Scottish Local Government Finance Statistics 2022-23

Annual publication providing a comprehensive overview of financial activity of Scottish local authorities in 2022-23 based on authorities' audited accounts (where available).

This document is part of a collection

4. Reserves and Fixed Assets

4.1 Reserves

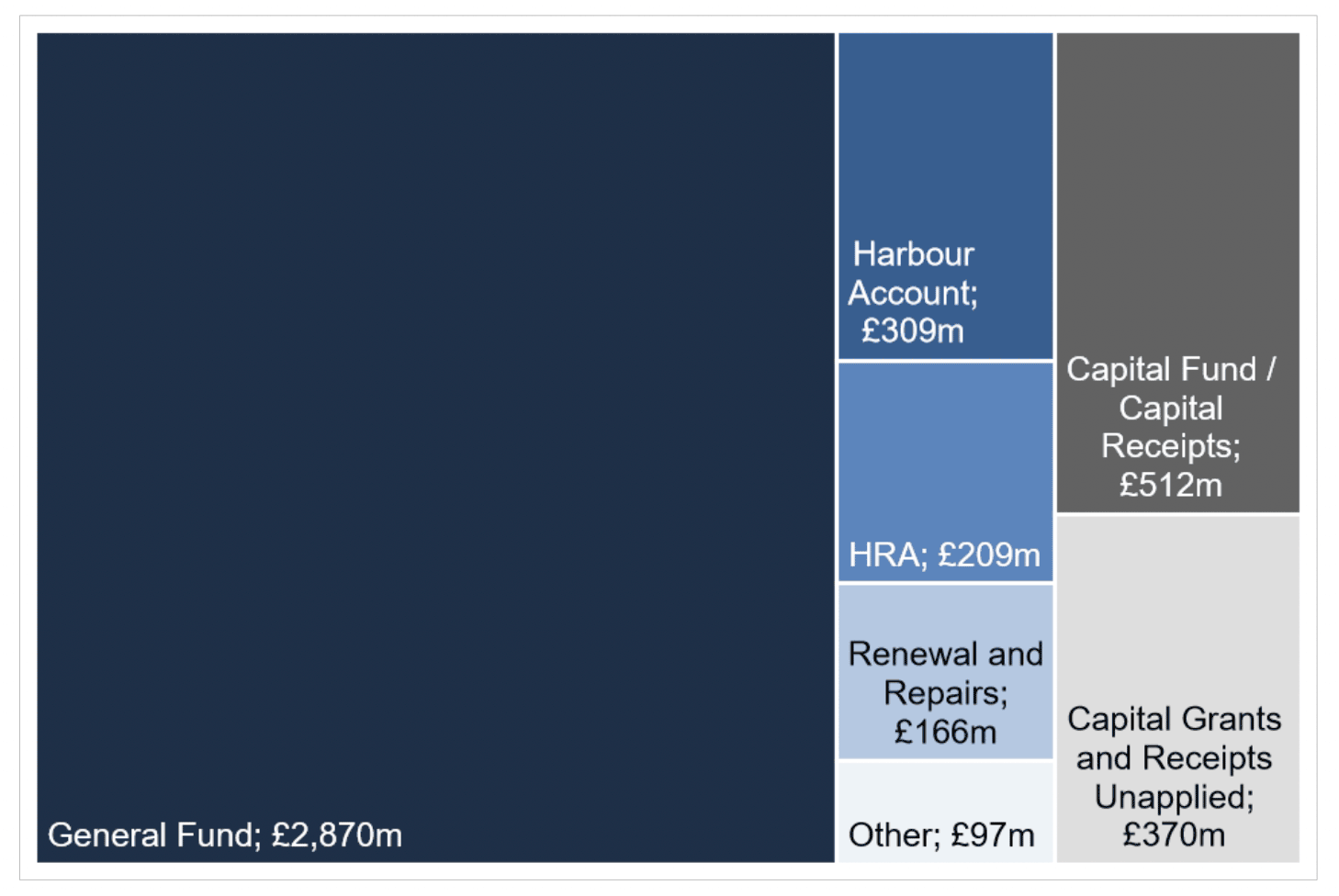

Usable reserves reflect a local authority’s accumulation of surplus income that can be used to finance future revenue or capital expenditure on services. Chart 4.1 shows the total usable reserves at 31 March 2023, by fund.

Please note that 'Other' revenue reserves includes the Insurance Fund.

Source: LFR 23

The General Fund is the principle usable revenue reserve of the local authority. Any deficit in a local authority’s revenue accounts is met from their General Fund, and any surplus is added to the General Fund reserve. The General Fund therefore reflects a local authority’s accumulation of surplus income that can be used to finance future revenue expenditure on services or to fund future capital expenditure.

The Orkney County Council Act 1974 and the Zetland County Council Act 1974 require Orkney and Shetland to also hold a Harbour Account, a separate account and reserve fund specifically for harbour undertakings. Orkney and Shetland are also able to transfer money between their General Fund and their Harbour Accounts. In this chapter Harbour Account figures are presented separately, however they are included within General Fund figures in other chapters within this publication.

Where a council has housing stock, the accumulation of surplus income relating to housing is separately identified in their Housing Revenue Account (HRA).

In addition to the General Fund a local authority may also hold other statutory usable revenue reserves, such as a Renewal and Repairs Fund, an Insurance Fund, or other reserves specific to a local authority as permitted by legislation. Amounts will be transferred to and from the General Fund to these reserves.

Local authorities hold two capital reserves – the Capital Fund / Capital Receipts Reserve and a Capital Grants and Receipts Unapplied Account.

The Capital Fund and Capital Receipts Reserve were previously identified separately but are now treated as a single reserve. The Capital Fund / Capital Receipts Reserve may be used for the purpose of meeting the cost of capital expenditure and for the repayment of principal on loans, but not any interest on loans.

The Capital Grants Unapplied Account holds capital grant that has been received but not yet used to fund capital expenditure, or capital receipts held pending their funding of specific expenditure as permitted by Scottish Ministers.

Local authorities also hold a number of unusable reserves, that is reserves which are not backed by cash resources and cannot be used to fund services. Unusable reserves include a Revaluation Reserve, where increases in the value of fixed assets are recorded. This reserve is not usable as an increase in value of an asset will not be realised until the asset is sold. Other unusable reserves include sums deferred or set aside as statutory adjustments which are used to ensure the Annual Accounts of a local authority reconcile to statutory requirements. As these are unusable reserves, they are not discussed in this publication. However this data is collected as part of the Local Financial Returns and is available in the published LFR 23 workbook. A summary of the movement in each unusable reserve in 2022-23 is also provided in the ‘SLGFS 2022-23 – Additional Analysis – Reserves’ supporting excel file.

A change in accounting practice in 2018-19 (IFRS 9) resulted in unrealised gains in the value of investments held by local authorities being included in the General Fund / HRA / Harbour reserve balances, rather than in an unusable reserve as before. This gain is unrealised as the investment is still held and any gain will only be realised if the investment is sold. The unrealised gain is therefore required to be earmarked and is not available to fund future revenue expenditure or to fund capital investment. The value of usable reserves presented in this publication therefore exclude any IFRS 9 unrealised gains held as part of the General Fund / HRA balances.

Table 4.1 sets out the movements across all reserves in 2022-23. Figures relating to the General Fund (including Harbour Account figures) and HRA were also presented in Chapter 2.4.

Local authorities had an increase of £118 million in their revenue reserves, and an increase of £222 million in their capital reserves in 2022-23. This means local authorities’ usable reserves increased by £339 million overall, from £4,193 million at 1 April 2022 to £4,532 million at 31 March 2023.

| Usable Reserve | Level of reserves held at 1 April 2022 | Net increase (+) or decrease (-) in year | Level of reserves held at 31 March 2023 |

|---|---|---|---|

| General Fund | 2,693 | 177 | 2,870 |

| Housing Revenue Account | 215 | -6 | 209 |

| Harbour Account | 331 | -22 | 309 |

| Renewal and Repairs | 190 | -24 | 166 |

| Insurance Fund | 95 | -4 | 91 |

| Other Statutory Funds | 9 | -4 | 6 |

| Total Revenue Reserves | 3,533 | 118 | 3,650 |

| Capital Fund / Capital Receipts | 466 | 46 | 512 |

| Capital Grants and Receipts Unapplied | 194 | 176 | 370 |

| Total Capital Reserves | 660 | 222 | 882 |

| Total Usable Reserves | 4,193 | 339 | 4,532 |

Please note that level of reserves held at 1 April and 31 March exclude amounts relating to unrealised gains that are included in revenue reserves in statutory Annual Accounts applying IFRS 9: Financial Instruments.

Source: LFR 23

The majority of the increase in usable reserves relates to an increase in the General Fund of £177 million between 1 April 2022 and 31 March 2023, and an increase in Capital Grants and Receipts Unapplied of £176 million.

Glasgow City Council’s Capital Grants and Receipts Unapplied reserves has increased by around £195 million over the year, and was £216 million as at 31 March 2023. Of this, Glasgow City council have set aside £200 million to fund the equal pay settlement.

As part of the annual budget setting process, the Scottish Government commits to providing a level of funding to Councils in the form of general and specific revenue and capital grants.

Specific revenue grants must be used to meet a specific Scottish Government priority and any unused specific grant can only be carried forward with the consent of the Scottish Ministers. General Capital Grant must be spent in the year received and any unspent General Capital Grant is required to be returned to the Scottish Government at the end of the financial year and may not be held in reserves. In both cases therefore, if this funding is not otherwise utilised within the financial year by the Scottish Government, then it will be reported within reserves as part of the Scottish Government Consolidated Accounts. If consent is provided to carry forward a specific revenue grant this will be disclosed in the local authority’s annual accounts as an earmarked reserve.

Earmarked reserves are held for a specific purpose, the majority of which will be fully committed to existing spend programmes and represent the extent to which resources are received or generated in advance of the actual spend.

Local authorities are able to earmark, or set aside, part of their General Fund reserves for future use for a specific purpose. At 31 March 2023, local authorities’ had earmarked 83.3 per cent, or £2,390 million of the £2,870 million General Fund reserves. These figures exclude amounts relating to unrealised gains that are included in revenue reserves in statutory Annual Accounts applying IFRS 9: Financial Instruments.

Councils may hold an additional unearmarked amount to mitigate financial risk. This amount equated to £480 million as at 31 March 2023, or 2.1% of Gross Service Expenditure (£23,391 million).

Table 4.2 sets out the level of reserves held across all local authorities in Scotland at 31 March 2019 to 31 March 2023. Over this five year period, the most significant change is between 31 March 2020 and 31 March 2021, caused by Covid-19 pandemic money provided late in 2019-20.

| Usable Reserve | 31-Mar-19 | 31-Mar-20 | 31-Mar-21 | 31-Mar-22 | 31-Mar-23 |

|---|---|---|---|---|---|

| General Fund | 1,143 | 1,315 | 2,274 | 2,687 | 2,870 |

| HRA | 177 | 188 | 248 | 215 | 209 |

| Harbour Account | 314 | 269 | 328 | 331 | 309 |

| Renewal and Repairs | 138 | 141 | 177 | 190 | 166 |

| Insurance Fund | 90 | 102 | 99 | 95 | 91 |

| Other Statutory Funds | 12 | 13 | 14 | 9 | 6 |

| Total Revenue Reserves | 1,874 | 2,027 | 3,141 | 3,527 | 3,650 |

| Capital Fund / Capital Receipts | 491 | 475 | 464 | 461 | 512 |

| Capital Grants and Receipts Unapplied | 180 | 207 | 227 | 175 | 370 |

| Total Capital Reserves | 671 | 681 | 691 | 636 | 882 |

| Total Usable Reserves | 2,546 | 2,708 | 3,832 | 4,163 | 4,532 |

Please note the following:

Figures exclude amounts relating to unrealised gains that are included in revenue reserves in statutory Annual Accounts applying IFRS: Financial Instruments.

Figures for 31 March 2022 may not match the 1 April 2022 figures shown in Table 4.1 due to restatements in local authorities' accounts between years.

Figures for 31 March 2021 and 31 March 2022 may differ from previous publications due to audited accounts being submitted after SLGFS 2021-22 was published. These figures have been revised for this publication. See the introduction for more information.

Source: LFR 23

4.2 Fixed Assets

Capital expenditure creates local authority assets. In 2022-23, the value of local authority fixed assets was £55,261 million, an increase of 3.8 per cent, or £1,999 million, from 2021-22. The value of local authority fixed assets from 2018-19 to 2022-23 is shown in Table 4.3.

| Fixed Asset Type | 31-Mar-19 | 31-Mar-20 | 31-Mar-21 | 31-Mar-22 | 31-Mar-23 | % change between 31 March 2022 and 31 March 2023 |

|---|---|---|---|---|---|---|

| Operational assets | 44,242 | 46,110 | 47,766 | 50,822 | 52,536 | 3.4% |

| Non-operational assets | 1,875 | 2,139 | 2,384 | 2,336 | 2,610 | 11.7% |

| Intangible assets | 65 | 65 | 85 | 103 | 115 | 11.3% |

| Total Assets | 46,182 | 48,315 | 50,234 | 53,261 | 55,261 | 3.8% |

Source: LFR CR for 31 March 2020 onwards, CR Final for 31 March 2019

Operational assets are assets a local authority can use when providing services, such as a school, council houses, vehicles etc. Almost all of local authorities’ fixed assets are operational assets (95 per cent of total assets) and the value of these has increased by 3.4 per cent, or £1,714 million, from 2021-22 to 2022-23.

Non-operational assets are assets that a local authority cannot currently utilise, for example an asset that is still under construction or an asset that is being held for disposal. Intangible assets are non-physical assets, such as computer software. Non-operational assets and intangible assets together accounted for 4.9 per cent of local authorities’ total fixed assets in 2022-23.

Contact

Email: lgfstats@gov.scot

There is a problem

Thanks for your feedback