Modelling the economic impact of US tariffs on Scotland and the rest of the world: technical paper

Technical paper on the use of structural gravity modelling which sets out economic modelling on the potential impact of US Tariffs on Scotland and the rest of the world.

Results

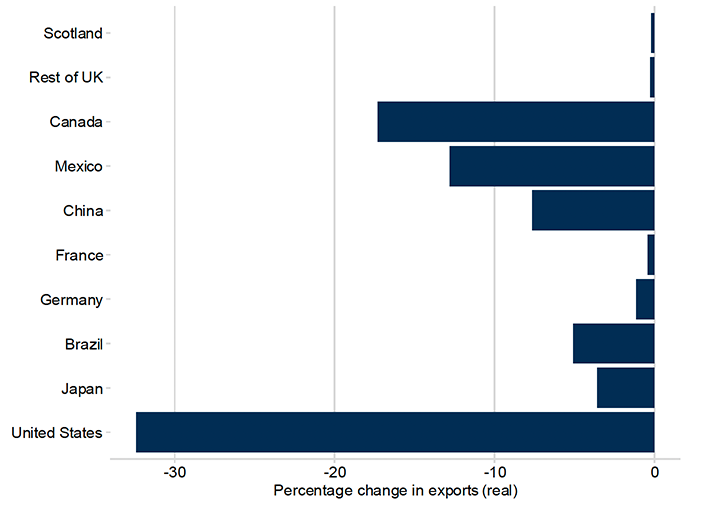

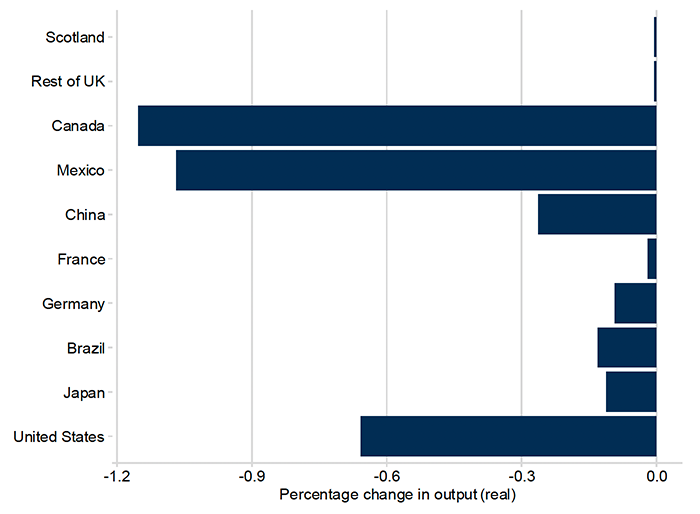

The model tells us how much larger or smaller trade flows would be in the long run, in the scenario of interest compared to the baseline trade flows in the input data. The results presented here are summarised from the raw outputs, showing how exports and output could be affected for Scotland, the rest of the UK, and other selected countries.

The model finds that, in the long run, total global trade could be 7% lower and global output could be 0.3% lower than if the tariff increases were not applied. Scotland and the rest of the UK are relatively less exposed than many other countries. Directly targeted countries (Canada, Mexico, China) tend to be hardest hit. The USA is also one of the worst affected countries. Figures 1 and 2 include retaliation by China and Canada, but even without this retaliation, the USA’s economy is damaged even by its own tariffs on others. This is consistent with economic theory: while tariffs can protect domestic industries, they can also disrupt supply chains and increase prices.

These results (and those below) are in real terms, meaning that price changes have been taken into account. Note that we present percentage impacts, meaning that the size of the bar doesn’t show the absolute change in value.

Of the countries not directly targeted, some fare worse than others – the UK is less affected than Germany, Brazil, and Japan. These results don’t include the effect of the UK–US Economic Prosperity Deal, which might be expected to reduce the impact further, or even result in positive results for the UK, as the UK may be able to benefit from reduced competition from other countries facing higher tariffs.

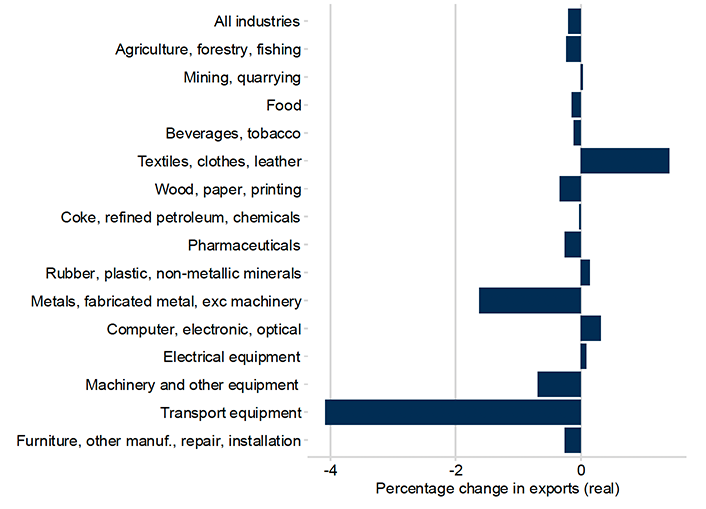

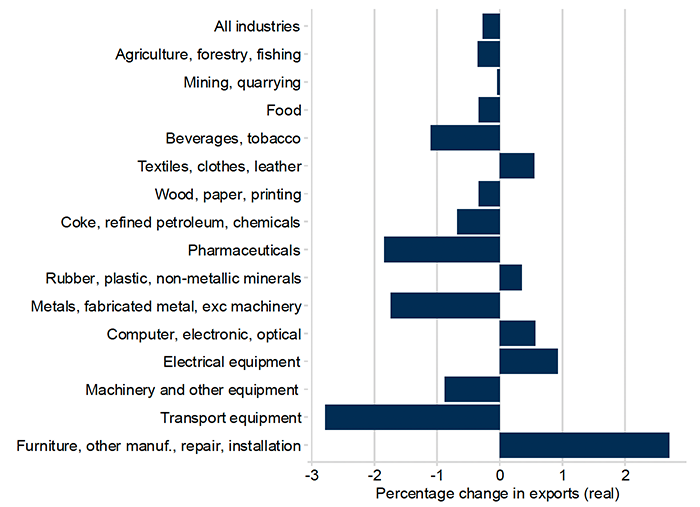

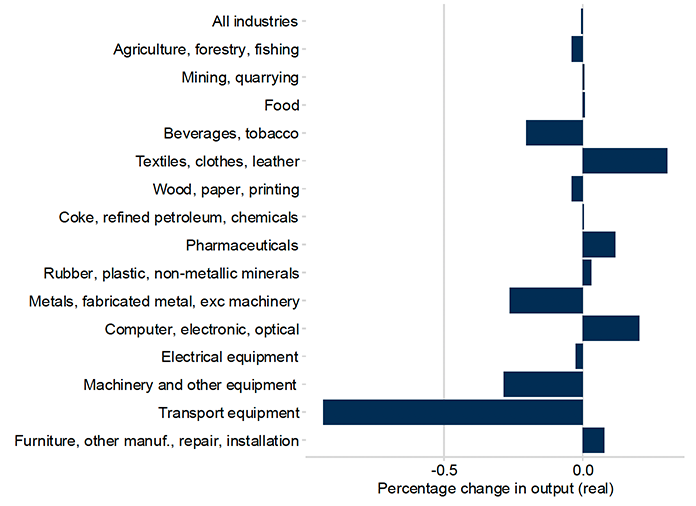

As shown in Figures 1 and 2, the total impact on Scotland’s and the rest of the UK’s exports and output is expected to be minimal. However, this impact can vary by sector, as shown in Figures 3 to 6.

Some results may be overstated. In particular, the transport equipment result comes from the US tariff on cars and car parts, but Scotland does not export many cars and car parts, instead exporting other transport equipment. However, in constructing the scenarios, due to data availability, the aggregation is based on UK trade flows, and the UK does export a significant value of cars to the USA.

The sectoral distribution of impacts in Scotland compared to the rest of the UK will depend on several factors, including revealed comparative advantage in each sector, and exposure to trade with the US. On the whole, the impacts on rest-of-UK exports are slightly larger than the impacts on Scottish exports, possibly indicating greater exposure to the US in terms of total exports.

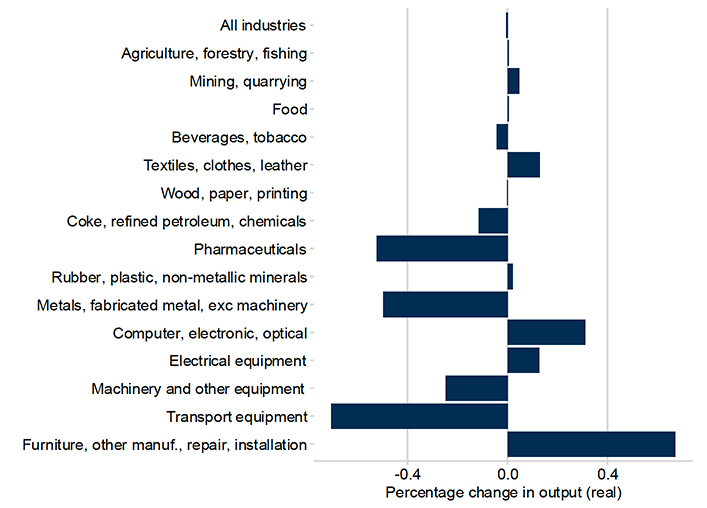

Output includes the total production in a sector: that is, exports plus domestic consumption. As such, it tends to show similar patterns to the export changes but on a smaller scale: all impacts here are less than 1%, and if we exclude transport equipment for the reasons given above, all impacts are well below 0.5%.

The impact on rest-of-UK output shows that directly targeted industries (pharmaceuticals, metals, and transport equipment) tend to be hardest hit, but there may be opportunities in “furniture, other manufacturing, repair and installation”.

Contact

Email: economic.statistics@gov.scot