New Build Heat Standard 2024: business and regulatory impact assessment

Business and regulatory impact assessment (BRIA) in consideration of the introduction of the New Build Heat Standard (NBHS). Looking in detail at the economic impacts of moving to Zero Direct Emissions heating systems in all new buildings.

This document is part of a collection

19. Annex

19.1 Consultation: Local Authorities

168. Please note that, in some cases, responses from local authorities only represented certain voices from the local authority council, such as those responsible for building standards or housing.

| Local Authority |

Part I |

Part II |

Overall |

|---|---|---|---|

| Aberdeen City |

No |

No |

No |

| Aberdeenshire |

No |

Yes |

Yes |

| Angus |

No |

No |

No |

| Argyll and Bute |

No |

No |

No |

| City of Edinburgh |

Yes |

No |

Yes |

| Clackmannanshire |

No |

No |

No |

| Dumfries and Galloway |

Yes |

No |

Yes |

| Dundee City |

No |

No |

No |

| East Ayrshire |

Yes |

No |

Yes |

| East Dunbartonshire |

Yes |

No |

Yes |

| East Lothian |

No |

Yes |

Yes |

| East Renfrewshire |

No |

No |

No |

| Falkirk |

No |

Yes |

Yes |

| Fife |

No |

Yes |

Yes |

| Glasgow City |

Yes |

No |

Yes |

| Highland |

No |

No |

No |

| Inverclyde |

No |

No |

No |

| Midlothian |

No |

No |

No |

| Moray |

No |

No |

No |

| Na h-Eileanan Siar |

No |

No |

No |

| North Ayrshire |

Yes |

No |

Yes |

| North Lanarkshire |

Yes |

Yes |

Yes |

| Orkney Islands |

No |

No |

No |

| Perth and Kinross |

Yes |

Yes |

Yes |

| Renfrewshire |

No |

No |

No |

| Scottish Borders |

Yes |

No |

Yes |

| Shetland Islands |

No |

Yes |

Yes |

| South Ayrshire |

No |

No |

No |

| South Lanarkshire |

Yes |

No |

Yes |

| Stirling |

No |

No |

No |

| West Dunbartonshire |

No |

Yes |

Yes |

| West Lothian |

No |

No |

No |

| Number that responded |

10 |

8 |

16 |

19.2 Scottish Firms Impact Test

169. This section details the questions put to businesses in the one-to-one discussions held as part of the Scottish Firms Impact Test. In total, 14 questions were prepared in advance of discussions. These are given below.

- The Scottish Government is currently consulting on prohibiting the use of DEH systems in new buildings from 1 April 2024 onwards through our New Build Heat Standard (NBHS). Are you supportive of the introduction of the NBHS? Why / why not? Please give your reasons.

- In your opinion, how has the use of DEH systems (such as fossil fuel boilers, etc.) changed over recent years (e.g., in the last 5 years)?

- How would you expect the use of these items to change in the next 5-10 years in the absence of the NBHS being introduced?

- In your opinion, what will the biggest potential impacts be (both costs and benefits) of introducing the NBHS on your business or on those which you represent? Which businesses, in your opinion, will be most affected by the regulations? Please provide evidence where possible.

- What technologies do you expect to replace DEH systems in new builds?

- Has your business or have the businesses you represent taken any steps to mitigate any anticipated impacts or costs associated with the NBHS? If so, please expand your answer.

- Does your organisation or association have specific comments on how the NBHS might impact businesses in more remote areas of Scotland? Please expand on your answer.

- To what extent do you expect the NBHS to put your business, or those which you represent, at an advantage or disadvantage, nationally or internationally? Please provide evidence where possible.

- Do you have any comments on the NBHS affecting competition amongst your suppliers, or those of the businesses which you represent? If so, could you elaborate?

- When the NBHS comes into force, will your business switch to alternative zero direct emissions heating (ZDEH) systems, or do you anticipate stopping the use, sale, or production of the DEH systems altogether? Please expand your answer.

- If your business will be substituting DEH with ZDEH alternatives (as part of your sales or production), how quickly do you expect this transition to take place? Do you anticipate any opportunities or difficulties prior to or during this transition? Please expand your answer.

- Are there any unintended consequences you may anticipate for your business or the businesses you represent as a result of the NBHS?

- Do you envisage any increase in costs relating to the use of ZDEH systems would be passed onto buyers, or would your organisation expect to absorb costs these costs?

- Do you envisage the introduction of the NBHS having any impact on the supply of housing across Scotland?

19.3 Costs and Benefits

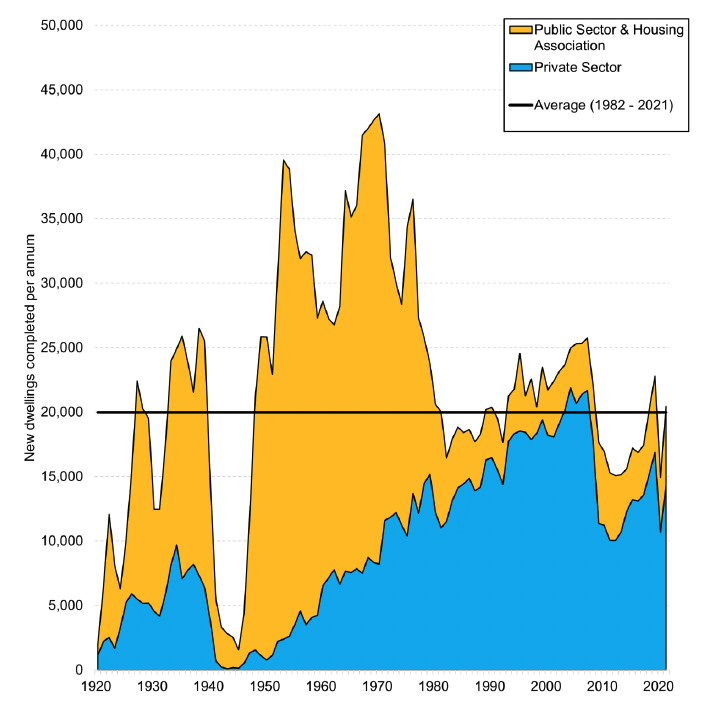

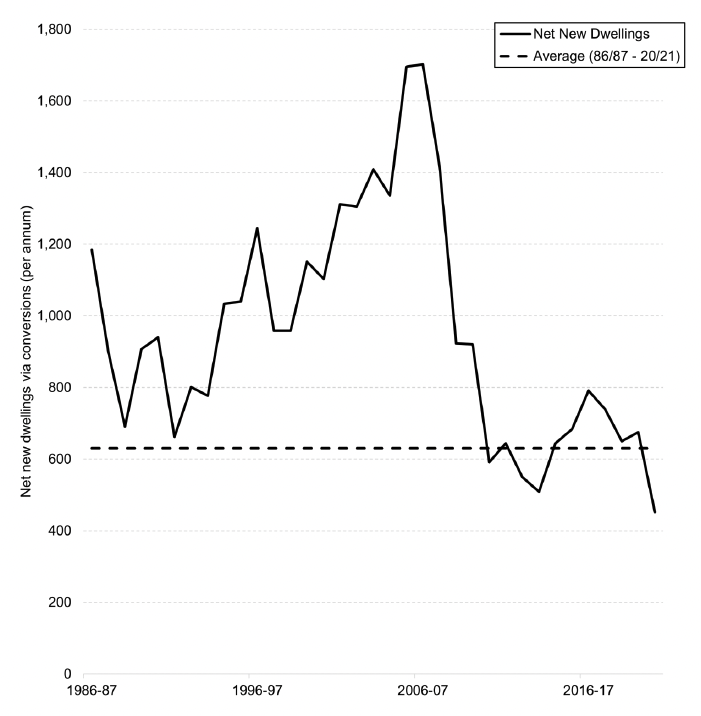

170. Over the last 60 years (1962-2021), over 1,450,000 homes were completed in Scotland.[135] The domestic side of the assessment assumes 19,975 new-build homes are completed each year, with a further 630 net conversions being added to the domestic stock annually. These annual additions are based on the averages observed for 1982 to 2021 and 1986/87 to 2020/21, respectively, with this being shown in Figure 8 and Figure 9 below. In the early years of the standard coming into force, a build-out parameter is assumed to capture the effect of time-lags between a building warrant being granted and a completion certificate being accepted.[136] In total, approximately 1,235,000 new homes are added to the domestic stock over the period of the assessment, with 1,195,000 of these assumed to be subject to the NBHS (after accounting for the lag in build-out in the initial few years).

Notes: Sourced from Scottish Government, accessed 10/11/2022.[137] Average for 1982 to 2021 is approximately 19,975 new dwellings per annum.

Notes: Sourced from Scottish Government, accessed 10/11/2022.[138] Average for 1986/87 to 2020/21 is approximately 630 net new dwellings per annum.

171. Under our central approach to modelling domestic new-builds, we use data on EPCs for new dwellings where the date of assessment took place in 2022.[139] From this data, we construct a 2 x 3 matrix containing the share of new-builds that fall into each technology (ZDEH, DEH) and Energy Efficiency Rating (EER) band (A, B, C) grouping. The share using ZDEH technologies is assumed to be around 21% in 2022. In the absence of the NBHS being adopted, it is assumed that this share would naturally grow to 100% by 2037, with this assumption being based on the growth in the share observed for 2014 through 2022 from EPC outturn data.

172. We also obtain the median floor area for each EER band (A-C), conditional on the property using a DEH system, and combine this with metered gas consumption statistics for new-builds published by BEIS to obtain gas consumption for each EER band A to C.[140], [141] This is then used alongside an assumed gas boiler efficiency of 89.5%[142] to obtain the heat demand of the property.

173. We assume all DEH-using properties will use mains gas as their fuel in the counterfactual. For comparison, analysis of the EPCs assessed between 2018 and 2022 finds that around 2.5% used oil or LPG, and 0.2% used biomass as their main fuel type. This assumption is deemed to be insignificant, but ultimately plausible as building standards tighten in the future, making oil/LPG adoption in new-builds increasingly unrealistic.

174. It is important to point out that our reliance on the BEIS metered gas consumption statistics is a potential limitation of the analysis. The data is for English and Welsh new-builds which recorded an EPC since the start of 2014, with the consumption data pertaining to the year 2017. This may lead to us overstating the benefits of the policy intervention if Scottish new-build gas consumption would be lower than this amount (and hence the carbon savings lower). This could, for example, be plausible as a result of more stringent building standards. On the other hand, we argue that the use of metered consumption data is preferable to Standard Assessment Procedure (SAP) estimates of fuel consumption as these can suffer from what has come to be known as the "energy performance gap." This is the gap between modelled fuel consumption versus actual fuel consumption.[143], [144] As such, use of the BEIS metered fuel consumption data under central assumptions is deemed preferable.

175. It is also important to note that fuel poverty estimates are based on the modelled energy use required for a household to meet a satisfactory heating regime and not based on actual household consumption. The Scottish statutory definition of fuel poverty is set out in the Fuel Poverty (Targets, Definition and Strategy) (Scotland) Act 2019, while statutory heating regimes are set out in out in the Fuel Poverty (Enhanced Heating) (Scotland) Regulations 2020. As the analysis in this report is based on actual metered consumption and not the energy required to meet a households statutory heating regime, energy use figures and costs quoted will not reflect fuel poverty estimates.

176. Information on the technological assumptions made in the domestic side of the assessment is available in Table 6 below, with these assumptions being based on evidence from a variety of sources.

| Technology |

Cost (£) |

Lifetime (years)[145] |

Efficiency (%)[146], [147] |

|---|---|---|---|

| Gas boiler |

6,723 (4,670) [NA] |

15 |

89.5 |

| Air-to-water heat pump |

15,148 (7,368) [7,973] |

20 |

300.0 |

| Electric |

4,757 (4,648) [6,205] |

15 |

100.0 |

Notes: Figures outside of parentheses and brackets are the capex for an installation in a virgin new-build, whereas figures in parentheses are repex, and figures in brackets are retrofit costs. Capex for virgin installations are discounted by 10% in line with research on new-build installation costs.[148] Capex of heat pump installations falls by 20% by 2030, bringing capex to just over £12,100 from 2030 onward.[149] Repex and retrofit costs above already include this assumed reduction. All costs converted to 2021 base year prices using CPIH 05.3.1.4 "Heaters, air conditioners" information.[150]

177. The capex for the gas boiler pulls on research for BEIS[151] and comprises the following: (a) a high-end 18 kW non-combi boiler, (b) a highly insulated unvented cylinder, (c) cost of fittings for a new installation, and (d) a labour fee for installation in an unoccupied / easy-access building. The sum of the above costs is then multiplied by the cost multiplier associated with using a regional installer, and then the cost of digital controls and a large heat distribution system is added to the result. The total cost is inflated from 2017 to 2021 prices, then reduced by 10% in line with research on new-build installation costs.[152] The repex includes (a), (b), the cost of standard fittings (not fittings for a new installation), and a standard labour fee (as opposed to one for an unoccupied / easy-access building). Again, the sum is multiplied by the regional installer cost multiplier and inflated to 2021 prices.

178. The capex for the air-to-water heat pump at the beginning of the assessment pulls on the same BEIS research and comprises the following: (a) a mid-range 6 kW heat pump, (b) a central estimate of the cost of fittings, (c) a medium-sized buffer tank with a highly insulated unvented water cylinder, (d) high-end controls, (e) labour fee associated with a simple installation, and (f) the cost of a heat distribution system for a 3-bed home (underfloor downstairs, radiators upstairs). The sum of (a) through (f) is then inflated to 2021 prices and reduced by 10% in line with research on new-build installation costs.[153] Over time, this capex is reduced by a further 20% by 2030 in line with the same research previously referenced.

179. The repex for the heat pump comprises (a) and (c), as well as a low estimate of the cost of fittings (as some of the old system's components can be reused) and the cost of labour for a standard installation. Since the first like-for-like heat pump replacement does not occur until 2044 in the assessment, we build the "20% by 2030" cost reduction into the repex estimate. The retrofit cost comprises (a), a low estimate of the cost of fittings, a low estimate for the cost of a buffer tank and water cylinder, a low estimate of the cost of controls, a central estimate of the cost of labour, and a high estimate of the cost of replacing radiators. The first retrofit does not occur until 2039 in the assessment, so we build the "20% by 2030" cost reduction into the retrofit cost estimate. As with treatment of prior heating system costs, these repex and retrofit costs are expressed in 2021 prices.

180. The capex for the electric heating system pulls on the same BEIS research and comprises the following: (a) a mid-range 7 kW High Heat Retention (HHR) storage heating system, (b) standard controls, (c) new circuit board and breaker, and (d) 1-day installation labour fee. The sum of these is inflated to 2021 prices and reduced by 10% in line with treatment of other virgin installation costs.

181. The repex for the electric heating system comprises (a), as well as a central estimate of the cost of disposing of old units and half a day for installation labour fees. The retrofit cost comprises (a), as well as the cost of basic controls, a high estimate of disposal costs, replacement of circuit board, and 2 days of installation labour fees. These are converted to 2021 prices.

182. Build-out rates for the non-domestic sector use information provided by Scottish & Southern Electricity Networks (SSEN) as part of their Distribution Future Energy Scenarios (DFES) for the Scottish Hydro Electric Power Distribution (SHEPD) licence area.[154] These are then extrapolated based on the current ratio of SHEPD to Scottish Power Transmission (SPT) customers to inform non-domestic build-out rates for southern Scotland. Information on the average floor area of new-build non-domestic properties from the Non-Domestic National Energy Efficiency Data-Framework (ND-NEED) is then used to calculate an average number of non-domestic buildings constructed over the time horizon of the appraisal.[155] In total, over 50,000 non-domestic buildings are added between 2024 and 2083, with around 40,000 being subject to the NBHS.

183. Information on the technological assumptions made in the non-domestic side of the assessment is available in Table 7 below, with these assumptions predominantly being based on assumptions made by the CCC in their Sixth Carbon Budget which were informed by research carried out by BEIS.[156], [157]

| Technology |

Cost (£/kW) |

Lifetime (years) |

Efficiency (%) |

Size (kW)[159] |

|---|---|---|---|---|

| Gas boiler |

231 (5) |

15 |

89.5 |

300 |

| Air-to-water heat pump |

1,333 (5) |

20 |

283 |

150 |

| Air-to-air heat pump |

697 (9) |

20 |

283 |

150 |

| Electric |

183 (3) |

15 |

100 |

150 |

Notes: Figures outside of parentheses are the capex, and this is also used as the repex due to a lack of evidence for these specific costs. The retrofit cost is assumed to be 7.5% higher than capex in line with research.[160] Figures within parentheses represent opex, excluding fuel costs. Capex for virgin installations are not discounted by 10% due to a lack of an evidence base for this assumption in the non-domestic sector. Capex of heat pump installations falls by 20% by 2030, bringing capex to just over £1,066/kW from 2030 onwards for air-to-water and £557/kW for air-to-air. This feeds through to repex and retrofit costs. All costs converted to 2021 base year prices using CPIH 05.3.1.4 "Heaters, air conditioners" information.[161]

19.4 Sensitivity Analysis

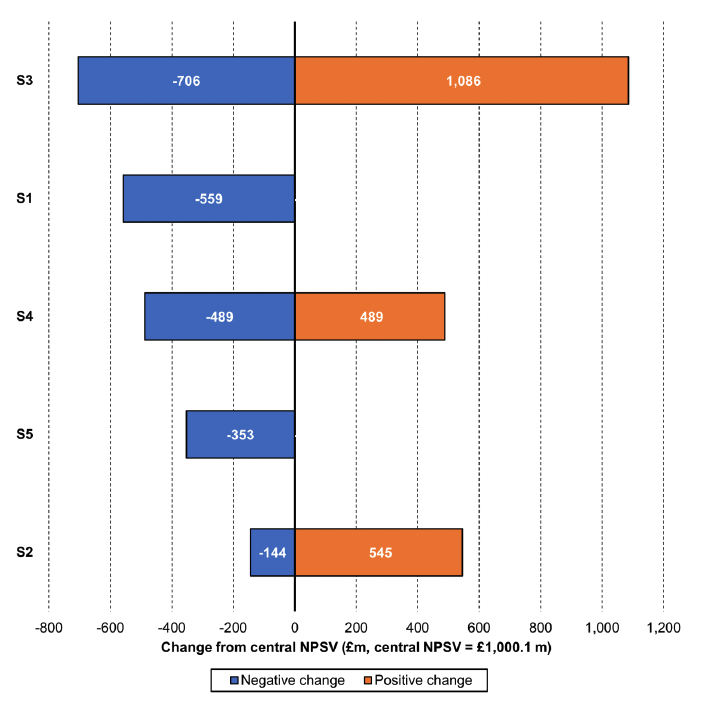

184. This section explores the sensitivity of our NPSV estimate, using the scenario B gas LRVCs NPSV. Sensitivities investigated are discussed below, alongside their effect on the NPSV, shown in Figure 10.

185. S1: Air-to-water heat pumps in the non-domestic sector. This sensitivity check has a large negative impact on the NPSV of the standard. Under our central set of assumptions, new-builds in the non-domestic sector are assumed to adopt air-to-air heat pumps on the grounds of (i) their lower capital costs and (ii) evidence that suggests the need for cooling capability (which air-to-air heat pumps can provide) is higher in the non-domestic sector.[162] Since the cost of an air-to-water heat pump sits around £1,333/kW compared to that of an air-to-air heat pump of almost £697/kW, assuming that air-to-water heat pumps are installed in new-build non-domestic properties pushes up the capital costs incurred within the non-domestic sector. However, while the NPSV falls, it does not become negative. In reality, the technology mix in new-build non-domestic buildings is likely to consist of both air-to-air and air-to-water heat pumps, alongside other ZDEH options such as heat networks and electric heating systems.

186. S2: Scenarios A and D for gas LRVCs. BEIS guidance recommends testing the sensitivity of the results using the A and D scenarios for the LRVCs of gas. Relative to the scenario B NPSV, A reduces the NPSV by almost £150 mn. On the other hand, scenario D is an additional scenario which assumes that high gas prices will remain constant in the long run. Under such a scenario, and using central electricity LRVCs, the NPSV increases relative to our central estimate by almost £550 million.

187. S3: Pessimism and optimism. In order to check the effect a set of pessimistic assumptions has on our results, we assume low LRVCs for gas (scenario A), high LRVCs for electricity, and low carbon values.[163] Under optimistic assumptions, we assume high LRVCs for gas (scenario D), low LRVCs for electricity, and high carbon values. Under the set of pessimistic assumptions, the NPSV retains its sign and remains positive. This set of assumptions has the largest negative effect across the scenarios considered as part of this sensitivity analysis. Under more optimistic assumptions, the NPSV more than doubles (giving us the largest positive effect as part of this sensitivity analysis).

188. S4: Carbon values. We check the sensitivity of the results to using low and high carbon values and find that the NPSV remains positive.

189. S5: Electric heating in both sectors. Our central set of assumptions assumes heat pumps are adopted as the main technology in both the domestic and non-domestic sectors. This sensitivity check assumes direct electric heating is adopted. As is shown in Figure 10, this assumption has a negative impact on the NPSV. However, it still remains positive, suggesting a net benefit for social welfare.

Contact

Email: 2024heatstandard@gov.scot

There is a problem

Thanks for your feedback