Local Government 2022-23 Provisional Outturn and 2023-24 Budget Estimates

This publication summarises the 2022-23 provisional outturn and 2023-24 budget estimates for revenue and capital services provided by Scottish local authorities.

This document is part of a collection

Capital Expenditure

Capital expenditure is expenditure that creates an asset, extends the life of an asset or increases the value of an asset. It creates the buildings and infrastructure necessary to provide services, such as schools, care homes, flood defences, roads, vehicles, plant and machinery. Capital expenditure also includes grants a local authority provides to a third party to fund capital expenditure of the third party; direct expenditure on a third party's assets; and loans to third parties to support capital investment of the third party where this is financed from capital resources. Capital POBE figures include amounts relating to a local authority's direct provision of housing, which is recorded in the Housing Revenue Account (HRA).

It is important to note that the 'lumpy' nature of capital expenditure means that delays or changes to large capital projects at the end of the financial year can have a large impact on final figures compared to provisional outturn and budgets.

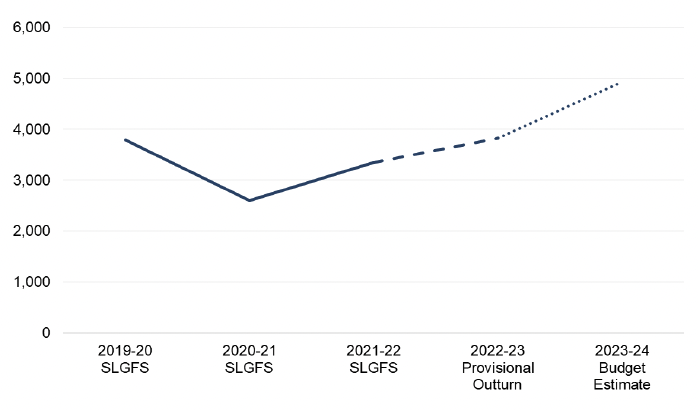

For capital expenditure, local authorities have reported total provisional outturn of £3,825 million in 2022-23, and budget estimates of £4,927 million for 2023-24.

Source: POBE 2023 Return, LFR CR, CR Final

Around £450 million of the notable decrease in capital expenditure between 2019-20 and 2020-21 relates to significant, one-off transactions incurred by Glasgow City Council for Culture & Related Services in 2019-20. The remaining decrease likely relates to the impacts of the COVID-19 pandemic on the building sector in 2020-21.

Capital expenditure is expected to increase significantly in both 2022-23 and 2023-24, reflecting the resumption of delayed capital projects following the easing of COVID-19 restrictions combined with new capital investment programmes starting.

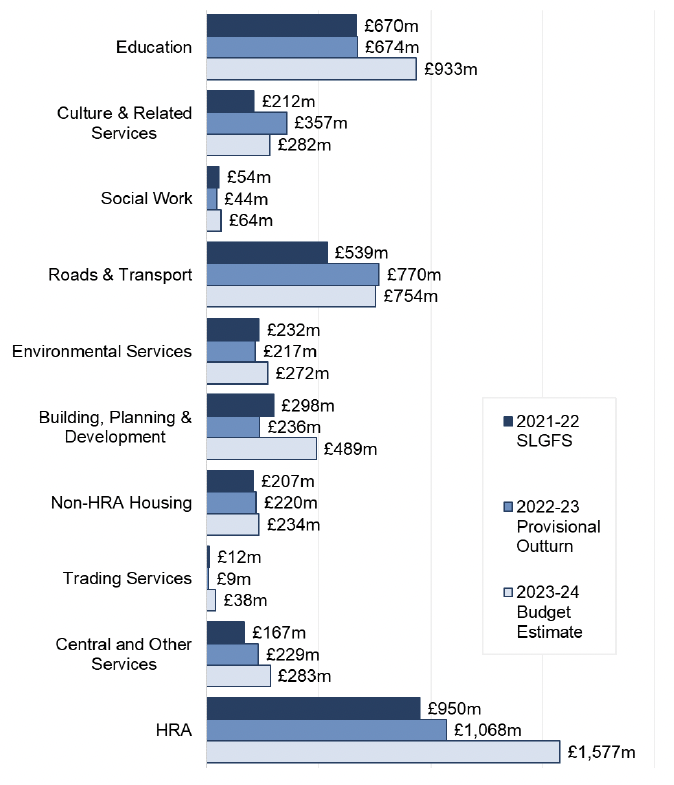

As shown in Figure 5, most services show increases in capital expenditure in 2022-23 and 2023-24, compared to 2021-22. The HRA is the service with the largest capital expenditure in each year, and this is provisionally reported to increase to £1,068 million in 2022-23, and to £1,577 million in 2023-24. This increase is driven by expenditure on new construction and conversion, which accounts for 45 and 55 per cent of the increased expenditure in 2022-23 and 2023-24 respectively.

Please note that 'Non-HRA Housing' includes capital expenditure related to Consented and Statutory Borrowing.

Source: POBE 2023 Return, LFR CR, CR Final

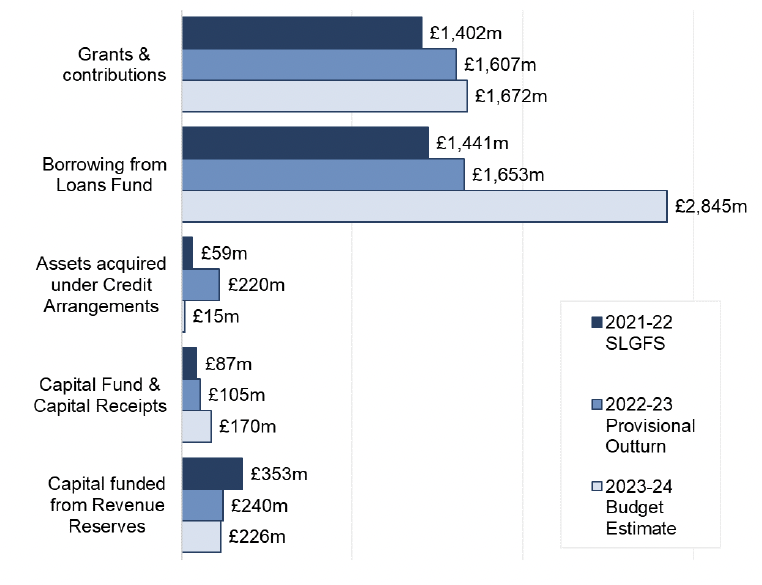

Local authorities can finance capital expenditure in a number of ways, including use of grants and contributions; borrowing; credit arrangements; capital receipts and reserves. Figure 6 shows how capital expenditure was financed in 2021-22 and how it is anticipated to be financed in 2022-23 and 2023-24.

Please note that 'Grants & Contributions' and 'Borrowing from Loans Fund' include amounts used to fund grants to third party capital projects which will also be included in the revenue figures.

Source: POBE 2023 Return, LFR CR, CR Final

Borrowing and Grants & Contributions roughly equal each other for 2021-22 and 2022-23 (at approximately £1,400 million and £1,600 million respectively). However, borrowing is the largest source of capital financing in 2023-24, increasing to £2,845 million respectively. This increase in borrowing is seen across most local authorities in 2023-24 and is due to a combination of planned capital investment and reallocation of capital expenditure as a result of the COVID-19 restrictions delaying capital projects in 2020-21.

Grants and contributions represents the second largest source of capital financing, and accounts for £1,672 million in 2023-24. This source of capital financing includes grants and contributions received from the Scottish and UK Governments; other government agencies and Non-Departmental Public Bodies (NDPBs); other local authorities; and private developers. Capital grant from the SG includes capital allocations paid to local authorities as part of the Local Government Finance Settlement. Details of these allocations can be found in the relevant Local Government Finance Circular.

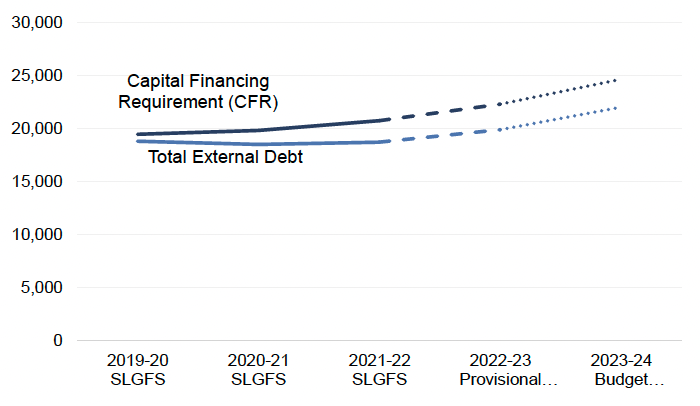

The Chartered Institute of Public Finance and Accountancy (CIPFA) Prudential Code sets out a framework for a local authority to demonstrate its capital investment plans are affordable, prudent and sustainable. The Capital Financing Requirement (CFR) is one of the prudential indicators set out in this framework. It represents the amount of capital expenditure a local authority has determined should be met from borrowing or funded from a credit arrangement, with the repayment of debt met from future budgets. That is, it represents an authority's underlying need to borrow money. Local authorities have reported total provisional CFR of £22,264 million in 2022-23, and total budget estimate for CFR of £24,617 million for 2023-24.

Total External Debtreflects local authorities' gross external borrowing and other long-term liabilities. This may be less than the CFR where an authority has chosen to utilise cash reserves rather than borrow externally; or it may be more than the CFR where an authority has chosen to borrow in advance of capital expenditure being incurred. The Prudential Code limits local authorities' borrowing in advance to the CFR amount plus up to two years planned capital expenditure to be funded from borrowing. Local authorities have reported provisional external debt of £19,857 million in 2022-23, and budgeted for external debt of £21,981 million in 2023-24.

Please note that the treatment of loans to other statutory bodies in the CFR and Total External Debt figures may vary between local authorities for years prior to 2020-21, however this relates to comparatively small values and so it not material.

Source: POBE 2023 Return, LFR CR, CR Final

As shown in Figure 7, Total External Debt continues to remain below the CFR. This means local authorities are under-borrowed and indicates their treasury policy is to utilise cash reserves to fund borrowing at this time. Should their cash requirements increase, a local authority can borrow externally to meet that need, utilising their under-borrowed position.

Contact

Email: lgfstats@gov.scot

There is a problem

Thanks for your feedback