Coronavirus (COVID-19): Scotland's Strategic Framework update - February 2022

This update of the Strategic Framework assesses where we are in the pandemic and sets out Scotland’s approach to managing COVID-19 and its associated harms effectively for the long term as we prepare for a calmer phase of the pandemic.

This document is part of a collection

Overview

The last Strategic Framework update in November 2021 anticipated a challenging winter ahead, and noted the risk of a new variant. It underlined the need to remain cautious, even as we continued on a generally improving trajectory in our management of COVID-19. It set out the measures we were retaining to help keep people safe and noted that we would act quickly in response to deteriorating epidemiological conditions, such as a new variant.

That risk of a new variant materialised quickly. The Omicron variant was categorised as a Variant of Concern by the World Health Organisation (WHO) on 26 November. From the early data it became clear that Omicron had a significant growth advantage over Delta, the previous dominant variant in Scotland. Omicron is more able than Delta to infect people who have been vaccinated or who have had a previous infection. It has multiple genetic mutations that enable it to better evade antibodies and other immune responses developed through vaccination or natural infection.[1]

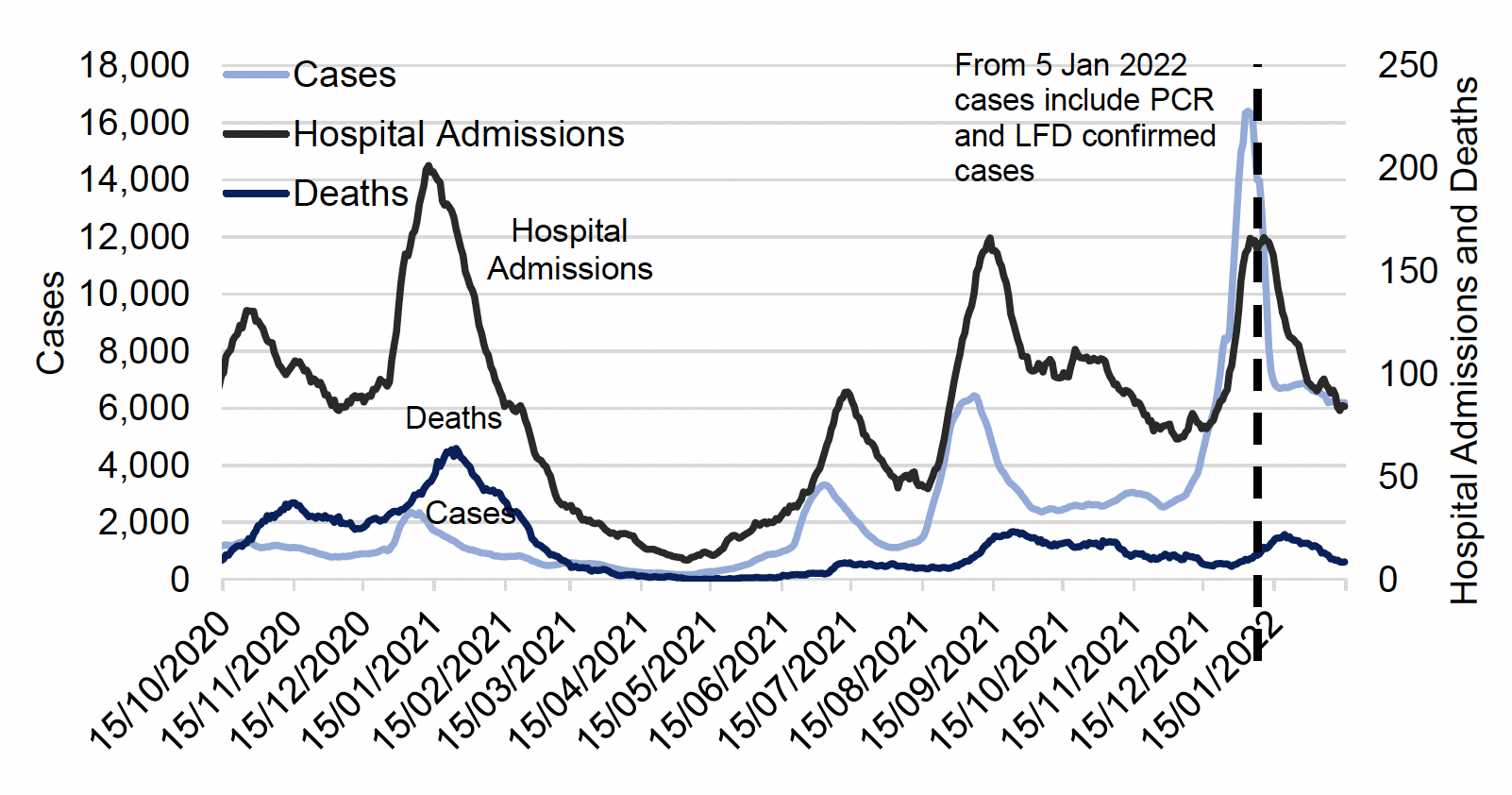

Despite international efforts to slow the spread of the virus through targeted travel measures, Omicron quickly took hold in Scotland and around the world. It was first reported in Scotland on 29 November 2021 (based on a sample from 23 November), became the dominant strain on 17 December,[2] and led to a rapid escalation of cases (at a time of year when upward pressure on cases was likely even without a new variant). Cases peaked on 3 January 2022 at 16,407 weekly average PCR (polymerase chain reaction) confirmed cases per day - considerably higher than previous peaks.[3]

It was not clear in the early stages whether Omicron would be more or less severe in terms of disease than Delta. Subsequently, research has indicated that Omicron infections are generally less severe and less likely to result in hospital admission than Delta.[4] [5] Preliminary data from the UK Health Security Agency (UKHSA) indicate that the risk of attending hospital or emergency care is estimated at around half for Omicron compared to Delta, and the risk of being admitted to emergency care around one third of Delta.[6]

Notwithstanding the reduced severity of Omicron, given the sheer scale of cases, pressure on the NHS increased, on top of already significant general pressures. COVID-19 hospital admissions peaked at a seven day average of over 160 per day at the beginning of January 2022. This was at a similar level to the previous peaks in September 2021 (peaking at an average of over 160 per day) but lower than the peak in January 2021 (peaking at an average of over 200 per day), see Figure 3. Weekly average hospital occupancy for COVID-19 positive patients peaked at over 1,500 per day in mid-January 2022.[7]

The high number of infections also accentuated pressure on the COVID-19 testing system and led to a change in testing approach (those with no symptoms were no longer asked to take a PCR test to confirm a positive LFD test).[8]

Consistent with the approach set out in the previous Strategic Framework, temporary, targeted protective measures were implemented as a proportionate response to the threats posed by Omicron. On 17 December 2021, legal requirements were introduced for businesses and other organisations to take reasonable measures to reduce transmission. Guidance was given to limit indoor socialising to three households with LFD testing before meeting. On 26 and 27 December 2021, restrictions on event capacity were introduced, one metre physical distancing was required in hospitality and leisure facilities, table service was required in hospitality where alcohol was served, and nightclubs were closed.

Another key part of our response to Omicron was to expand the booster vaccination campaign and accelerate the vaccine roll-out more generally. Eligibility for boosters was expanded to over 40s on 30 November, while 16-17 year olds were able to book their second dose.On 15 December, booster eligibility was further expanded to over 18s.Thanks to the unprecedented rates of vaccine take-up from people across Scotland, over 3.3 million people (70.6% of those over 12 years of age) have received their third dose or booster vaccine by 18 February 2022.[10] Scotland is the most vaccinated per capita of the four nations in the UK across first, second, third and booster doses.[11]

In combination with people behaving more cautiously in response to the deteriorating situation, as evidenced in data including from the contact survey,[12] and with the increasing impact of booster vaccination, the additional, targeted measures helped to reduce the spread of Omicron in Scotland. They also limited the ensuing increase in morbidity and mortality from levels they might otherwise have reached.

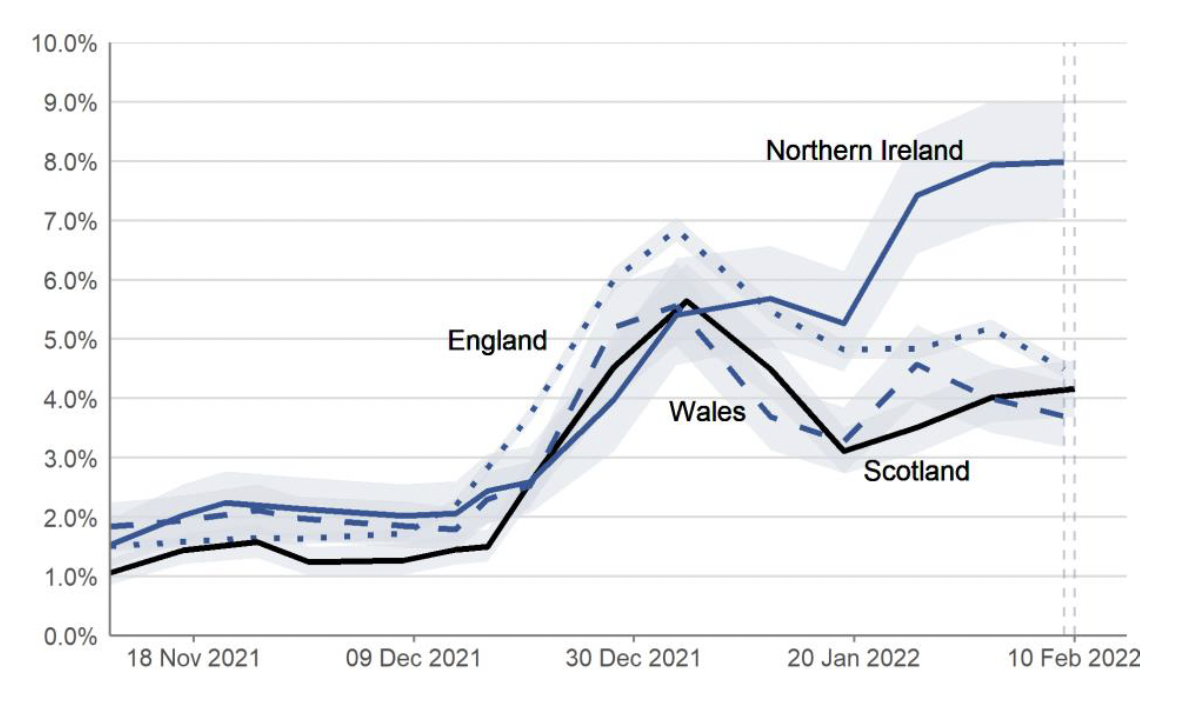

As can be seen in Figure 4, COVID-19 prevalence in Scotland peaked in early January and has since fallen, though it remains at a high level. The observed improvement has translated, following expected lags, into reduced hospital admissionsand to reduced hospital and ICU occupancy. This has eased some of the most acute pressures on the NHS, though significant general pressures remain.

Once the peak in Omicron infections had passed and we were confident that infections were on a downward trajectory, we moved quickly to begin the phased easing of the temporary measures that had been put in place to provide extra protection against Omicron. Limits on largescale outdoor events were removed on 17 January 2022 alongside physical distancing requirements at outdoor event venues, outdoor exhibitions and outdoor spaces in sports stadia. The majority of the protective measures implemented after Christmas were lifted by 31 January, along with the guidance to limit socialising indoors to three households. The COVID-19 certification scheme was adjusted to permit the use of a negative test on 6 December and to add the requirement for a third dose on 17 January.)

Although economic and broader societal activities would have been curtailed by Omicron even in the absence of additional protective measures, as people exercised more caution, we acknowledge the impact of these measures on affected sectors. To support these sectors through this challenging period, we committed £375 million of additional financial support.

Though a number of sectors continue to face significant challenges as a result of the pandemic, the general economic situation has improved in a number of respects. Overall economic output in Scotland, as measured by Gross Domestic Product (GDP), recently returned to its pre-pandemic level of February 2020 for the first time. Latest monthly data show Scotland's GDP grew 0.8% in November and is 0.6% above its pre-pandemic level. In January 2021, 82% of businesses were trading in some form compared to 98% of businesses in January 2022.

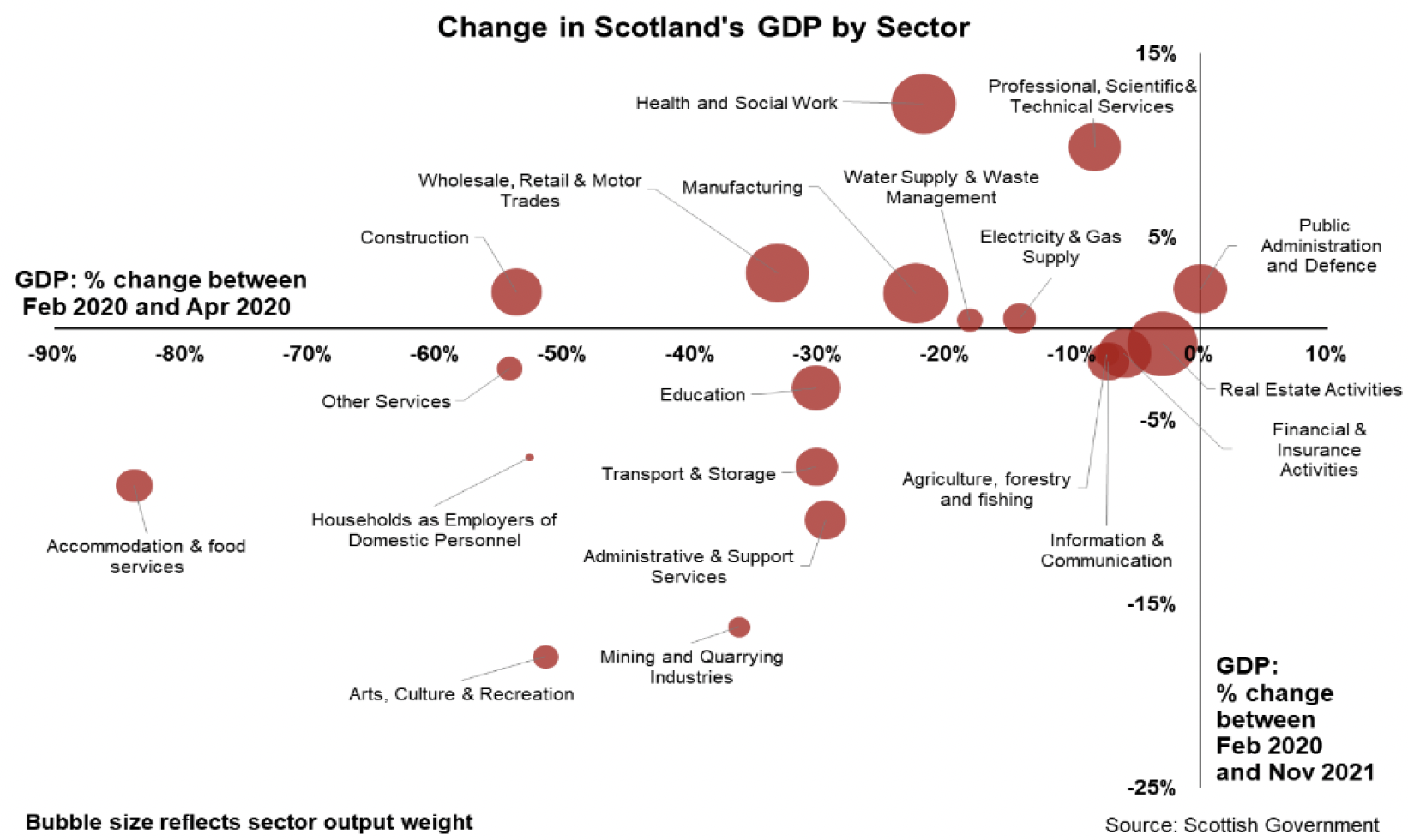

The economic impacts of the pandemic have been felt unevenly across sectors, with those most affected by restrictions being the hardest hit, with the impacts felt by businesses, customers and those whose livelihoods depend on them. Consumer-facing service sectors, such as hospitality, remain notably below pre-pandemic levels. Figure 6 shows that economic output in hospitality in November 2021 was 8.5% below pre-pandemic levels of output and arts, culture and recreation services were 17.9% below. Business resilience remains a key challenge, with data for January 2022 showing that 21.4% of hospitality businesses have less than three months of cash reserves.

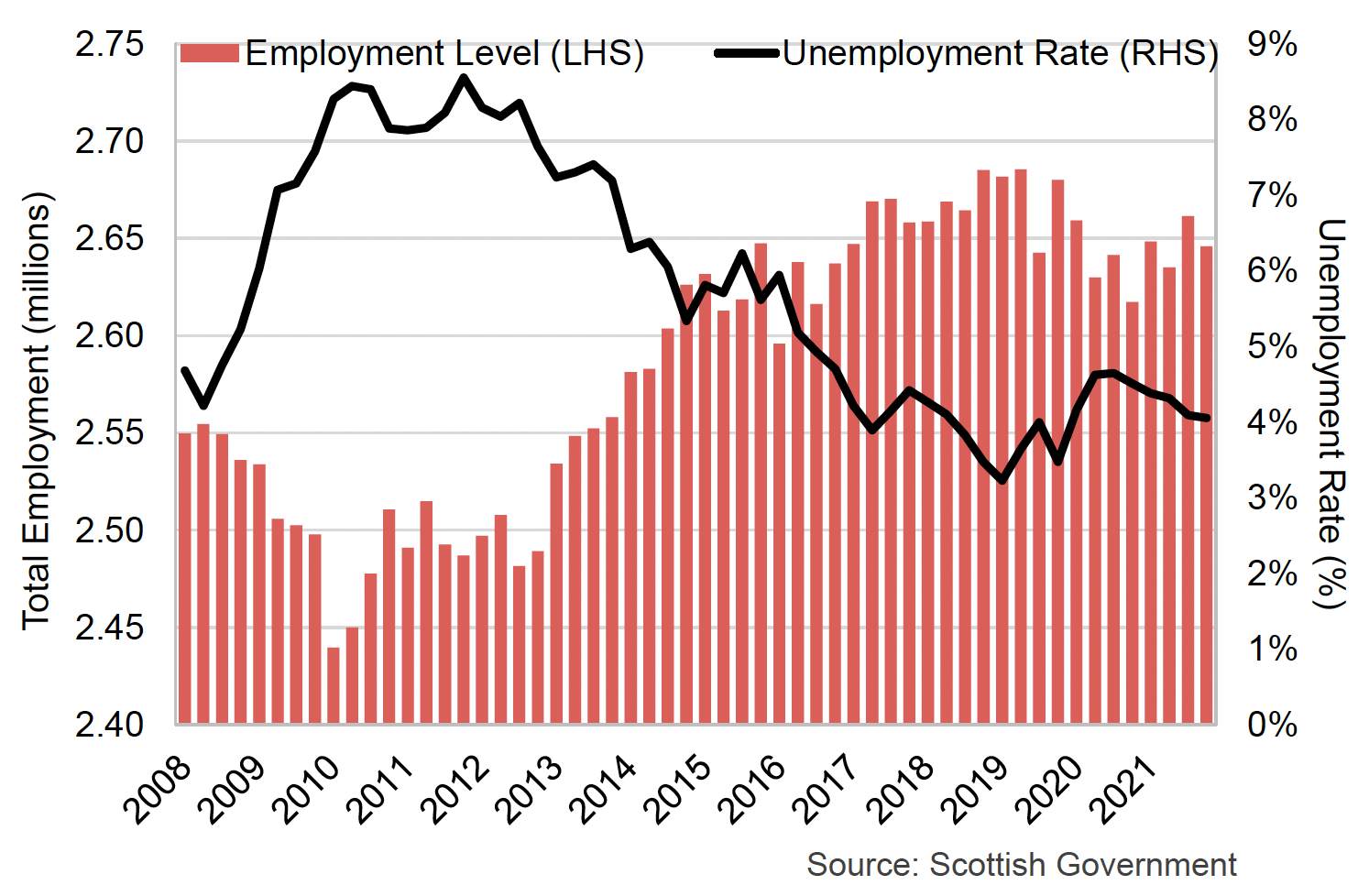

Labour market indicators are strong, reflecting the impact of the furlough scheme in protecting jobs to its completion at the end of September 2021. The latest labour market statistics for October to December show that 2.65 million people were employed in Scotland, an employment rate of 74.1% (up 0.8 percentage points over the year), and the unemployment rate was 4.1% (down 0.5 percentage points over the year) (see Figure 7).

Notwithstanding the various positive signs for the economy overall, key economic challenges remain, such as the ongoing impacts of BREXIT and broader supply chain issues, staff shortages, pressures on costs for businesses and households, some related to the energy market as well as the cumulative impacts of the pandemic. These impacts are being felt more acutely in particular sectors of the economy and groups in society. Self-isolation rules, particularly during the Omicron wave, added to these challenges.

In the 7 day period to 10th February 2022, visits to workplaces in Edinburgh remain 31% below pre-pandemic levels and those in Glasgow 26% below.[14] The decrease in visits to workplaces as a result of more people working from home has provided benefits over and above reducing infections, with people reporting that they welcome the increased flexibility and reduced commuting costs, and contributed to growth in some local businesses. However, it has negatively affected businesses that rely on office trade, particularly in city centres. And these impacts have not been distributed equally, with certain sectors and professions able to work from home whilst others cannot and have therefore been much more exposed to workplace-related transmission and the threat of workplace closures and lost income.

Effective management of COVID-19 going forwards will strengthen the economy; our forthcoming National Strategy for Economic Transformation will set out how we plan to transform the economy over the next decade.

Throughout this recent, challenging period, schools and other educational institutions were generally able to remain open, though protective measures have remained in place and activities and settings have sometimes been disrupted by the high number of infections. School attendance has generally remained high. Nevertheless, the pandemic has negatively impacted on relationships and development among babies and children, and on concentration and learning in primary school-aged children[15] and has also hampered our efforts to improve school attainment and reduce inequality. In further and higher education, while online learning has allowed for the continuation of many courses, some students have disengaged with online provision, others have been disadvantaged by lack of access to placements and practical training and some have chosen not to take up or have dropped out of courses in greater numbers than before the pandemic. This underlines the need to make education as close to normal as we can in the near future.

More generally, COVID-19 has continued to weigh on us as a society – as it has internationally – affecting our mental health, broader sense of wellbeing, and our ability to make plans for the future.

Throughout the pandemic levels of anxiety and loneliness have been much higher, particularly amongst younger people and disabled people.[16] Managing the risk of exposure to COVID-19, both by adhering to protective measures, and by choosing to take other risk-reducing measures has reduced social connection. People have fewer social contacts per day, have reduced participation in sporting, cultural and other activities and whilst there was an increase in informal help and support in the early stages of the pandemic, this has declined over time.

Despite this, one constant positive throughout these difficult times has been the high levels of public support for protective measures in Scotland, and the willingness of people to adhere to them, often at some personal cost. 76% of people in Scotland say they are happy to follow some rules and guidance if it means they can do the things that matter to them, and 75% agree they have a responsibility to follow the rules and guidance from the Scottish Government to keep others safe.[17] This sense of social cohesion and collective responsibility has been central to our management of the pandemic.

Recent polling data show that, as we move ahead into 2022, after two long years of the pandemic, there is an air of increased optimism in Scotland. Around half of people polled say they are sure things will get better soon, compared with only a quarter in the middle of December 2021.[18]

COVID-19 will not suddenly go away. However, there are good reasons to hope and expect that in Scotland we are now moving away from tackling COVID-19 as a crisis and towards a calmer phase in which the virus transitions to becoming endemic. It may be liable to periodic surges due to the ongoing risk of new variants - and some short-term measures may be necessary in response - but we should still be able to effectively manage COVID-19 as we do other diseases, with much less recourse to restrictive protective measures than in the past. The next section will set out clearly how we plan to do that.

As we have described, the impacts of COVID-19 are widespread and long-lasting. It will take time to recover, which is why we are focused, alongside managing the ongoing threat of COVID-19, on supporting the recovery and rebuilding for a better future set out in our COVID-19 Recovery Strategy. This Strategic Framework helps to set the solid platform for that broader recovery and later sections of this document will also point to the recovery work taking place at pace across many different fronts.

Contact

Email: CEU@gov.scot

There is a problem

Thanks for your feedback