Heat in Buildings Bill consultation: business and regulatory impact assessment (partial)

Business and regulatory impact assessment (partial) in support of consultation on proposals for a Heat in Buildings Bill.

Costs and Benefits

9.1 This section provides a qualitative assessment of the use of a cohesive strategy based on a combination of regulatory, economic and behavioural change initiatives (option 2) as compared with BAU (option 1). Given the proposed option comprises a comprehensive policy package, covering both regulatory and non-regulatory action most of which is in the early stages of development, it is not possible to provide a detailed appraisal of the costs and benefits at this stage. The focus here is on the role of non-regulatory actions providing mitigation to the impacts of the regulatory actions.

Qualitative Assessment

9.2 The following provides a brief qualitative assessment of the two options against relevant criteria arising from the policy objectives and outcomes presented above.

Climate change mitigation

9.3 Option 1 (do nothing) will not achieve the levels of deployment of energy efficiency or zero emissions heat required to achieve emissions reductions for the Buildings sector and thus wider Climate Change objectives. This is due to a combination of supply and demand constraints, including a lack of public engagement, misaligned incentives, underdeveloped supply chains and skills gaps which taken together suggest the continued deployment of zero emissions heat will be limited and an ongoing reliance on fossil fuelled heating systems. Through a coordinated approach, including regulatory and non-regulatory action, Option 2 provides a framework to drive up the deployment and ensure the building sector begins to make a contribution to overall emissions targets, giving a clear direction of travel, including dates, to the supply chain.

Fuel poverty reduction

9.4 The Heat in Buildings Strategy recognises reaching emissions reduction and fuel poverty targets simultaneously is challenging, but we are committed to ensuring we decarbonise in a manner that does not increase the rate or depth of fuel poverty. We know that zero emissions heat can be more expensive to run than a modern efficient fossil fuel boiler and we remain committed to taking forward no action that could have a detrimental impact on fuel poverty rates, unless additional mitigating measures can also be put in place.

9.5 Scottish Government investment is underway and will provide direct mitigation through existing programmes including Warmer Homes Scotland, our flagship fuel poverty scheme, Home Energy Scotland and the Social Housing Net Zero Heat Fund. For domestic properties, Scottish Government currently fund 100% of the clean heating system and the related energy efficiency works for those in fuel poverty, and offers a grant of up to £7,500 for installation of a heat pump for other owner occupiers along with up to £7,500 loan for energy efficiency works.

Economy

9.6 Analysis suggests the heat transition, through investment in the deployment of energy efficiency and zero emissions heat, could significantly benefit the Scottish economy through employment opportunities. Under Option 1, without further action investment and deployment will remain marginal and the extent of the economic benefits outlined will not be realised.

9.7 In contrast, Option 2, through coordinated regulation and non-regulatory support schemes, will provide certainty to the market and drive deployment, securing and maximising economic opportunities. By promoting innovation and skills development, not only will the combined approach of regulation and incentives and support provide high quality jobs, it may also position Scotland to take advantage of export opportunities.

9.8 It is important to note, however, the potential for displacement such that the level of positive net impact on jobs may be more limited, and that while certain sectors are likely to benefit from the transition (energy efficiency, and low and zero emission fuels and technologies), others may see a reduction in their market (high carbon fuels and technologies). However, existing firms may be able to switch from supply associated with fossil fuel to zero emissions, and policy development will seek to ensure barriers to entry are minimised.

9.9 We are committed to building local supply chains, maximising local job creation, and ensuring a just transition. We will work with Scottish businesses so that they can play a significant part in the transformation of Scotland's homes and buildings, and work with industry bodies to enable existing gas and oil boiler installers to offer expert knowledge on alternative systems.

Deliverability and quality

9.10 Without additional direct government intervention and the certainty and clarity provided by proposed regulation, it is unlikely that the clean heat sector will have sufficient incentives to invest in developing supply chains and upskilling their workforce to match the deployment levels required to meet emissions reduction objectives, which are far higher than current rates. This could lead to lower standards, with poor performance resulting from misspecification, particularly in the case of heritage or other hard-to-treat buildings where a specialised skillset may be required. Therefore, Option 1 poses risks in terms of deliverability and quality, which are addressed specifically under Option 2 which relies on broad engagement with the UK Government, skills delivery partners and the supply chain to ensure the necessary skills, quality assurance, accreditation and standards are in place to support deployment and drive high standards necessary to deliver the changes brought about through the setting of regulated standards.

Affordability and value for money

9.11 The upfront cost of installing a clean heating system is often significantly higher than replacing incumbent polluting boilers, and as noted above, may lead to increased fuel bills. Therefore, there are affordability concerns associated with the mass deployment of clean heating systems. However, steps can be taken to ensure affordability and value for money. As the clean heat market is relatively immature, there may be opportunities for economies of scale as demand increases and businesses can increase the efficiency of their production processes, leading to lower costs for consumers.

9.12 Under Option 1, without kick-starting deployment at scale, it is unlikely that these efficiencies will be realised. There may also be increased running costs associated with misspecification where skills and standards are not in place, or where energy efficiency and clean heat are not considered in tandem, potentially leading to suboptimal outcomes.

9.13 Option 2, by taking a holistic view to energy efficiency and clean heat, whilst targeting skills and embedding standards, is more likely to lead to cost-effective outcomes for households and businesses. Furthermore we have established a Green Heat Finance Taskforce which is exploring potential new and value for money innovative financing mechanisms for both at-scale and individual level investment. Our holistic approach to heat in buildings reflects our broader commitment to taking a whole system view, and will support identification of least cost options and coordination efficiencies.

9.14 The heat transition will necessarily require significant investment, and by putting in place both regulatory and non-regulatory support, there is increased likelihood of attracting private sector investment, while putting in place mechanisms to support those less able to pay. Taking a holistic and strategic approach allows an accurate assessment of how costs will be recovered to ensure these, alongside benefits, are distributed fairly.

Population and human health

9.15 Option 1 will not deliver significant changes to health outcomes. Option 2, through the deployment of energy efficiency, may provide health benefits through improvements to thermal comfort and in particular prevent fuel poverty worsening. Furthermore, switching away from polluting heating systems may have additional benefits in terms of reducing pollution and improving air quality. The impact on the population and human health will be considered further.

Quantitative Assessment

9.16 As policies are not yet fully developed and the proposals are now the subject of consultation, this section provides necessarily high level estimates. All figures should be treated as indicative and viewed in the light of current uncertainties around key aspects of the transition.

9.17 The changes to our buildings and systems that are needed to eliminate emissions from heating comprise both capital investment and ongoing costs. Different pathways and options have different balances as to where these costs arise.

9.18 How heat consumers are exposed to these costs, e.g. whether through bills, upfront costs, or taxes, depends on policy choices, energy market frameworks and new business models (such as heat-as-a-service). This diversity in potential outcomes further underscores the rationale for this impact assessment to take a broad qualitative approach, with quantitative assessment deferred to more specific policy development.

9.19 The total gross capital cost of converting buildings stock to clean heat, including energy efficiency upgrades, has been estimated in the region of £33 billion, with additional investment required to upgrade energy networks and ensure sufficient energy generation capacity. This is an estimate of the gross cost and does not take account of investment in fabric measures and boiler replacements in a business-as-usual scenario. For example, it would cost around £5 billion to replace existing fossil fuel heating systems in the domestic sector on a like-for-like basis. This figure is under review.

9.20 We also anticipate that, under the current market framework and electricity pricing structure, clean heat could result in increased running costs for some, however this may be partly or fully offset by the higher efficiency of some clean heating systems, demand reduction through improved energy efficiency and targeted support where appropriate.

9.21 In recent years, several key factors have shown high level of variation, resulting in uncertainty around the impact of the transition to clean heating:

- Fluctuations in energy prices have resulted in, on average, significantly higher fuel bills for most households, and therefore more households facing fuel poverty.

- Associated with this, inflation in the UK has been highly variable. While not consistent across all goods and services, this is likely to result in higher nominal costs of the conversion.

- The rate of clean heating installation has increased significantly since 2015. While this reduces the total number of buildings to move to clean heating, without regulation, the increased rate is still not sufficient to meet climate targets.

- Living and working patterns have changed during and since the COVID-19 pandemic, with many more people working from home. As a result, the average energy intensity of a home in Scotland has increased on previous years.[32]

9.22 While cost projections are subject to considerable uncertainty, the finding that low and zero emissions heating is likely to add whole-system lifecycle costs relative to the incumbent system is robust, reflecting a wider range of estimates.[33]

Residential buildings: Upfront building-level costs

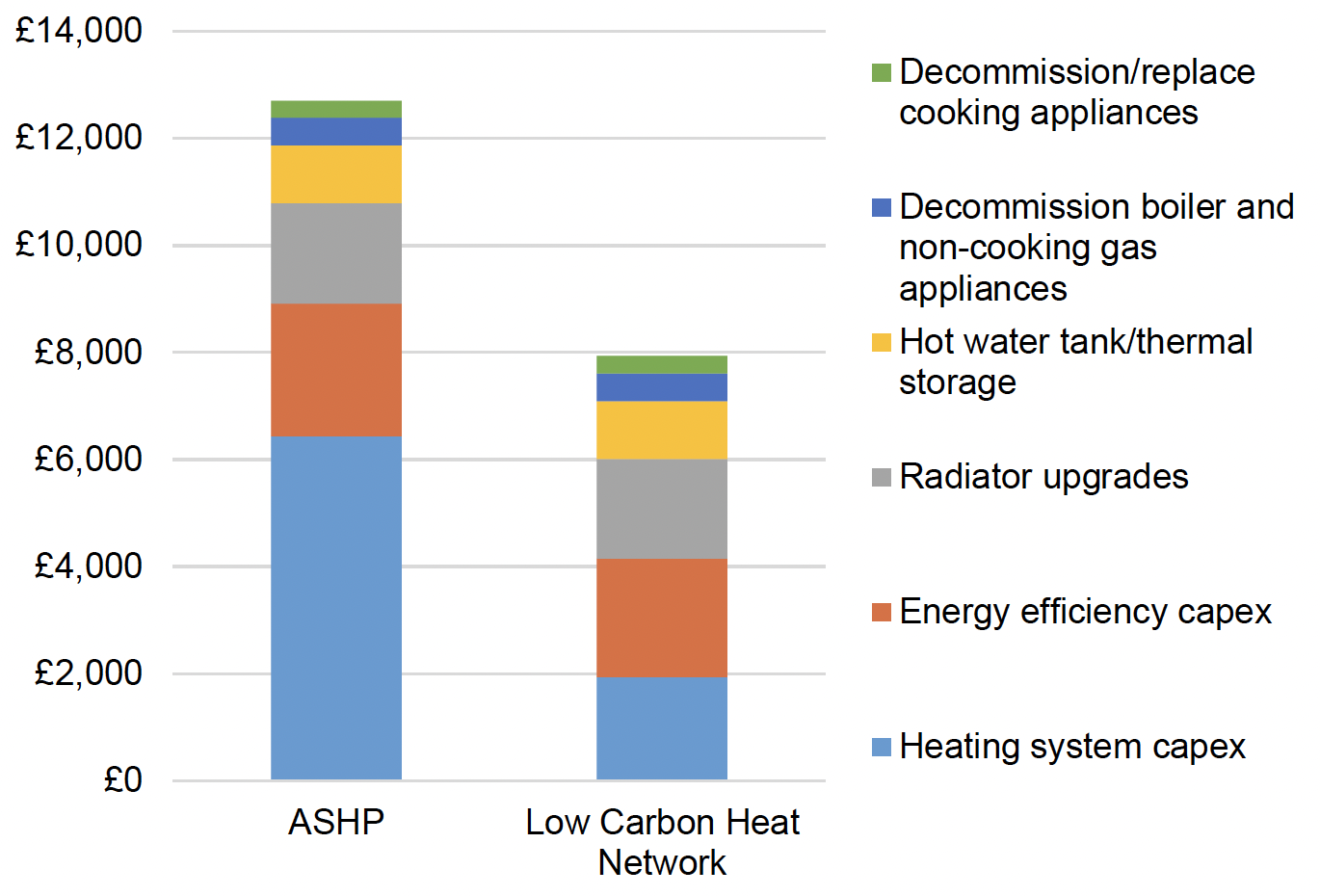

9.23 Heat pumps and heat networks can be deployed in many areas and buildings as no- or low-regrets interventions to reduce direct emissions from buildings. The capital cost of a heat pump alone is estimated at under £7,000; however, there are additional costs associated with decommissioning and water/thermal storage, which on average cost an additional £2,000. Many Scottish homes will also need energy efficiency upgrades if heat pumps are to run as efficiently as possible, which are estimated at an average of around £4,500. Therefore, the average total estimated cost to convert a home to highly efficient ZDEH is estimated at around £14,000.[34]

9.24 More recent research has estimated the potential costs of upgrading the Scottish housing stock to adequate levels of energy efficiency. These estimates vary based on the approach taken, with some homes likely needing very high levels of intervention to achieve energy efficiency sufficient to support the efficient running of a heat pump. On average however, these estimates are broadly in line with the CCC estimates above.[35]

9.25 By comparison, replacing a fossil fuel boiler (without fabric upgrades) costs in the region of £2,000 to £3,000.

Source: Element Energy (2020) "Development of trajectories for residential heat decarbonisation to inform the Sixth Carbon Budget" study for the Committee on Climate Change.[36]

Residential Buildings: Operating costs

9.26 The impact on energy bills of converting a home from fossil fuel heating to a zero emissions system depends on property characteristics such as build form, occupancy levels, and fabric efficiency. The retail cost of energy is also an important factor. Environmental and social obligation costs (levies) play a significant role in the relative costs of different options. The development of UK Government policy in this area, along with future evolution of wholesale and other system prices, means forecasting future relative operating costs is challenging. Therefore, this section considers the impact on fuel bills of adopting strategic zero emissions heat technologies according to existing evidence, but it should be noted that recent fluctuations in energy costs are likely to have a significant impact on these findings.

9.27 Heat pumps are a key zero emissions technology, and a very efficient way of using electricity to provide heat . Although one kWh of electricity is currently more expensive than one kWh of gas (currently by a factor of about 3), the median energy efficiency of an Air Source Heat Pump (ASHP) is nearly 250%, meaning that the energy demand is significantly lower. This means that for some properties, heat pumps can help reduce bills where they are replacing older, more inefficient oil and gas heating systems, or where they are combined with upgrades to the efficiency of the building's fabric. Modelling undertaken using the National Household Model shows that for the vast majority of Scottish dwellings using fossil fuels and which are below the equivalent of an EPC C, modelled fuel costs can fall where a heat pump is installed along with fabric measures, supplemented in some cases by solar PV or solar thermal. Conversely, properties currently using fossil fuels that have already attained the equivalent of an EPC C may have fewer options to offset the increase in fuel costs due to change in heating system. This latter group comprises around half of homes that use gas and around 8% of homes that use oil. [37]Nevertheless, these results are highly sensitive to both fuel prices and behavioural factors.

9.28 Running costs when using a heat network are more difficult to generalise, as they are dependent on the configuration of the network infrastructure (and hence capital cost that are recovered through bills) and the particular heat sources used. Heat networks are often suited to high density areas where per-connection network costs can be minimised. Larger networks are able to generally supply at lower cost, due to their lower average cost of development and operation, driven by factors such as more consistent demand, storage potential, renewable usage and available business models. Evidence collated by KPMG to inform the Heat Networks (Scotland) Bill Business and Regulatory Impact Assessment[38] suggests that heat networks could provide bill savings, with a potential saving of around 17% or 1.29 p/kWh in 2019 under a central scenario, and potentially ranging up to 36% under a high scenario. While further work is needed to estimate the range of heat network operating costs faced by users should networks extend to lower density areas, in this BRIA we assume they will generally be lower than levelised costs of alternative zero emissions options, as this represents an efficient resource allocation.

Non-Domestic Buildings costs

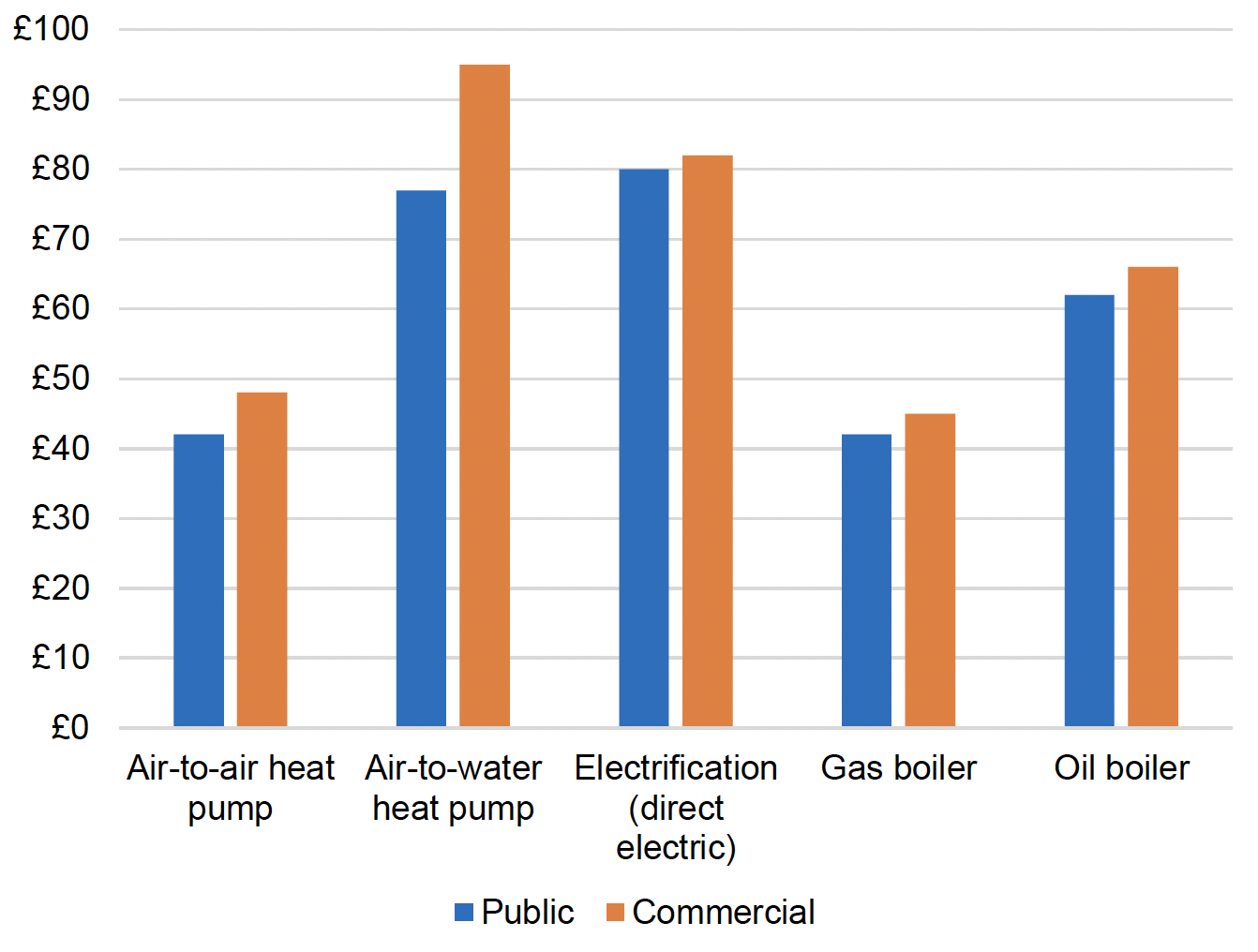

9.29 Figure 8 shows the estimated levelised costs associated with zero emissions heating options for non-domestic buildings, alongside equivalent costs for gas and oil boilers. These are presented on a £ per MWh basis. This is because the size, use and energy demand of non-domestic buildings varies significantly and to a much a greater extent than residential buildings. As such, average costs are unlikely to provide an accurate representation of the cost of zero emissions heat in the non-domestic sector.

Source: CCC Sixth Carbon Budget. Note: costs of capital of 3.5% assumed for public sector and 7.5% assumed for commercial

9.30 The levelised[39] costs of an air-to-air heat pump are similar to those of gas boilers at around £40-50/MWh. They present a potential saving in comparison to oil boilers, which are around £60-70/MWh. Air-to-water heat pumps are more expensive than both gas and oil boilers, at £77/MWh for public buildings and £95/MWh for commercial buildings, reflecting the relatively high upfront capital costs of air-to-water systems. Direct electric heating is also more expensive, at around £80/MWh, reflecting high fuel costs.

9.31 As stated above, there is a significant amount of heterogeneity present in the non-domestic stock. The decarbonisation solution selected for a given building will depend on its physical characteristics as well as the characteristics of the business that operates within it. Furthermore, we are not proposing to require non-domestic buildings to install energy efficiency measures to achieve a particular standard, as in the domestic sector, however some building owners may be incentivised to install energy efficiency measures to partially or fully mitigate any increase in potential operating costs. Therefore, non-domestic building costs are difficult to predict and subject to uncertainty, however we will continue to review and build the evidence base in this area.

Energy infrastructure and other costs

9.32 By 2030, a much larger proportion of heat demand will be electrified compared to today, supplied through either individual heat pumps or larger scale heat pumps supplying heat networks. In the wider context of policy initiatives to decarbonise other sectors such as transport and industry, there is significant potential for increased electricity demand in the future. This could have implications for both electricity generation capacity and distribution networks. Therefore, there is likely to be costs associated with increasing capacity and reinforcing networks. Given the electricity system's role in decarbonising services other than heat, the sharing and apportionment of these additional costs to zero emissions heat is difficult to specify. Due to the significant complexity and interdependencies, a robust estimate of these costs is not available currently. However, as set out in the Strategy, research is being commissioned to explore the likely range of network investment costs and potential impacts on consumers.

9.33 In addition to electrification, decarbonised gas is also likely to play a role (albeit a more limited one) in emissions reduction to 2030. This will involve increasing amounts of green gas (currently exclusively biomethane, but in the future also potentially hydrogen) being blended into the gas network. As committed to in the Strategy, the costs and benefits of increased hydrogen blending will be kept under review. Furthermore, subject to successful demonstration and safety case trials, parts of the gas network could be converted to 100% hydrogen and in the longer term this could play a vital role in decarbonising Scotland's building stock. This will require continued demonstration and rapid investment in hydrogen generation, storage, and the repurposing of the gas grid. The Energy Strategy refresh will provide more detail on the pathways to decarbonised gas and options for hydrogen for heat, and it is not possible to provide robust estimates of potential investment costs or the impact on consumers in the meantime. However, in all instances the evolution of energy infrastructure costs (both for electricity and gas) depends on UK Government action, as energy policy and regulation remains reserved.

Contact

Email: HiBConsultation@gov.scot

There is a problem

Thanks for your feedback