A Deposit Return Scheme for Scotland: Strategic Environmental Assessment Addendum

This document is a revised SEA Addendum setting out the environmental impacts of DRS under the new go-live date. On 14 December 2021, the Minister for Green Skills, Circular Economy and Biodiversity announced that the Scottish Government would seek to amend the full implementation date for DRS to 16 August 2023.

A Deposit Return Scheme for Scotland: Strategic Environmental Assessment Addendum

Background

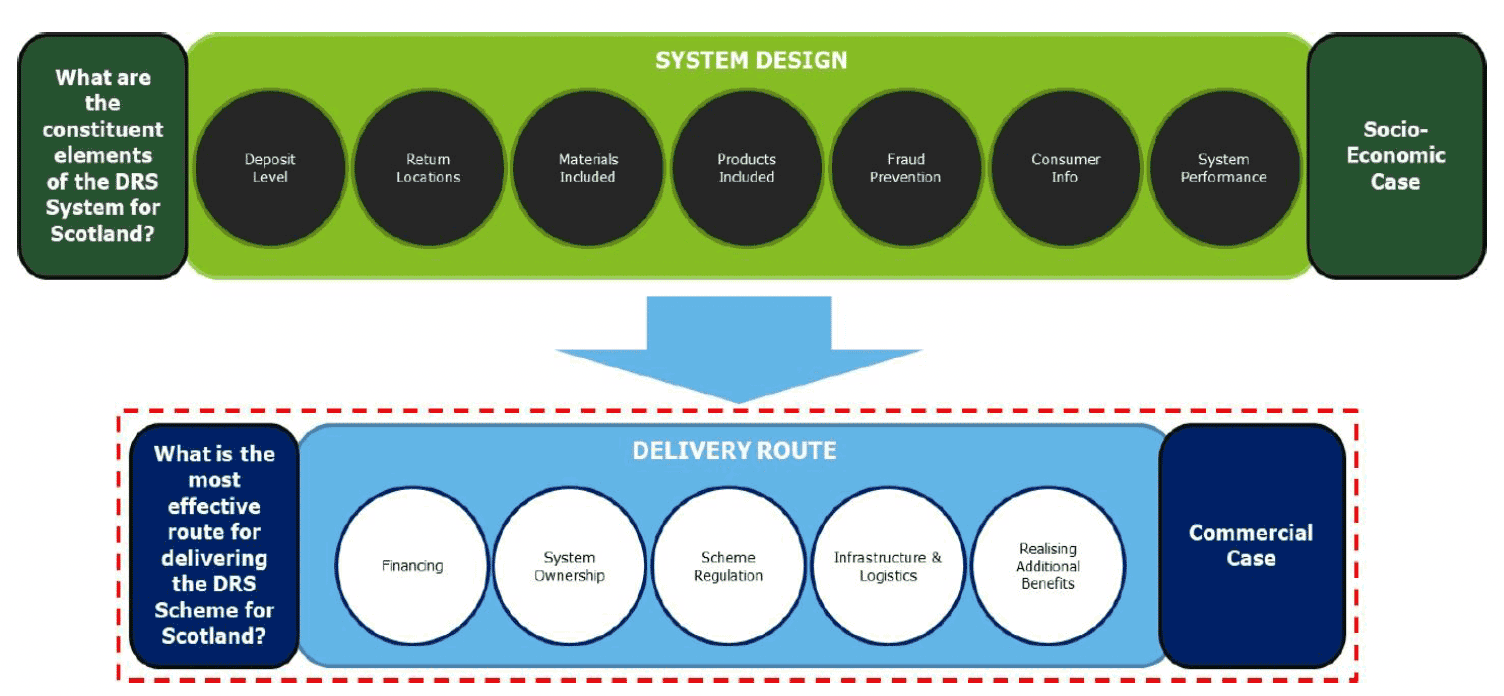

In the Environmental Report,[1] developed as part of the Strategic Environmental Assessment for Scotland's Deposit Return Scheme (DRS), four 'example deposit return schemes' were presented.

These were selected to illustrate different possible configurations of the 12 components which make up a functioning DRS:

Extensive modelling was undertaken to determine the likely performance and environmental impacts of these example systems, and the results were presented for public consultation in the Environmental Report.

Following extensive public consultation, stakeholder engagement and further evidence- gathering, the preferred scheme design for Scotland's DRS was announced by the Scottish Government on 8 May 2019.

In December 2019, the Scottish Parliament's Environment, Climate Change and Land Reform Committee requested an update to the original Environmental Report, detailing the characteristics, operational performance, and environmental impacts of the planned DRS for Scotland. That request was addressed with the publication of the Strategic Environmental Assessment (SEA) Addendum, published alongside the DRS Regulations on 16 March 2020.[2]

On 17 November 2021, the Minister for Green Skills, Circular Economy and Biodiversity announced that the Scottish Government would seek to amend the full implementation date for DRS from 1 July 2022 to 16 August 2023. This revised SEA Addendum sets out the environmental impacts of DRS under the new go-live date.

Comparison of Key Scheme Characteristics

The Scottish DRS will be a national ‘return-to-retail’ scheme for single-use drinks containers made of PET, steel, aluminium or glass, with a deposit of 20p per container.

Cartons, cups and HDPE are not included (for more information, see Section 5.1 of the Post Adoption Statement).[3]

Table 1 compares the key characteristics of Scotland's DRS with those of the example systems presented in the Environmental Report. Scotland's DRS is most similar to Example 3 but features a higher 20p deposit.

| Scheme | Return Point | Materials of drink containers collected | Deposit level | Capture rate | Means of collection |

|---|---|---|---|---|---|

| Example 1 | Dedicated points | 1. PET 2. Steel and aluminium 3. Glass |

20p | 60% | 1,058 automated deposit return points placed in towns with a population of at least 1,000. |

| Example 2 | Dedicated points and some shops | 1. PET 2. Steel and aluminium 3. Glass 4. HDPE 5. Drink cartons 6. Single-use paper-based cups |

20p | 70% | 2,009 automated deposit return points placed in, or within a set distance of, any shop selling drinks in containers. |

| Example 3 | Any place of purchase | 1. PET 2. Steel and aluminium 3. Glass |

10p | 80% | Any retailer selling drinks in an in-scope disposable container to operate a (automated or manual) return point for all DRS containers. |

| Example 4 | Any place of purchase | 1. PET 2. Steel and aluminium 3. Glass 4. HDPE 5. Drink cartons 6. Single-use paper-based cups |

10p | 80% | Any retailer selling drinks in an in-scope disposable container to operate a (automated or manual) return point for all DRS containers. |

| Scottish DRS | Any place of purchase | 1. PET 2. Steel and aluminium 3. Glass |

20p | 90% | Any retailer selling drinks in an in-scope disposable container to operate a (automated or manual) return point for all DRS containers. |

Comparison of Scheme Performance and Environmental Impacts

Scotland's DRS has been designed to achieve higher recycling performance outcomes for target materials (PET, steel and aluminium, and glass) compared to the four example schemes (see Table 2).

This higher performance is driven by a combination of features:

- National return-to-retail coverage is designed to maximise accessibility and return convenience across Scotland;

- The 20p deposit provides a stronger incentive for consumer participation;

- The running costs of the scheme will be funded by producers – this will incentivise them to maximise scheme performance and minimise instances of fraud;

- The target capture rate of 90% will be mandated in the Regulations and it will be the producers' legal responsibility to meet it.

As a result, Scotland's DRS is expected to support greater levels of recycling, and greater carbon savings overall, compared to example schemes 1, 2 or 3.

It is also expected to outperform example scheme 4 for materials targeted under both schemes, but achieve a slightly lower overall recycling tonnage and carbon benefit due to the inclusion, under example scheme 4, of HDPE drink containers, drinks cartons and single-use paper cups. The Scottish Government has committed to reviewing the scope of the scheme in due course. If that review were to result in the inclusion of additional materials, it can reasonably be assumed that further environmental benefits would be realised.

Based on the principle that the more material a scheme captures, the greater its environmental impact, Scotland's DRS, with its 90% capture rate target, is expected to deliver enhanced environmental impact compared to the other example schemes (for target material). The DRS Regulations set out the statutory collection rates which producers must meet; this is set at 80% for 2024 and 90% for each subsequent year.

This revised SEA Addendum reflects the following changes from the SEA Addendum published on 16 March 2020; otherwise the assumptions are unchanged from that document:

- The first full calendar year of operation of the scheme is now set at 2024;

- A two-year ramp-up for scheme collection targets is modelled in line with the previous paragraph, compared to the three-year ramp-up in the original;

- Revised Scottish population estimates have been included.

The final option will save an estimated 3,918 ktCO2eq between 2024 and 2049[4] and, based on extensive stakeholder engagement, represents an optimum environmental outcome taking account of technical practicalities in establishing and operating a successful scheme.

| Business As Usual (BAU) | Example 1 | Example 2 | Example 3 | Example 4 | Scotland's DRS Final scheme | |||

|---|---|---|---|---|---|---|---|---|

| Take back to dedicated drop-off points | Take back to dedicated drop-off points and some shops (with cartons and cups) | Take back to any place of purchase | Take back to any place of purchase (with cartons and cups) | |||||

| (2018-2043) | (2018-2043) | (2018-2043) | (2018-2043) | (2018-2043) | (2024 – 2049) | |||

| Recycle Rate | Recycle Rate | Recycle Rate | Recycle Rate | Recycle Rate | Recycle Rate | Increased recycling vs BAU (kt) | Carbon savings vs BAU (ktCO2eq) | |

| Glass drink container | 63% | 84% | 88% | 91% | 91% | 96% | 1,320 | 1,243 |

| Steel drink container | 46% | 77% | 82% | 87% | 87% | 95% | 40 | 72 |

| Aluminium drink container | 48% | 78% | 83% | 88% | 88% | 95% | 184 | 1,841 |

| PET drink container | 50% | 79% | 84% | 88% | 88% | 95% | 355 | 761 |

| HDPE drink container | 53% | 53% | 84% | 53% | 89% | 53% | - | - |

| Drink cartons | 38% | 38% | 80% | 38% | 86% | 38% | - | - |

| Single-use paper cups | 1% | 1% | 67% | 1% | 77% | 1% | - | - |

| Total | 57% | 78% | 86% | 84% | 90% | 88% | 1,899 | 3,918 |

It should be noted that the figures in the above table do not take into consideration other anticipated interventions to deliver a more circular economy in Scotland.

Contact

Email: JOHN.FERGUSON@GOV.SCOT