevated levels reached towards the end of last year.[20]

An increase of £300 equates to around 40% of an average two-bed rent, but it should be borne in mind that:

- even in normal market conditions, a seller is unlikely to pass anywhere near a 100% of a cost increase onto buyers, since the market price is constrained by the buyers' responsiveness to price increases. In the current rental market, tenants are particularly affected by cost of living pressures, which will limit their ability to pay higher rents, and in turn limit how much the market rent can increase by;

- this is particularly the case when very large cost pressures affect only a segment of the market, since the market rent is determined independently of an individual landlord's financing decisions since they will be competing with other landlords who have made different financing decisions.

One illustration is that data from Zoopla report that annual growth in new let rents in Scotland in October 2022, following the surge in mortgage rates after the UK Government mini-budget in September 2022, was 11.3%, well short of the increase in costs that might have been incurred by some landlords due to higher mortgage costs, despite new let rents being free to be set at market rates.

In terms of the number of applications that might be received by Rent Service Scotland for the 6% increase due to prescribed property costs, in the BRIA/Financial Memorandum accompanying the initial legislation, various scenarios were set out. Although it was estimated that there could be at least 5,500 eligible cases (just from the mortgage cost element[21]), it was argued that many landlords may decide not to go through the process for an average increase in the region of £20 per month for a period of up to six months, particularly if they thought there might be the potential to increase rents by more, either due to the expiry of the initial six month period of the legislation, or because there might be a change in tenant. Accordingly, a range of scenarios was presented, ranging from 125 in the lowest scenario, to 250, 500 or 1,000 cases in the highest scenario.

As at 31 December 2022, Rent Service Scotland had received 12 applications (of which 10 were valid) from landlords in relation to prescribed costs. This suggests that over the full six months of initial period, the number of applications will fall well below the number set out in the low scenario. However, to the extent that this was due to landlords choosing to wait to see if the provisions would end after six months, there could be a substantial increase due to the extension for another six month period. This would imply a greater likelihood that the number of applications in the next period could reach the highest scenario of 1,000 applications. However, given that landlords are now able to raise rents by up to 3% without applying to Rent Service Scotland in relation to prescribed property costs, many landlords who have experienced an increase in mortgage costs may chose to go down the former route.

In addition to applications to Rent Service Scotland in respect of prescribed property costs, tenants also have the right to refer a rent increase notice to a Rent Officer to verify whether a proposed rent increase is in line with the rent cap. Although, as set out above, the number of cases where rents can be increased could be in the region of 110,000, we would anticipate that any such referrals to the Rent Service Scotland would be substantially lower than this, given that the operation of the rent cap in respect of this element is a simple uplift of 3% of the current rent. The verification check by Rent Service Scotland will require Rent Officers to verify there have been no increases in the previous year, confirm the existing rent and calculate the 3% cap and issue a verification decision to the tenant. Although the calculation is straightforward, the main burden may be ensuring that the necessary documentation is provided to produce a decision within timescales prior to the effective date. It is difficult to quantify how many tenants might apply under this provision. There is a possibility that there could be a large volume of applications if tenants whose increase is in compliance with the regulations still contact the Rent Service Scotland. We will provide clear guidance and undertake proactive communication to minimise the number of such applications.

The extension of the rent cap for a further 6 months may have an impact on certain incentives to invest. The incentive to invest in new supply will not be initially affected because the cap does not apply to new lets. Furthermore, as the legislation cannot be extended beyond 31 March 2024 at the latest, landlords of new units which are let for the first time after 31 March 2023 are unlikely to raise rents for sitting tenants during the period of operation of the legislation.

However, there is a degree of tension between protecting existing tenants and preserving incentives for landlords to invest in the quality of the property and continue to provide existing rental accommodation. In extending the protection for tenants for a further six months, the intention has been to ensure that any rent increases are sufficiently modest so that they do not impose significant additional pressure on tenant budgets while cost of living pressures remain acute (which will help them to sustain their tenancy), while allowing some uplift for landlords to help them meet any cost increases related to maintaining properties to the required standard, or from higher mortgage rates, or other sources. We believe that raising the general rent cap to 3%, or alternatively allowing rent increases of up to 6% based on a 50:50 sharing of prescribed property costs, will achieve this balance.

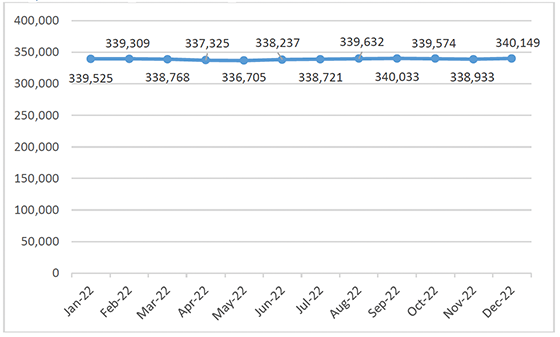

On the issue of the overall supply of privately rented properties, it is worth considering trends in the number of properties registered on the Scottish Landlord Register. This gives a comprehensive picture of the Scottish private rented sector, although there are some limitations, such as the fact that registrations last for a period of three years and there could be a time lag in landlords de-registering properties which are no longer available for rent. In the case of any landlords looking to leave the sector or reduce their portfolio, it should be recognised that the process could take several months from freeing up properties to completing sales.

Nevertheless, subject to these limitations, Figure 1 shows that the number of registrations has been steady across the whole of 2022. In particular, the number of properties registered in December 2022 was 0.2% higher than in August 2022. We will continue to track data from the Scottish Landlord Register on a monthly basis.

Contact

Email: housing.legislation@gov.scot