State of the economy: November 2021

This report summarises recent developments in the global and Scottish economy and provides an analysis of the performance of, and outlook for, the Scottish economy.

This document is part of a collection

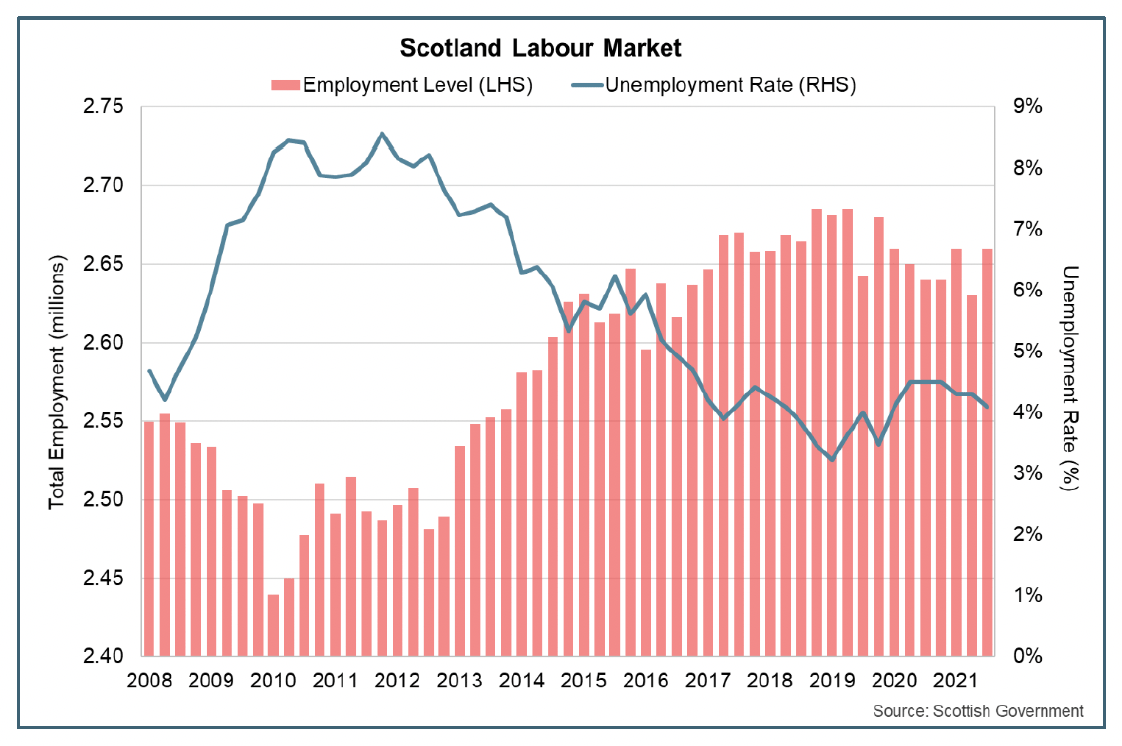

Labour Market

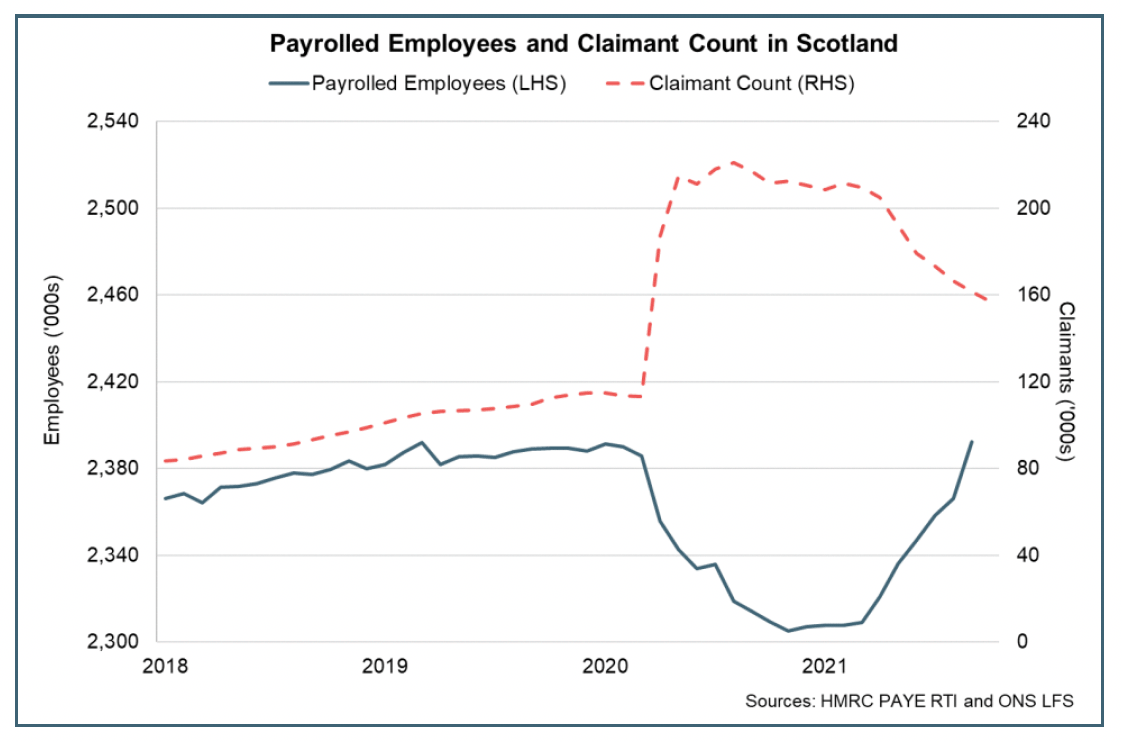

In October, the number of payrolled employees in Scotland rose back above its pre-pandemic level for the first time since the start of the pandemic, however the claimant count continues to fall more slowly.

Employment, Unemployment and Furlough

The unemployment rate has remained broadly stable since the start of the year, however the latest labour market statistics for July – September 2021 show Scotland's unemployment rate was 4.1%, down 0.2 percentage points over the quarter, and the lowest rate since the start of 2020 (3.7%, Dec-Feb 2020).

Scotland's employment rate in the 3-months to September was 74.8%, up 0.6 percentage points over the quarter, while the inactivity rate fell 0.4 percentage points to 22.0%, signalling some strengthening in the labour market as restrictions have eased.[18]

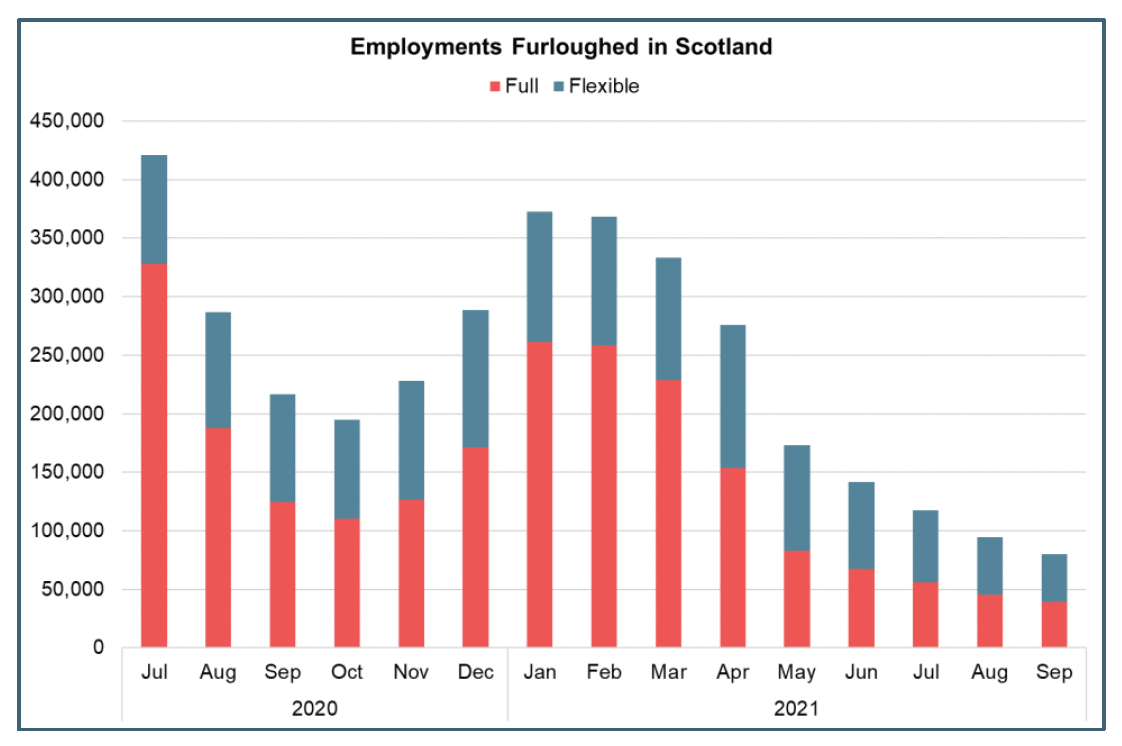

Up to the end of September, the Furlough Scheme was providing significant support to the labour market and the retention of jobs and earnings. Since its inception, the furlough scheme has supported 911,700 unique jobs in Scotland (11.7 million across the UK) and since its most recent peak of supporting 393,400 during lockdown restrictions in January this year, the number of jobs on furlough has naturally steadily fallen as restrictions eased and businesses resumed trading.

However, the ending of the support scheme at the end of September, provides a degree of uncertainty regarding the impact that this will have on businesses ability to retain staff that have remained most recently furloughed and the near term outlook for redundancies and unemployment.

At the end of September, 80,300 jobs in Scotland were furloughed (3% of eligible jobs), with 51% of those flexibly furloughed and 49% fully furloughed.[19]

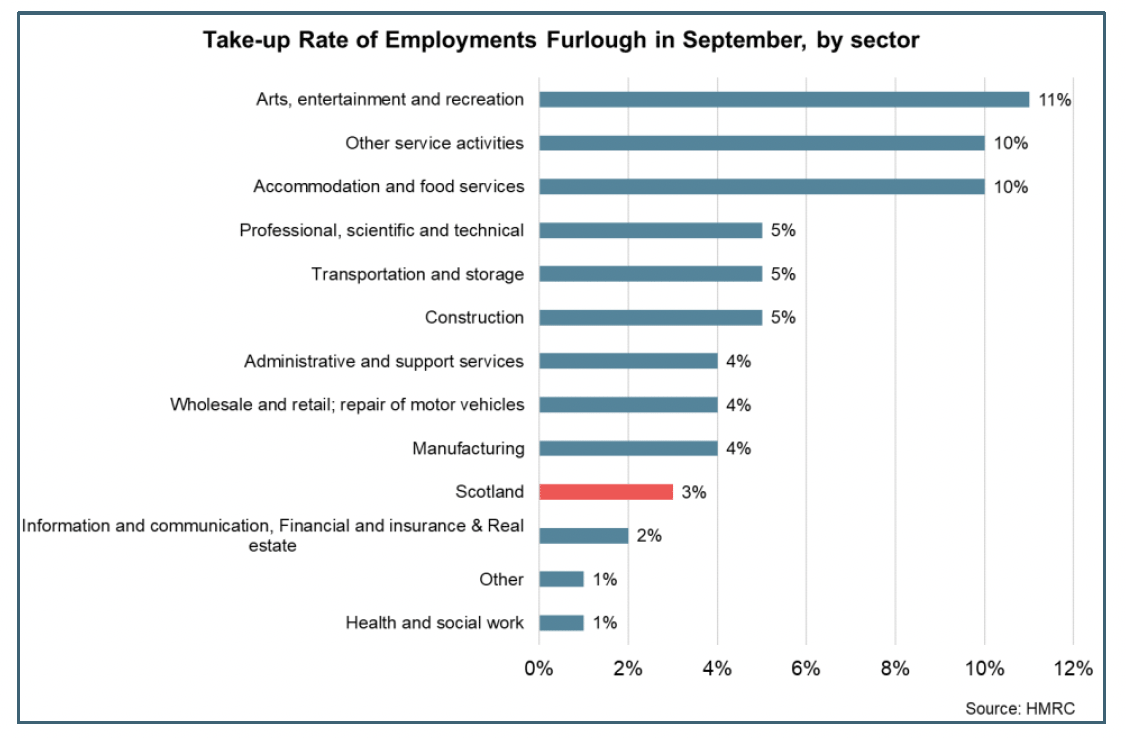

Furthermore, in September there remained widespread use of the furlough scheme across sectors, however the highest take up rates remained in consumer facing services such as arts, entertainment and recreation (11%) and accommodation and food services (10%), reflecting the uncertainty that these sectors are continuing to face at this stage of recovery around the capcity at which they are trading and their staffing requirements.

Flash estimates of PAYE employment data for October signalled an increase in employment levels with the number of payroll employees in Scotland rising by 12,000 over the month and is now 0.1% above its pre-pandemic level.[20] Similarly, Claimant Count data also signalled further improvement in October with the number of claimants of Job Seekers Allowance and Universal Credit (claiming principally for the reason of being unemployed) falling 1.3% to 157,100. The number of claimants is at its lowest level since the start of the pandemic, though remains 43,300 (38.1%) higher than its pre-pandemic level in February 2020 suggesting that there remains pressure in this element of the labour market.[21]

Demand for Staff and Labour Shortages

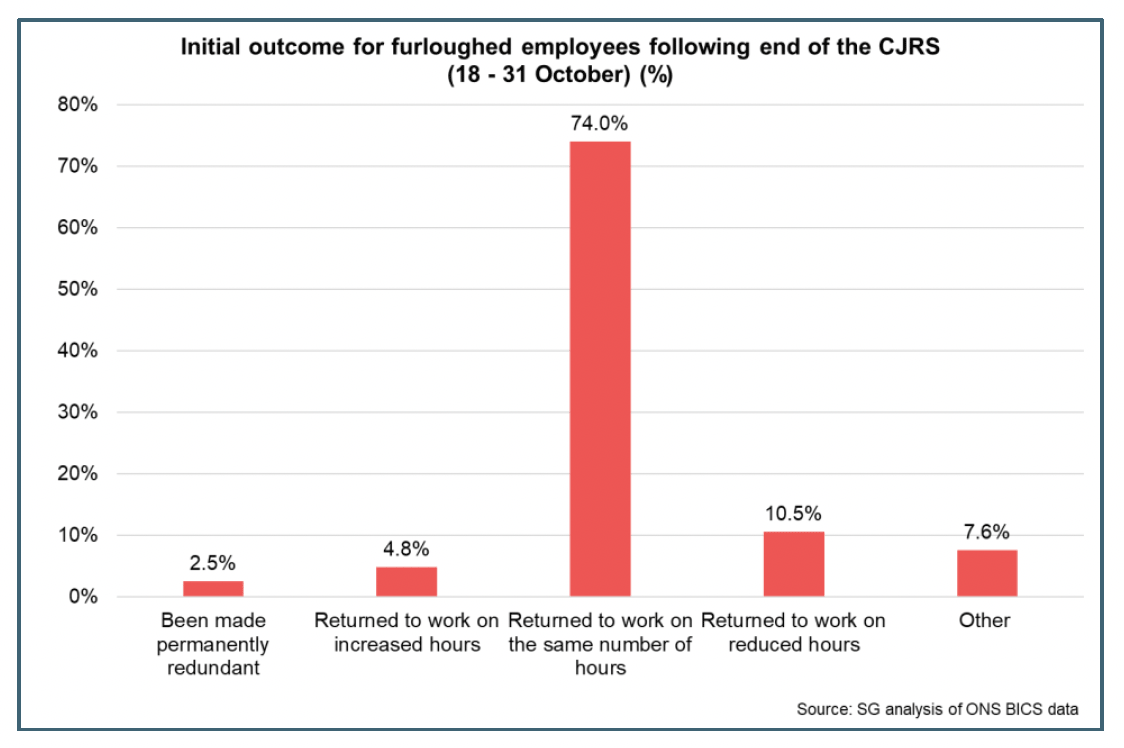

The end of the furlough scheme continues to present an element of uncertainty for the labour market in the near term and the impact this could have on unemployment over the final quarter of the year. BICS data for October estimates that since the end of the furlough scheme, 74% of furloughed workers returned to work on the same number of hours, 10.5% on reduced hours with 2.5% of furloughed workers being permanently made redundant.[22] At a UK level, analysis by the Resolution Foundation found that 88% of employees who were furloughed in September were working in October.[23]

The Scottish Fiscal Commission forecast that unemployment will rise slightly at the end of the year to 5.4% reflecting that some people on furlough in September may be made redundant, while there may also be an increase in labour market participation with restrictions largely removed.[24]

To date, the return to work of furloughed staff over the course of the year and the rebound in the number of payrolled employees reflects the strong increase in demand for staff and recruitment activity as restrictions have eased and economic activity has strengthened.

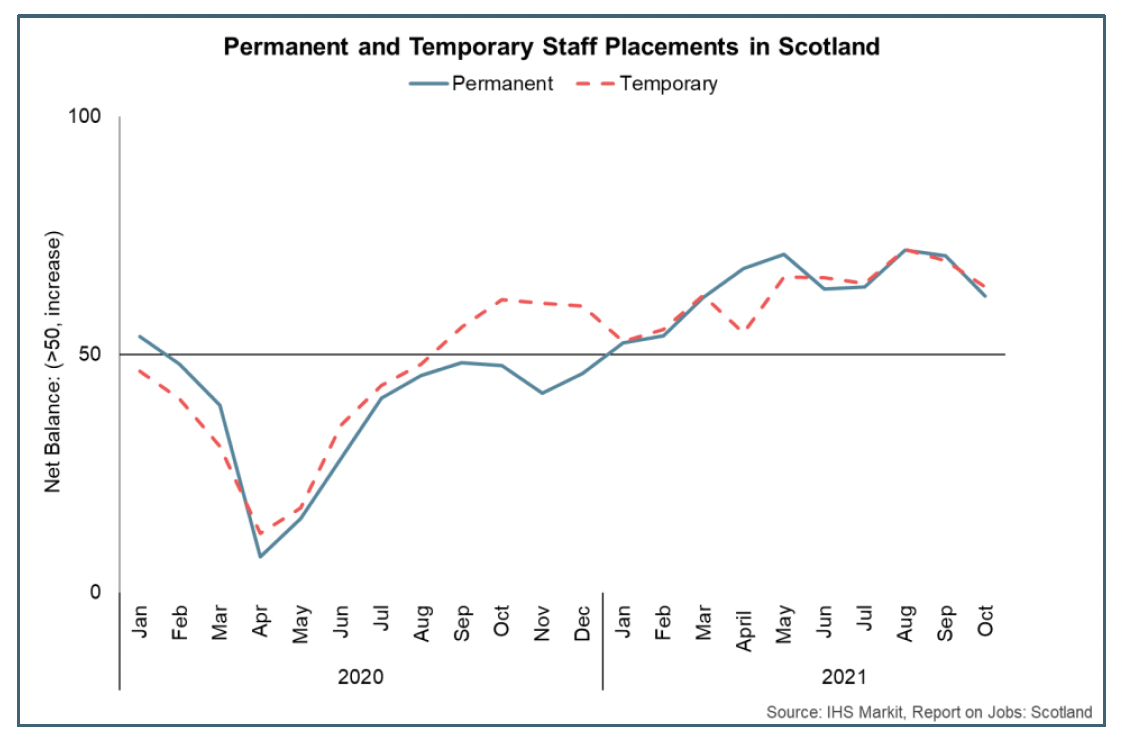

The November RBS Report on Jobs for Scotland signalled that permanent and temporary staff placements continued to grow robustly with net balances of 62.4 and 64.2 respectively, though the pace of growth had slowed slightly from the more rapid rates of growth over the second and third quarters.[25]

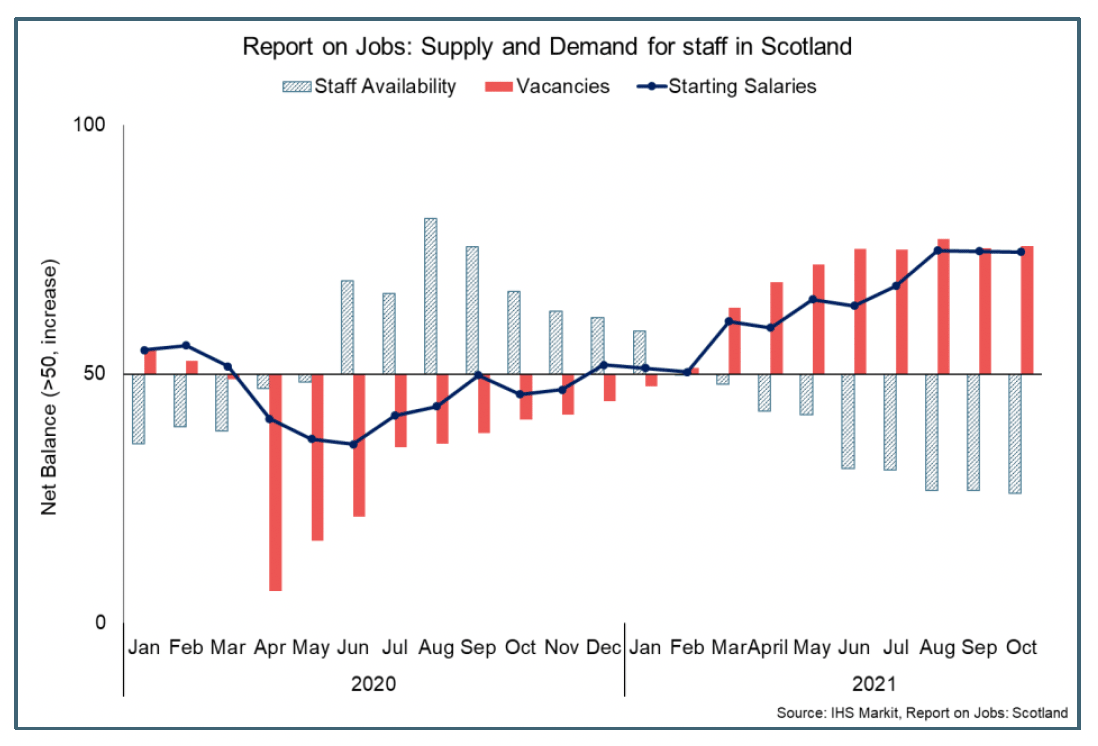

Despite the slight slowing of placements in October, demand for permanent and temporary staff remained heightened with vacancy rate net balances remaining close to their record high in August. Furthermore, ONS Adzuna data shows that during the third quarter of the year, online job vacancies in Scotland have been on average 27% higher than pre-pandemic levels, rising to an average of 37% higher in October and into November.[26] However, staff/candidate availability continued to fall in October, which businesses attributed to the effects of the pandemic, EU Exit and the overall strong demand for staff, and has resulted in recruitment challenges intensifying in recent months.

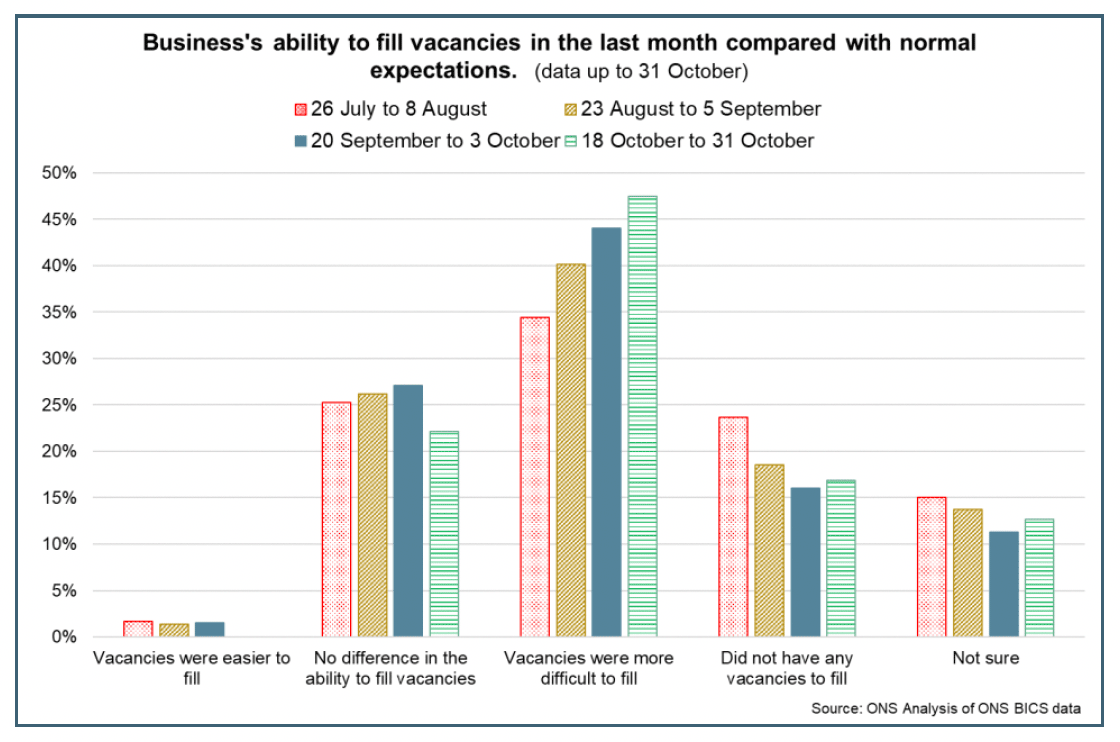

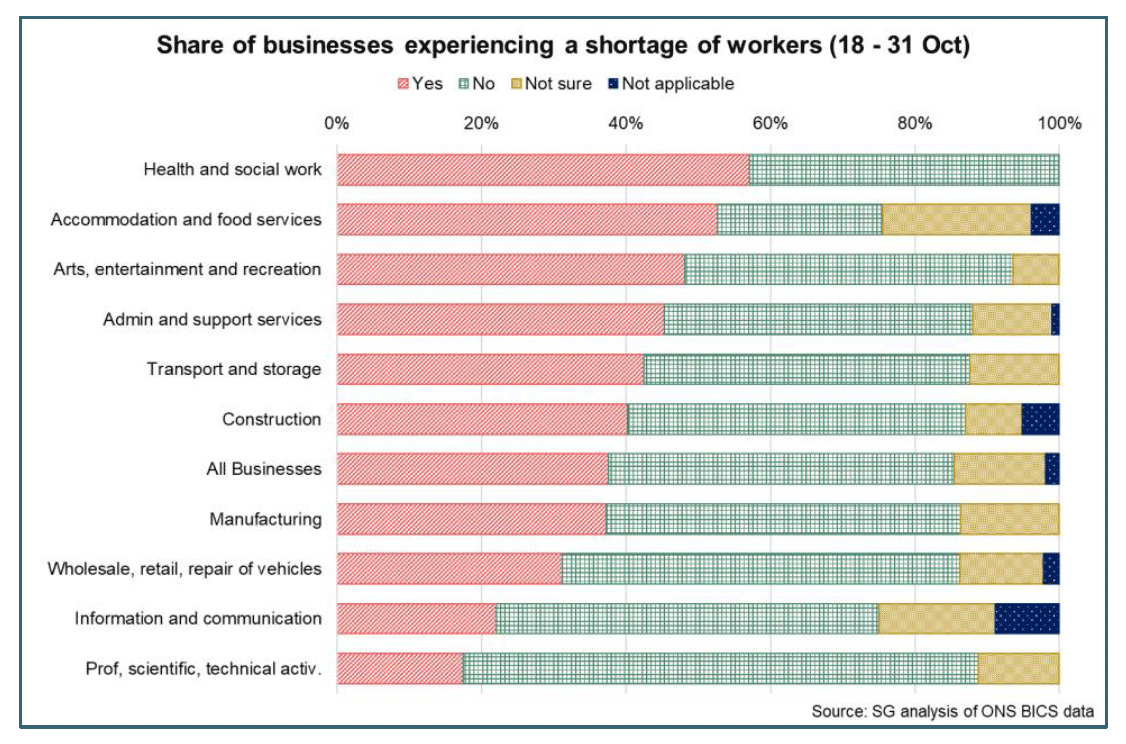

Furthermore, latest BICS data show that at the end of October, the proportion of businesses that did not have any vacancies to fill had fallen from 24% at the start of the third quarter to 17% in October, while the proportion of businesses finding vacancies more difficult to fill had increased from 34% to 47% over the same period.[27]

Overall, the imbalance between demand and supply of staff has resulted in labour shortages affecting sectors including haulage, construction, tourism, hospitality and food & drink.

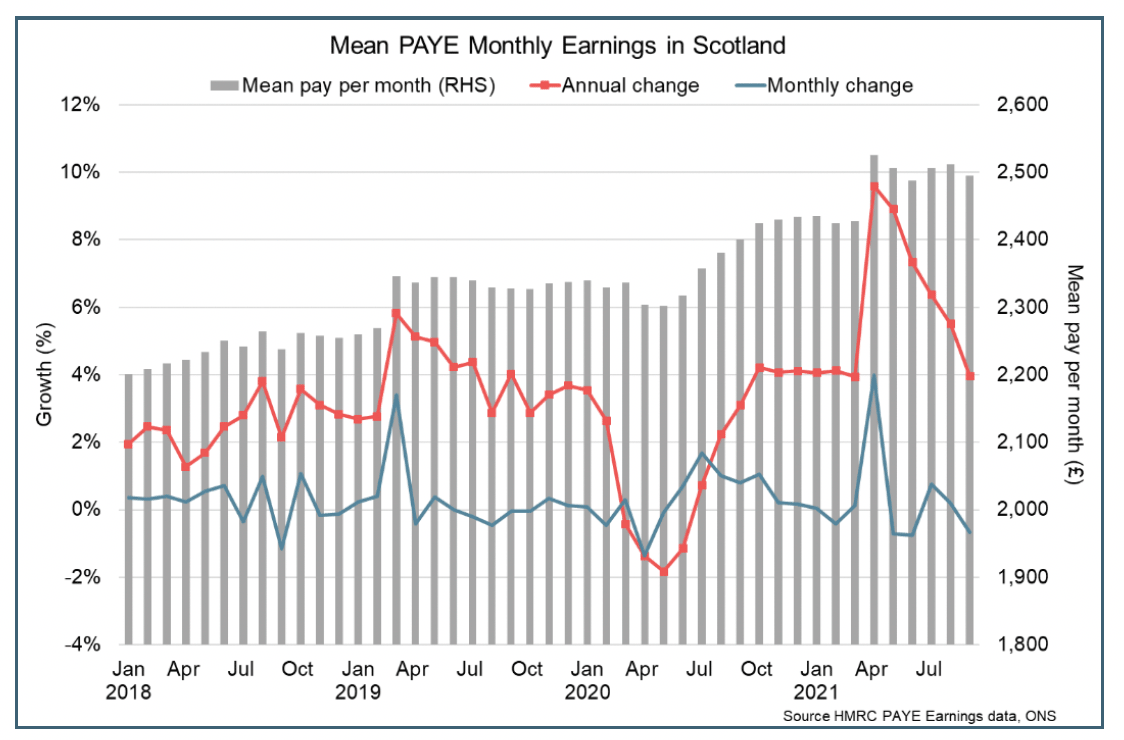

The imbalance also presents upward pressure on earnings. At an aggregate level, mean PAYE monthly pay fell sharply at the start of the pandemic, however strengthened over the course of 2020 and rebounded back above its pre-pandemic level in July 2020. Relatively robust earnings growth over this period in part reflects the lower inflows of new employees, for which mean pay tends to be around 40% lower than for those continuously employed meaning inflows into payrolled employment tend to bring down average pay and average pay growth. Latest data shows mean pay per month in Scotland fell 0.7% in September to £2,495, with annual growth slowing to 4.0%.[28]

In general, the rate of earnings growth over this period needs to be interpreted with caution over this period as base effects, compositional factors which reflect a fall in the number and proportion of lower-paid employee jobs, and the furlough scheme have all influenced the data.

Looking ahead, the recruitment challenges that have emerged, has created upward pressure on starting salaries in the near term for both permanent and temporary staff positions. The latest RBS Report on Jobs reported that the permanent starting salaries index remained close to its series high in October (74.8) while temporary wages (70.7) had eased back slightly from August and September.[29]

Box B: Bottlenecks in Supply Chains and the Labour Market

Demand across the global economy has rebounded sharply as restrictions on activity have been removed over the course of 2021. However, the impacts of the pandemic on the supply side of the economy has meant that resource availability and international supply chains have not readjusted and rebounded as quickly, leading to significant bottlenecks in supply chains.

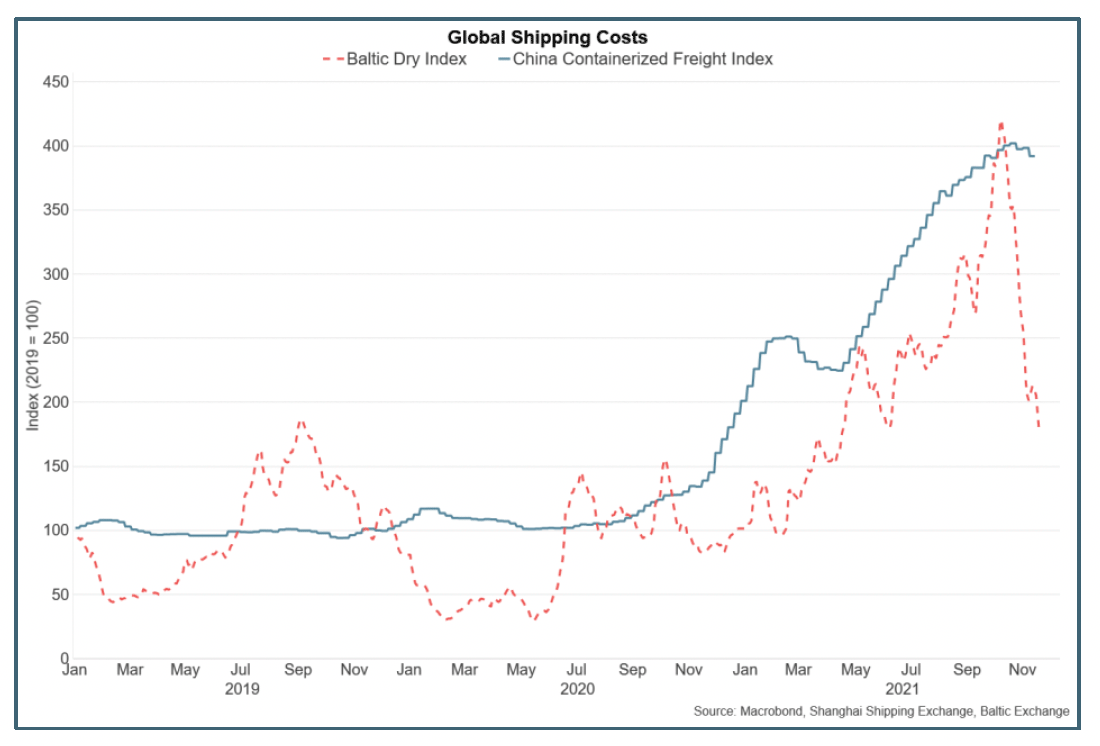

As a result, costs of many materials and goods have increased, as has the cost of transporting them across supply chains. Global shipping costs have increased sharply over the past year in response to the strong demand for goods, ongoing disruption from the pandemic impacting supply chain capacity and temporary disruptions such as the blockage of the Suez Canal. Shipping price indices have more than doubled over the past year and remain elevated in November, however recent data suggest that the pace of growth has moderated over the past month.

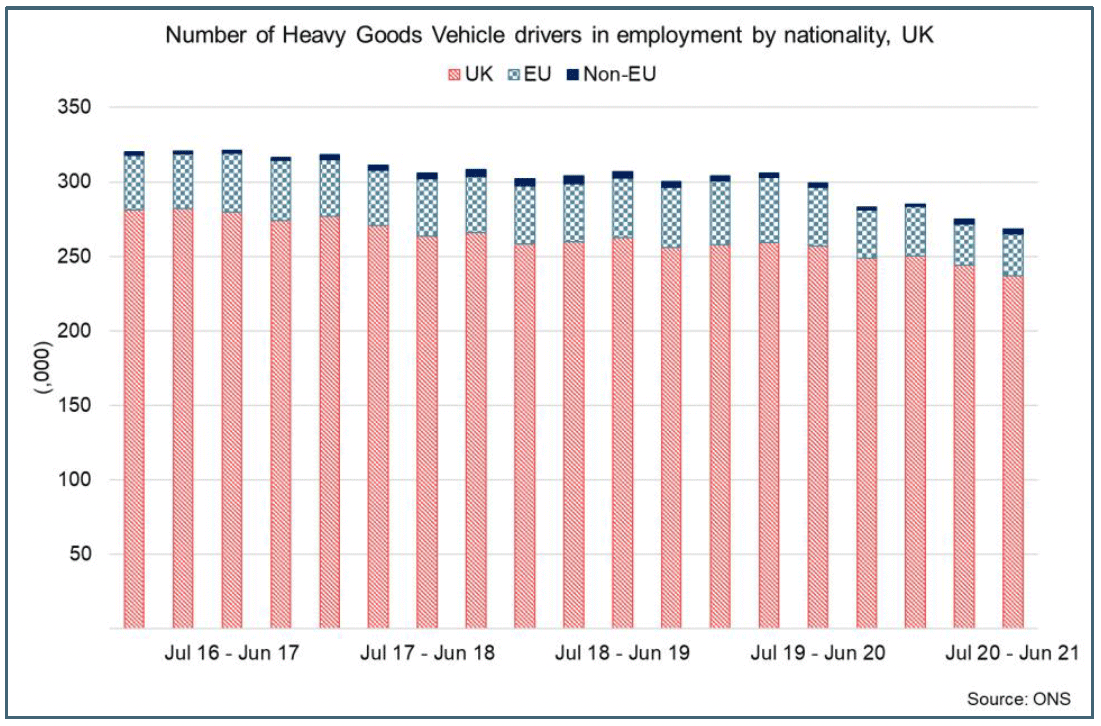

Supply disruption in the UK partly reflects the global issues, however domestic factors are also impacting. For example, a shortage of HGV drivers has emerged across a range of countries including the UK. This in part reflects longstanding recruitment challenges in the haulage sector. At the UK level, there has been a general downward trend in the total number of HGV drivers in employment with 15% (42,000) fewer UK nationals working as HGV drivers than there were four years earlier.[30]

However, the largest decrease was during the pandemic with 26,000 (-10%) fewer UK nationals employed as HGV drivers in the year ending June 2021 than in June 2019. This has been exacerbated by a fall in EU nationals working as HGV drivers over the same period and delays due to COVID regulations which have stalled the number of newly qualified drivers gaining certification.

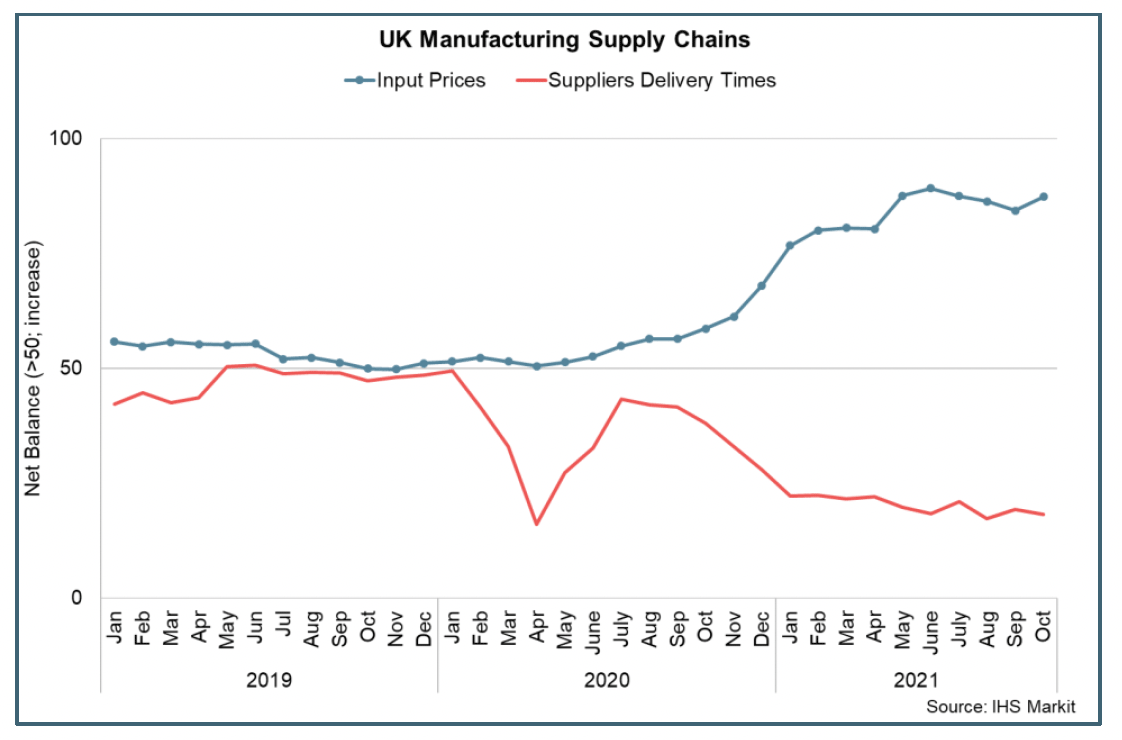

Combined, the impacts of global and domestic supply chain disruption remains elevated in the UK with many industries reporting both a deterioration in the availability of materials and supplier delivery times coupled with a corresponding rise in input prices. UK PMI data for the manufacturing sector shows that suppliers delivery times have weakened to their lowest levels in the time series, while input price inflation remains close to its highest level.[31]

Bottlenecks across supply chains and shortages in certain parts of the labour market are expected to be temporary as the demand and supply side of the economy rebalance following the significant shocks to activity during the pandemic to date. However, they are currently weighing on activity and output in a range of sectors including manufacturing, construction and parts of the services sector during the third quarter of the year and continue to contribute significantly to the current rise in inflationary pressures.

Contact

Email: OCEABusiness@gov.scot

There is a problem

Thanks for your feedback