How to pay for a Minimum Income Guarantee

On behalf of the independent Minimum Income Guarantee Expert Group, WPI Economics delivered a report which provides key recommendations around how the revenue could be raised to pay for a Minimum Income Guarantee.

Exploring key revenue-raising options in more detail

In the section we discuss in more detail seven scenarios from the options outlined in the chapter above. These scenarios were selected as options that the Expert Group think could play an important role in financing a MIG across both the short term and long term. The scenarios we explore are set out in Table 14.

| Revenue-raising options | Scenario under consideration | Stage of powers required |

|---|---|---|

| Scenario 1: Reducing Scottish Income Tax thresholds | Reducing the Higher Rate threshold to £40,000 AND Reducing the Additional Rate threshold to £58,285 | Stage 1 |

| Scenario 2: Changing the council tax ‘multipliers’ | Increasing council tax across a five-year period by:

|

Stage 1 |

| Scenario 3: Reducing the Scottish Income Tax personal allowance | Reducing the Scottish Income Tax personal allowance by £5,000 from £12,570 to £7,570. | Stage 2 |

| Scenario 4: Expanding Scottish Income Tax to dividends and savings | Applying Scottish Income Tax rates, bands and thresholds for earned income to income from savings and dividends. | Stage 2 |

| Scenario 5: Increasing NICs rates | Increasing the main employee rate, employee rate above UEL and employer rate by 1ppt.[147] | Stage 3 |

| Scenario 6: Increasing and broadening the VAT base | Increasing the standard and reduced rate of VAT by 1ppt. AND Scrapping the zero rate and setting this at the new reduced rate. | Stage 3 |

| Scenario 7: Increasing excise duties | Increasing fuel, alcohol and tobacco duties by 10% | Stage 3 |

For each of these scenarios, we provided an assessment of the following:

- Overall purpose of the revenue-raising option;

- Delivery and implementation considerations which includes a ‘high – low’ RAG rating of:

a. Administrative feasibility: Assessing the administrative and logistical complexity of delivering and implementing the option;

b. Political desirability: Assessing the support of key political actors;

c. Policy viability: Assessing the trade-offs between expected impacts and costs from existing policy evidence;

- A discussion of the revenue-raising potential and costs of the scenario, drawing upon existing estimates and original microsimulation analysis which provides a static estimate of the expected total fiscal cost of the tax changes (namely, accounting for any increased social security spending as a result of the modelled tax changes);

- A discussion of the distributional impacts of the scenarios, drawing upon existing literature and original microsimulation of the impact of the tax change before housing costs, average household disposable income (in cash terms and proportionally) and the number of gainers and losers from the tax change across income deciles; and

- A discussion of the anticipated wider impacts, considering likely behavioural changes,[148] economic theory and a ‘high – low’ RAG rating of the risk of a negative impact on a range of macroeconomic metrics (GDP, productivity, labour market participation, employment rates, investment).

Our full modelling results are presented in Annex I and a modelling explanatory note is outlined in Annex II.

Scenario 1: Reducing Scottish Income Tax thresholds (Stage 1)

Purpose

Reducing the thresholds at which people pay Scottish Income Tax would raise additional revenue under existing powers. Since 2017-18, Scotland has had powers to vary its income tax schedule and has continuously done so since.

By changing thresholds, more taxpayers are contributing additional tax revenue without the need for the introduction of any additional tax bands or for changes to existing rates. The proposed reforms in the scenario could be categorised as a way to broaden the income tax burden, but in a targeted manner on taxpayers earning above median income.

Delivery and implementation

Administrative feasibility

High

Politacal desirability

Low

Policy viability

Medium

Changing Scottish Income Tax thresholds would come with limited administrative challenges and could be enacted quickly through the Scottish Government’s annual Budget. There would be no change to how the revenue would be collected, making the administrative feasibility of this policy high. However, there appears to be limited political desirability for any further reforms to Scottish Income Tax, and current political focus is on allowing recent changes to the Scottish Income Tax schedule to be embedded and evaluated. The Scottish Government’s 2024 Tax Strategy has committed to maintaining the Scottish Higher, Advanced and Top Rate thresholds at current levels, albeit with scope for this to be annually reviewed at the Budget.[149]

Revenue-raising potential and cost

The amount raised from a change to Scottish Income Tax thresholds in Scotland would depend on the exact gross income the thresholds were set at, as well as any associated behavioural changes. We have modelled a scenario to lower the 42% Higher Rate threshold to £40,000 and the 45% Advanced Rate to £58,285. Our modelling found that these reduction to Scottish Income Tax thresholds would raise £672m per year.

Our modelling only captures the static impact of the change, and estimates from modelling using Landman Economics’ tax-transfer model (calibrated to Scottish Government assumptions on behavioural change) suggest £502m would be raised from reducing the Higher Rate threshold to £40,000 and £68m from the introduction and widening of a 45% Advanced Rate.[150] When compared to our static modelling, this suggests around £100m would be lost due to behavioural changes.

Further additional revenue could be raised by changing where the thresholds of other tax bands are set. In addition, coupling these changes to thresholds with changes to the tax rate could also raise further additional revenue. However, this would come with some behavioural impacts, and the Scottish Government’s 2024 Tax Strategy has committed to not increase the rates of Scottish Income Tax until at least May 2026.[151]

Distributional impact

The proposed reforms to Scottish Income Tax thresholds would be considered progressive. In particular, reform to the Advanced Rate threshold affects those with full-time gross earnings in Scotland that would put someone in the 9th income decile.[152] Our modelling in Figure 1 shows the greatest cash and proportional effect of the policy was felt by those in the top two income deciles.

However, in 2025-26 it is expected that less than 12% of taxpayers in Scotland will pay the Higher Rate and only 2.8% of Scottish taxpayers will pay the Advanced Rate.[153] There is therefore some concern that too much focus on the progressivity of the personal tax system distorts the best way of revenue-raising through personal taxation. As countries that raise more revenue than the UK show, there is often greater focus on having higher rates and lower thresholds to ensure a greater number of middle earners are paying more tax.[154]

Source: IPPR Tax-Benefit Model, Centre for Social Policy Studies.

Anticipated wider impacts

Negative impact on:

GDP: Low-Medium

Productivity: Low

Labour market participation: Medium

Employment rate: Medium

Investment levels: Low

Most concern amongst analysts is around the behavioural impact of income tax changes, although there is an acknowledgment that the size of these impacts is uncertain. At the higher end of the income distribution, it is often assumed that paying more in personal taxes reduces the incentive to work overtime or take on higher-paid or higher skilled jobs, and could support decisions for outward migration to other parts of the UK.[155] However, it should be noted that personal tax is often one of many factors in mobility decisions and HMRC analysis of 2018 and 2019 Scottish Income Tax changes concluded that there was ‘no evidence of changes in labour market participation and some limited evidence of a decrease in net cross-border migration (number of immigrants minus the number of emigrants) for Scottish taxpayers above the Higher rate threshold following the Scottish Income Tax changes’.[156]

Analysis by the Fraser of Allander Institute has suggested that accounting for behavioural changes reduces the revenue raised through a 45% Advanced Rate set at £58,285 by over a third (39%).[157] We have seen how previous dynamic modelling by Landman Economics does suggest that revenue from the reforms could be markedly below that of static estimates due to behavioural assumptions. Moreover, high income earners could respond to changes in thresholds by relatively easily reclassifying their income as dividends or capital gains in order to pay lower rates of tax. This is because the Scottish Government currently lacks powers to extend Scottish Income Tax to these types of income.[158]

More broadly, research has suggested that the overall macroeconomic impact of higher income tax is limited. The net impact of income tax increases on growth is often uncertain. However, macroeconomic modelling by the National Institute of Economic and Social Research (NIESR) simulated the effect on GDP of a change in tax rates that could raise an average of £3bn of income per year. This modelling found that funding this through income tax would have by far the least negative effect on GDP and that, in the long run, the economy could return to baseline levels with a slight increase in potential output.[159] Other research has found that productivity and investment are not so much hampered by higher income taxes per se, rather by a lack of certainty and stability within the tax system.[160]

Scenario 2: Changing the council tax multipliers (Stage 1)

Purpose

Changing the council tax multipliers would raise additional revenue from council tax under the Scottish Government’s current powers. The multipliers are set by central government and determine the rate of council tax paid by properties in different bands. This is as a fixed proportion of the amount charged by local authorities for Band D properties in their area.

The change modelled below would reduce the tax gap between Scotland and England in council tax rates, as well as increase the overall progressivity of Scotland’s council tax system.

Delivery and implementation

Administrative feasibility

High

Political desirability

High

Policy viability

High

A change to the council tax multipliers could be enacted quickly and would require no change to the existing revenue collection mechanisms in Scotland. This makes the administrative feasibility of this option high. However, the political desirability is more unclear. Although the Scottish Government is set to consult on council tax reforms in 2025,[161] previous 2023 proposals to change the council tax multipliers for properties in Bands E-H were ultimately not taken forward after consultation. Many respondents to the 2023 consultation raised concern about the affordability of the proposed increases at a time of a broader cost-of-living crisis.[162]

Revenue-raising potential and cost

The amount raised from a change to the council tax multipliers in Scotland would depend on the rate set. We have modelled a scenario that combines the 2023 Fairer Council Tax consultation proposals with annual increases in the base rate of council tax for Band A-D properties and multipliers for Band E-H properties by the end of an indicative five-year parliamentary term.[163] These increases are set out in Table 15, and would see all households pay more in council tax, with those living in properties in higher bands experiencing the largest increases.

| Band | Year 1 | Year 2, Year 3, Year 4, Year 5 | Total increase over five-year period |

|---|---|---|---|

| A-D | Annual 3% (plus inflation) increase | 28% | |

| E | 7.5% increase (plus inflation) | Annual 4% (plus inflation) increase | 39% |

| F | 12.5% increase (plus inflation) | Annual 5% (plus inflation) increase | 51% |

| G | 17.5% increase (plus inflation) | Annual 7.5% (plus inflation) increase | 73% |

| H | 22.5% increase (plus inflation) | Annual 10% (plus inflation) increase | 97% |

Our modelling found that these council tax reforms would raise:

- £163m in Year 1

- £242m in Year 2

- £322m in Year 3

- £406m in Year 4

- £497m in Year 5

Distributional impact

As property is the ‘most valuable form of wealth’ held by households in Scotland, many argue it is the natural starting point for improving wealth taxation, and that reforms to council tax can help improve equality, including gender equality. While property value is not perfectly correlated with income level, analysis by IPPR Scotland found that most lower-income households live in Band A or B properties, and that the current system is regressive.[164]

However, there are concerns that raising council tax on higher value properties could negatively impact pensioners on fixed incomes, low- to middle-income households that might not be eligible for additional support, and families who would have less disposable income with which to support their children.

Our modelling finds that, across the five years of the policy, the proposed increase in council tax is progressive in cash terms, with those in higher income deciles contributing more of their average disposable income across the five years of the policy.

However, the policy has a less progressive proportional impact. Proportionally across the five years, the impact of the policy falls the greatest on those in 7th, 8th and 9th income deciles, and those in the 3rd and 4th deciles are the least impacted. The exception is the first year of the policy. As shown in Figure 2, a majority of the lower- and middle-income deciles (2nd through to 6th) are proportionally the least impacted.

Although our modelling accounts for social security changes that may help mitigate the council tax increases, we find that, in each of the five years, the impact on those in the lowest-income deciles is greater than those in the highest-income decile. Figure 3 shows how the fifth and final year of the policy is indicative of this trend. Despite this, 100% of those in the top-income decile loss out from the policy every year.

The Council Tax Reduction Scheme could be used to offset the rise in council tax for eligible low-income households. Alternatively, the regressive elements of the council tax reform could be mitigated by the introduction of a compensation package, albeit with reduced overall additional revenue. Landman Economics modelled a different council tax reform to replace council tax with a 0.7% proportional property tax. This modelling found that a compensation scheme to ensure no-one in the bottom third of the income distribution paid more than they would have under the existing council tax scheme, would still raise 46% of the revenue compared to a situation with no compensation scheme.[165]

Source: IPPR Tax-Benefit Model, Centre for Social Policy Studies.

Source: IPPR Tax-Benefit Model, Centre for Social Policy Studies.

Anticipated wider impacts

Risk of negative impact on:

GDP: Low

Productivity: Low

Labour market participation: Low

Employment rate: Low

Investment levels: Low

There are different views on the form property taxation should take due to housing being a service that’s consumed by the occupier, as well as an asset for homeowners and therefore a form of savings.[166] Property is one of the least mobile tax bases, and therefore behavioural changes will have less of an impact on the revenue raised from an increase in tax rates for council tax.[167] This also means it is deemed to be one of the most viable options for differentiated tax rates to England.[168] Property is also visible and easy to establish, so evasion is difficult.[169]

Economic theory suggests that changes in property taxes are largely or fully passed through to rent and property prices.[170] This would therefore impact the living standards of households, and potentially consumption, inflation and GDP. However, the scale of these impacts is highly uncertain. Regardless of the actual impact, the political context would likely be challenging, especially in light of not implementing proposals to raise council tax and continued concern about the cost of housing. For example, YouGov polling for the Public Insight Monitor in March 2024 reported 36% of all renters were either not managing very well, having some financial difficulties or were in deep financial trouble, as well as 20% of households with a mortgage.[171]

Scenario 3: Reducing the Scottish Income Tax personal allowance (Stage 2)

Purpose

Reducing the Scottish Income Tax personal allowance would raise additional revenue for use in Scotland.

At present, the Scottish Government does not currently have the powers to change the personal allowance, and it would need to request devolved powers to extend the Scottish Income Tax schedule.

The UK Government increased the income tax personal allowance significantly throughout the 2010s, rising by 61% in real terms between 2010-11 and 2019-20.[172] Since the 2021 UK Budget, the personal allowance has been frozen at 2021-22 levels (£12,570). This will remain the case until 2027-28.

There are two major justifications for reducing the personal allowance. Firstly, while increasing the personal allowance has been described as a policy aimed at helping those on the lowest incomes, most of the gains have been seen by better-off households. Lower-income households who do not earn enough to pay income tax do not benefit from the policy by definition, and non-taxpayers account for over a third (34.5%) of the Scottish population.[173] Additionally, two-earner couples (who tend to have higher household incomes) benefit twice over from increases in the personal allowance.[174] The progressivity of the policy only holds if the gains of individual income taxpayers are considered.[175] Therefore, a key purpose of reducing the personal allowance would be to implement a mildly progressive means of raising potentially substantial amounts of revenue.[176]

Secondly, there is political and policy justification for all elements of income tax policy to be fully devolved to the Scottish Government. As of 2025, the Scottish Government has control over decisions for setting income tax bands, rates and thresholds – but not the personal allowance. Often, these rates and bands are set relative to the personal allowance, and the Scottish Government is therefore missing control over a key element of income tax policy.

Delivery and implementation

Administrative feasibility

High

Political desirability

Medium

Policy viability

Medium

The Scottish Government has already demonstrated the administrative feasibility of making decisions over other elements of Scottish Income Tax, meaning there would be low administrative barriers to devolving decisions over the personal allowance to the Scottish Government. There would also, in theory, be a much more administratively simplified system for taxpayers, with all non-savings, non-dividend (NSND) income falling under the same income tax regime rather than the current hybrid system of UK and Scottish Government decisions.

However, despite a general political desire to see further income tax devolution to Scotland, there may be some political and policy hesitancy around introducing any significant changes to the personal allowance. This is due to concerns that any such further income tax devolution would deviate Scotland’s tax regime too much from the rest of the UK and also potentially distort the resulting behavioural impact.

Revenue-raising potential and cost

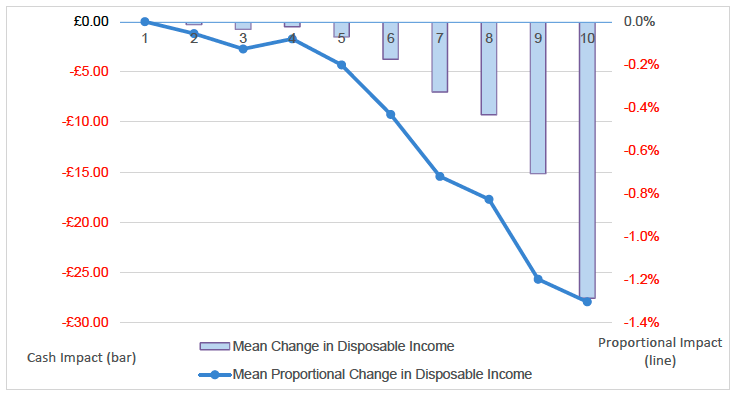

The amount raised from a reduction to the Scottish Income Tax personal allowance in Scotland would depend on the exact reduction applied to the person allowance. We have modelled a scenario to reduce the personal allowance by £5,000 from £12,570 to £7,570. This would reduce the personal allowance to a similar cash level before the personal allowance increases began in 2010. Our modelling found that this personal allowance reduction would raise £2.68bn. The extent of its revenue-raising potential here reflects the relatively significant reduction in the personal allowance we have modelled.

Distributional impact

The proposed reduction to the Scottish Income Tax personal allowance would lead to a much broader tax base across the income distribution. However, the impact would still be considered progressive in cash terms, with our modelling in Figure 4 showing that the greatest cash impact would fall on those in the 8th and 9th income deciles. Indeed, almost all taxpayers in these two deciles are net losers of the policy (97% and 99% respectively). Proportionally, however, the impact of the reform falls most heavily on the middle of the income distribution. In this respect, a significant reduction to the Scottish Income Tax personal allowance would more closely mirror the tax base in countries that generate more tax revenue than the UK. In these countries, median earners make a greater contribution through personal taxation than their UK counterparts.[177]

Source: IPPR Tax-Benefit Model, Centre for Social Policy Studies.

Anticipated wider impacts

Risk of negative impact on:

GDP: Low-Medium

Productivity: Low

Labour market participation: Medium

Employment rate: Medium

Ivestment levels: Low

The reduction in the personal allowance would be, in effect, a tax rise, and whose expected wider impacts would be similar to those discussed above for the reduction in Scottish Income Tax thresholds scenario.

Scenario 4: Expanding Scottish Income Tax to dividends and savings (Stage 2)

Purpose

Expanding the Scottish Income Tax regime to income from savings and dividends would raise additional revenue for use in Scotland.

As of 2025, the Scottish Government does not have the powers to apply Scottish Income Tax to dividends and savings income, so it would need to request devolved powers to extend the Scottish Income Tax schedule.

Within the UK, the tax rates applied to dividend income are lower than those applied to NSND income tax, and these rates are lower still than if Scottish Income Tax for NSND income applied to dividend income. An important purpose of the reform is to ensure taxation of all income at the same rate, regardless of the source of that income.

Income from earnings currently makes up most of income tax revenue in Scotland, but it does have important interactions with the smaller share of income that arises from savings and dividend income, especially amongst higher earners. As such, there would be practical reasons to complete the devolution of Scottish Income Tax to all types of earning. It would be potentially advantageous for the Scottish Government to have decision-making capacity over all taxable income.

Delivery and implementation

Administrative feasibility

High

Political desirability

Medium

Policy viability

Medium

In theory, applying the same Scottish Income Tax schedule to all income would design a simpler tax system, which would be considered politically desirable. However, the system becomes complex for some individuals who currently who do not pay any or very little Scottish Income Tax because their income arises mostly or entirely from dividend and saving income only.[178] As such, there may be political and policy hesitancy around introducing the change as well as the potential distortion the reform could cause between Scotland and the rest of the UK system.

However, more generally there is political will in Scotland to see further tax devolution, and the existing infrastructure to collect revenue from NSND income means there would low administrative costs to devolving dividends income to Scotland.

Revenue-raising potential and cost

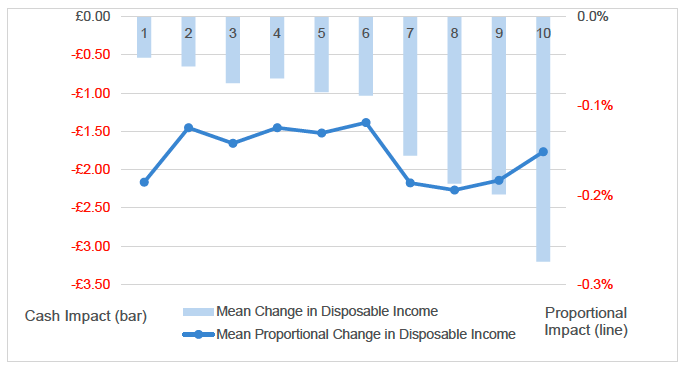

Estimates of the revenue-raising potential of devolving tax powers over savings and dividends income have not been made before. Nevertheless, it has been suggested that the expected revenue raised would be modest.[179] In contrast, however, by setting the rates and bands for income from savings and dividends to be the same as Scottish Income Tax for non-savings and non-dividend income, our modelling has found that this would raise £81m per year. This is only the increase in Scottish revenues, and does not reflect the wider budgetary impact of this policy through BGA and the net position.

Distributional impact

It is well established that business income (either from self-employment or owning and running a company) is much more important for higher income taxpayers. Business income in the UK accounts for around 21% of the income of the top 1%, compared to 9% of those below the top 1%.[180] As such, taxing income from these sources would be a progressive means of raising revenue.

Our modelling in Figure 5 shows that both the cash and proportional impact of this reform falls almost entirely upon those in the 10th income decile.

However, the number of people impacted by the reform is modest. Only 16% of people within the upper income decile would be impacted by this modelled policy change, suggesting that even amongst the highest earners a majority of people still derive their income through earnings.

Source: IPPR Tax-Benefit Model, Centre for Social Policy Studies.

Anticipated wider impacts

Risk of negative impact on:

GDP: Low-Medium

Productivity: Medium

Labour market participation: Low

Employment rate: Low

Investment levels: Uncertain

There is a degree of uncertainty around how any changes to taxing dividends would impact on employment, productivity and investment. Some research has suggested that dividends taxes constrain the efficiency of investment decisions, with the impact felt more sharply by those with limited internal funds.[181] However, evidence from France, where there was a steep increase in the dividends tax rate in 2013, suggests that the tax reform led to increased levels of cash holding which improved the allocation of capital, and led to no discernible reduction in investment even among equity-dependent firms.[182]

Taxing all income at the same rate would eliminate one of the more common forms of tax avoidance (namely, higher earners converting income into dividends) within Scotland. As the Poverty and Inequality Commission has outlined, there still remain additional complexities to consider around how the Scottish dividends tax system would operate alongside the system for the rest of the UK. A divergent, and higher, income tax structure for Scotland could create stronger incentives for individuals to arrange incomes in a way that reduces exposure to the Scottish Income Tax rates and bands and lead to potentially high revenue loss in Scotland as a result of behavioural changes and cross-border effects.[183]

Scenario 5: Increasing National Insurance contribution rates (Stage 3)

Purpose

Raising National Insurance contribution (NICs) rates would generate additional revenue through tax take from both employees and employers. As of 2025, NICs are charged at 8% on earnings for employees, an additional 2% on employee earnings above the Upper Earnings Limit (over £967 a week, or £4,189 a month) and 13.8% for employers. The 2024 UK Budget announced a rise in the employer NICs rate to 15%.

Compared to what is raised in the UK, other countries in Europe raise more revenue through social security contributions (somewhat equivalent to NICs although with a stronger contributary tie than is the case in the UK). This is especially the case for those social security contributions levied on employers.[184] Therefore, there is arguably scope to increase rates in Scotland to raise additional revenue, especially as NICs is the second largest source of government revenue in the UK.

As Scotland has powers over income tax, there is a logic to extending powers to NICs. NICs now function similarly to income tax, and Scottish Government control would therefore allow for better alignment and coordination between these two taxes. Scotland, however, does not currently have powers to change NICs rates and, as such, this option would require further devolution.

Delivery and implementation

Administrative feasibility

Medium

Political desirability

Medium

Policy viability

Medium

It has also been argued that it is optimal to devolve taxes which are less mobile. As NICs are, essentially, a tax on labour, this type of taxation is on the whole less mobile than capital and so would be a sound choice for devolution from an administrative and political desirability perspective. In addition, as the collection of NICs work broadly in the same manner as collection of income tax, there should be limited administrative issues of Revenue Scotland administering the NICs system.

Revenue-raising potential and cost

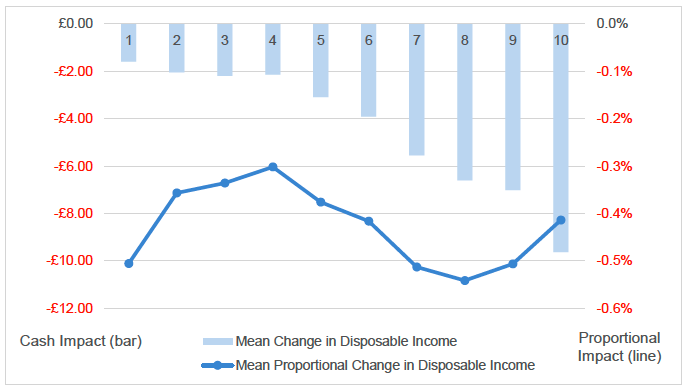

The amount raised from a change to NICs rates in Scotland would depend on the rate set and behavioural changes. We have modelled a scenario to raise the main employee rate, employee rate above UEL and employer rate all by 1 percentage point. This would raise £1.38bn per year. In our modelling we have accounted for the change to employers’ rates announced in the 2024 UK Budget.

Larger increases in these NICs rates could generate more additional revenue, but with potentially diminishing returns due to behavioural changes on labour market participation and recruitment.

In addition, it is worth noting that Scotland's relative lack of very high earners does not undercut Scottish NICs revenue in the same way as income tax revenue.[185]

Distributional impact

The increases to employer NICs announced in the 2024 UK Budget are likely to have a greater impact on the labour costs of those at the lower end of the income distribution, as IFS analysis has suggested.[186] Other research has also pointed out that it would be labour-intensive firms and those with a high number of lower-paid employees that would be affected the most.[187]

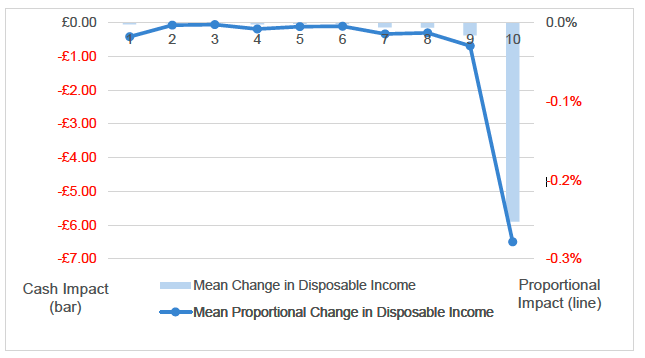

Our modelling in Figure 6 shows that increases across all rates of NICs would actually have a progressive impact in both cash and proportional terms. At the lower end of the income distribution, the increasing cash impact is relatively incremental, but there is an especially significant jump in the impact at the upper end of the income distribution. This is particularly the case in the difference in impact between the 9th and 10th income deciles, where the impact almost doubles from -£11.37 to -£21.44.

Source: IPPR Tax-Benefit Model, Centre for Social Policy Studies.

Anticipated wider impacts

Risk of negative impact on:

GDP: Medium

Productivity: Medium

Labour market participation: Medium

Employment rate: Medium

Investment levels: Low-Medium

In the short-term, it has been suggested that increasing NICs would not immediately affect wages or employment rates, as firms face challenges around lowering wages as wages are often resistant to immediate policy changes.[188] However, in the longer term, workers could face wage cuts or job losses, but the extent of this would depend upon specific business circumstances.[189] NICs increases are more likely to affect businesses based on employment size, not profitability, meaning that those firms with labour-intensive or lower-paid business models would be affected the most, leading to a drop in productivity.[190]

Research in Finland shows that, in response to NICs-style increases in social security contributions on employers, firms responded by altering their labour input choices by substituting low-skilled workers with high-skilled ones. This suggests that, even if wage effects are limited, there may be reduced employment opportunities and a knock-on effect on investment levels.[191]

Scenario 6: Increasing and broadening the VAT base (Stage 3)

Purpose

Increasing and broadening the VAT base would raise additional revenue through levying a higher rate of consumption tax on a wider range of goods and services. VAT is the third largest source of government revenue in the UK and is one of the most stable revenue sources relative to the economy cycle.[192]

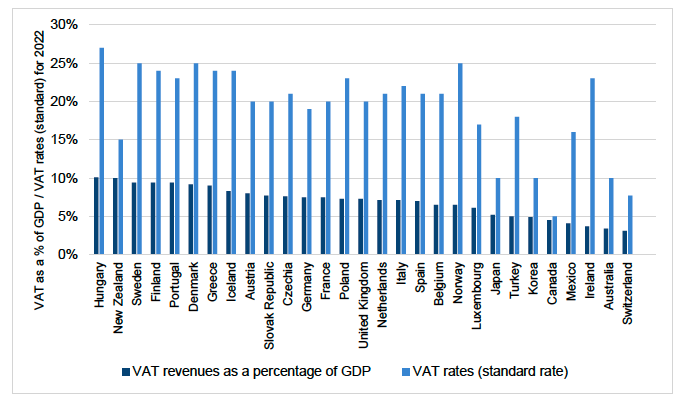

Other countries raise more revenue through broader tax bases or higher rates.[193] Therefore, there is arguably scope to increase rates in Scotland to raise additional revenue.

Source: OECD Consumption Tax Trends and Revenue Statistics 2024.

As of 2025, VAT is charged at 20% (with a 5% reduced rate and zero-rate). Scotland does not currently have powers to change VAT rates and, as such, this option would require further devolution.

Delivery and implementation

Administrative feasibility

Low

Political desirability

Low

Policy viability

Medium

VAT is viewed as both a tax on consumers and businesses and as being regressive. Therefore, an increase in VAT rates and increasing and broadening the way VAT is applied could be politically difficult, especially in the current economic context. In addition, the current standard rate of VAT is at an historic high, and above the consumption tax rate of many EU countries.[194] However, the reduced rate was not raised in 2011 and remains at just 5%, and there may be more political viability in raising this rate.

Further devolution would be needed to allow for VAT to be used as a revenue-raising option in Scotland. The Scotland Act 2016 allowed for the assignment of VAT to the Scottish Government. However, experts giving evidence at the Scottish Parliament’s Finance and Public Administration Committee in November 2023 raised concerns about the quality of data available and that a decade of work on assignment had failed to identify a methodology accurate enough to measure Scottish VAT receipts for assignment.[195] This complexity limits the feasibility of devolution of VAT, although both the Scottish and UK governments recommitted their intention to agree and implement a methodology in the 2023 updated Scottish Government Fiscal Framework agreement.[196]

There would also be significant administrative barriers because Scotland is, and is likely to remain, part of a highly integrated UK single market. This was also discussed during the Scottish Parliament’s Finance and Public Administration Committee meeting in November 2023, where VAT was described as a very poor candidate for devolution (or indeed assignment) because different VAT rates in Scotland would add extra costs for retailers and create opportunities for competition and avoidance.[197]

Revenue-raising potential and cost

The amount raised from increasing or broadening the VAT base in Scotland would depend on what rates are applied to certain goods, the rate set and behavioural changes. We have modelled a scenario to increase the standard and reduced rate of VAT by one percentage point. We have also broadened the VAT base by scrapping the zero-rate and applying the new reduced rate to all currently zero-rated goods. This would raise £891m per year.

| Rates | Current rate | New rate |

|---|---|---|

| Standard rate | 20% | 21% |

| Reduced rate | 5% | 6% |

| Zero-rate | 0% | 6% |

Distributional impact

Increasing and broadening of the VAT base would further contribute to the regressive nature of VAT (and other indirect taxes) in Scotland.[198] However, this can be offset by improving the progressivity of other taxes and transfers in the system to compensate. Economists argue that not every tax needs to be progressive, it is the progressivity of the overall system that matters.[199] As IFS research has shown, in the UK cash transfers play a big role in compensating for the impact of indirect taxes on lower-income groups.[200] A MIG scheme could further contribute to this picture.

Previous analysis has shown that applying VAT to food or other basic items, for example, would reduce the incomes of the rich by more than the poor, raising revenues that could be used to compensate the latter and generate surplus revenue.[201] It has also been argued that raising VAT rates or removing exemptions on merit goods could also improve the progressivity of the tax as currently levied, as it is higher-income groups who receive this tax relief to a far greater extent.

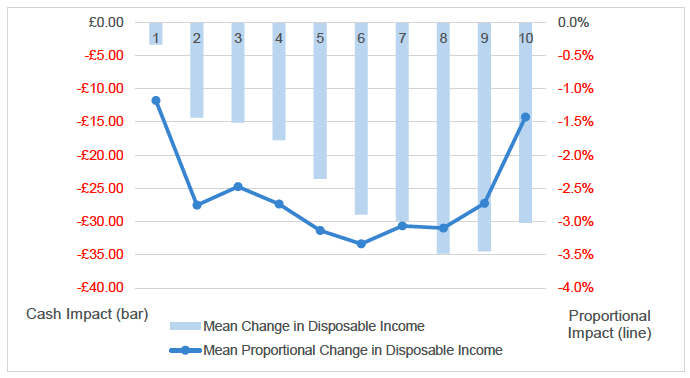

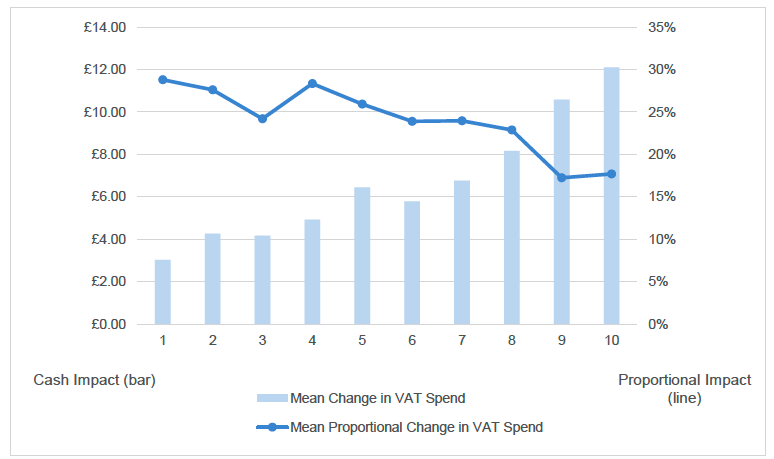

Our modelling in Figure 8 shows the regressive nature of increasing and broadening VAT. Broadly speaking, the higher up the income distribution, the less impact the VAT changes have on increased spending on VAT. The impact would be felt most by the bottom five income deciles, with consumers in these deciles seeing an increase in household spending on VAT by over a quarter. The proportional impact of the policy would be felt the least by the 9th and 10th income deciles, at 17% and 18% respectively.

Source: IPPR Tax-Benefit Model, Centre for Social Policy Studies.

Anticipated wider impacts

Risk of negative impact on:

GDP: Uncertain

Productivity: Uncertain

Labour market participation: Uncertain

Employment rate: Uncertain

Investment levels: Low

VAT is considered to be a well-designed consumption tax as it is paid by consumers, and not typically by businesses when they buy inputs into their production processes – thereby helping ensure production efficiency is achieved.[202] Furthermore, as VAT is charged across a broad range of products and services, the sustainability of this revenue option is reasonably high. However, there are some key considerations, including impact on inflation and cross-border flows.

Increases in consumption taxes are commonly passed on to consumers.[203] Therefore, any increase in VAT would lead to increased prices. Depending on the economic environment at the time of the change, increased prices could cause concerns over inflation levels, impact on consumption and, by extension, GDP. While an increase in VAT rates in Scotland would be likely to have an impact on Scottish inflation, consumption levels and GDP, it is unlikely to have significant impacts on rates across the rest of the UK.

There may also be some reduction in business activity if businesses absorb part of any increase, potentially impacting GDP, investment and employment rates. For instance, in 2010 when VAT was raised from 17.5% to 20%, the OBR predicted that company profits as a share of GDP would be 0.4 percentage points lower in 2014 than in the pre-Budget forecast due to businesses absorbing part of the rise through lower profit margins.[204]

However, the overall impact on GDP, productivity and employment is uncertain. An increase in VAT would have little impact on exports because VAT is not charged on goods exported and consumed outside of the UK. While there would most likely be a negative impact on consumption due to higher prices, the impact on employment depends on the type of goods taxed. Differentiated VAT rates can be used to support work incentives, if higher rates are applied to goods that are complementary to leisure time, such as restaurant meals, than those complementary to long work hours such as ready meals.[205] This is suggested to be a way of partially offsetting disincentives to work that a redistributive tax system creates. The practical significance of this argument is unclear, but it may have relevance for tax applied to childcare services or travel at peak times for example.

The geographical location of Scotland to the rest of the UK could also limit revenue raised. VAT is charged based on the location of the consumer, not the business. However, if consumers are easily able to shift their consumption into the rest of the UK, for example travelling across the border to shop, this would reduce tax take. This is more likely the greater the differentiation in rates between England and Scotland.[206]

Avoidance and evasion could also reduce tax take. The ‘VAT gap’ has a positive association with the number of VAT rates, size of the shadow economy and the level of VAT rates, amongst some other factors.[207] The additional complexity of dealing with two VAT systems for businesses operating in Scotland and the rest of the UK would likely increase the ‘VAT gap’.[208] One possible way to mitigate this would be move to a lower, single VAT rate that means there would be fewer opportunities for VAT evasion. The Mirrlees Review found that the cost-neutral implementation of a lower, single VAT rate would raise revenue through reduced VAT evasions.[209]

The amount raised by increasing or broadening the rate of VAT would also depend on the elasticity of prices for the type of goods or services it is levied on. The reduced or zero-rate could arguably be better options for raising additional VAT revenue due to the essential nature of these goods which makes consumption less elastic to potential price changes.

An EU-wide study estimated that a one percentage point increase in VAT leads to roughly a 1% reduction in the level of aggregate consumption in the short run, and a larger reduction in the long run.[210] However, VAT elasticity will depend on broader implications of tax policy, and it could be lower in Scotland. For instance, the VAT revenue elasticity is lower for Ireland than estimates for the UK, New Zealand and Australia, possibly reflecting the greater progressivity of the Irish income tax system compared to other OECD countries.[211] Much of the change also depends on whether the VAT change is unexpected or not. If a rise is expected, then consumers may bring consumption forward to benefit from a lower rate.[212]

Scenario 7: Increasing excise duties (Stage 3)

Purpose

An increase in excise duties would increase the tax levied on specific goods. This scenario focuses on increases to alcohol, fuel and tobacco duties. Duties paid on fuel and alcohol have been frozen since 2011, meaning that there is potentially headroom for a notable increase in duty rates.

Excise duties can be intended to change behaviour and reduce consumption of goods considered to have negative consequences, such as a harmful impact on health or the environment.[213] Alternatively, they can be implemented to raise additional tax revenue from goods where price increases have limited impact on overall demand.[214] Both of these characteristics are true for fuel, alcohol and tobacco and we have selected these goods on the assumption that there is still additional headroom to charge more tax on these products before decreases in consumption outweigh the additional tax revenue that would be generated.

Scotland would require further devolved powers to change the excise duty regime, which is currently set by the UK Government and collected by HMRC.

Delivery and implementation

Administrative feasibility

Low

Political desirability

Medium

Policy viability

Medium

Charging a higher excise duty rate in Scotland would need devolved powers and the establishment of new collection mechanisms in Scotland. This would bring administrative costs for both the Scottish Government and businesses that operate in both Scotland and the rest of the UK, who would need to interact with two different excise duty systems. An alternative would be to make excise duties an assigned tax, but this has proved difficult for VAT and may not be feasible.

Despite freezes to alcohol and fuel duty since 2011, the UK currently raises a relatively high amount of revenue from excise duties compared to other developed economies, which could limit the political desirability for increasing duties.[215] Policy viability for this option to fund a MIG scheme might also be limited as the rationale for excise duties can be tied to public health concerns and the associated demands on public spending.[216]

Revenue-raising potential and cost

The amount raised from a change to excise duties would depend on the rate set. In 2023-24, excise duties on fuel, tobacco, alcohol and vehicles together contributed 6.7% of the total Scottish tax take.[217] We have modelled a 10% increase in fuel, alcohol and tobacco duties.[218] This would generate an additional £189m of revenue from excise duties per year.

Distributional impact

Excise duties are considered to be regressive and to disproportionately affect those on lower incomes. In Scotland, the bottom quintile already pay 31% of their income in indirect taxes, contributing to those group having the highest tax burden as a proportion of the population.[219] This concern can, however, be mitigated by the progressivity of the broader tax and benefit system. Moreover, there is some evidence that the price responsiveness to excise duty increases is larger amongst lower income groups.[220]

Our modelling in Figure 9 highlights the regressive nature of the policy, with all income deciles experiencing a 10% proportional increase in spending as a result of additional excise duties being levied. In cash terms, increasing excise duties has a particularly significant impact on the upper half of the income distribution. In part this reflects that alcohol consumption and car ownership (and therefore the consumption of fuel) are more common amongst higher income households, although the reverse is true for tobacco consumption.[221]

Source: IPPR Tax-Benefit Model, Centre for Social Policy Studies.

Anticipated wider impact

Risk of negative impact on:

GDP: Low-Medium

Productivity: Low

Labour market participation: Uncertain

Employment rate: Uncertain

Investment levels: Uncertain

While excise duties are a tax paid by the seller of the goods, largely it is assumed that the cost of the duty is passed on to consumers. Therefore, excise duties are considered to be an indirect tax on consumption. Economic theory suggests taxes should be higher on goods with inelastic demand to minimise the amount that taxes alter consumer behaviour and reduce tax take.[222] Fuel is highly price inelastic,[223] whereas alcohol and tobacco are known to be more elastic but consumption is still fairly resilient to price changes.[224] In light of this, an increase in excise duties would be expected to have a minimal effect on consumption and GDP, but would contribute to price inflation.

Economic theory also argues that excise duties are inefficient because they do not adequately price in and target sub-optimal behaviours, for example, everyone consuming alcohol pays the duty, not just heavy drinkers.[225] However, this is of less concern if the intention is to raise additional revenue.

The key consideration in the Scottish context would be the likelihood of behavioural change if Scotland were to have higher excise duties compared to the rest of the UK. The effect of differentials in excise duties between neighbouring economies is complex and highly dependent on the specific circumstances.[226] The geography of Scotland means that cross-border flows of fuel consumption are less likely, but consumers would be more likely to travel further for bulk purchases of alcohol and tobacco, or for big ticket items.[227] While the exact relationship between price and willingness to trade is unknown, approximately 40% of the Scottish population live within a 2-3 hour drive of the border with England.[228] However, initial evidence of the impact of minimum alcohol pricing in Scotland, which has led to higher prices charged for alcohol in Scotland than England, suggests that cross-border trade has only happened on a small scale, likely by the small population living near the border.[229]

How far do these scenarios contribute towards funding a MIG?

The scenarios we have modelled are just some of the ways the taxes we have explored could be reformed. We have also not explored all of the taxes that could be available to the Scottish Government across different levels of powers. However, Table 17 shows that the scenarios we have modelled suggest that securing additional revenue from Scottish Income Tax, council tax, NICs, VAT and excise duties would make a significant contribution to the short, medium and long term revenue-raising targets for a MIG.

| Stages | Scenarios included | Revenue raised from modelled scenarios | Lower estimate of revenue-raising target | Scenario % of lower estimate | Upper estimate of revenue-raising target | Scenario % of upper estimate |

|---|---|---|---|---|---|---|

| 1 | 1 and 2 | £0.84bn | £0.3bn | 278% | £1bn | 84% |

| 2 | 1, 2, 3 and 4 | £3.75bn | £1bn | 375% | £2.5bn | 150% |

| 3 | 1, 2, 3, 4, 5, 6 and 7 | £6.39bn | £2.5bn | 256% | £10bn | 64% |

In the short term, implementing our modelled reforms to Scottish Income Tax and council tax, which the Scottish Government already has the powers to do, could generate an additional £835m per year in revenue.[230] While this does not account for behavioural changes, these static estimates suggest that if all this additional revenue were directed towards a MIG, it would raise 84% of the £1bn upper estimate for a MIG’s initial stage.

In the medium term, if the Scottish Government were to complete Scottish Income Tax devolution by securing powers over the personal allowance and were able to apply the Scottish Income Tax regime to savings and dividends income, it could generate around £3.75bn per year in additional revenue from expanded Scottish Income Tax powers combined with Stage 1 reforms.[231] Although this does not take into account potential behavioural changes, these static estimates suggest that if all of this additional revenue was directed towards a MIG it would vastly exceed the £2.5bn upper estimate for the second, intermediate phase of a MIG. Indeed, the additional revenue from the reduced Scottish Income Tax personal allowance scenario (£2.68bn) would alone meet the stage 2 upper estimate.

In the longer term, if the Scottish Government were able to secure powers over a wider range of taxes than is currently the case, £6.39bn per year could be generated from all of the scenarios we have modelled.[232] Although this does not take into account potential behavioural changes, these static estimates suggest that if all of this additional revenue was directed towards a MIG, it would raise 64% of the £10bn upper estimate for a MIG’s third and final stage.

Contact

Email: MIGsecretariat@gov.scot