Getting the Right Change – retail strategy for Scotland

This strategy contains current initiatives and future actions to help fulfil our vision for the retail sector in a fair, sustainable way. By delivering on its actions we aim for successful, profitable retail businesses, creation of new, better jobs and to become an exemplar for inclusive growth.

Annex A - Evidence

The annex contains statistics and the analytical context underpinning the strategy.

Sector

Overview of the Sector and Recent Trends

Employment

According to the Business Register and Employment Survey (BRES) 2020, the wholesale and retail sector[15] employed 348,000 people – 13.7% of all employment in Scotland. Of this, 241,000 were employed in the retail sector[16], 9.5% of all employment in Scotland.

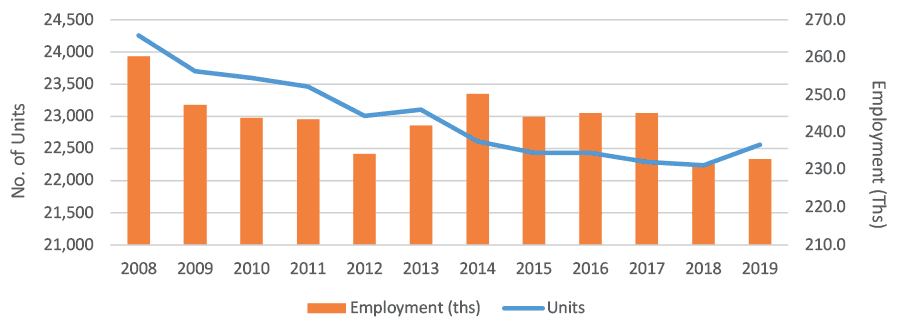

Due to a change of methodology, BRES statistics are not suitable for comparison further back than 2015. However, Scottish Annual Business Statistics 2019 do allow for an analysis of employment trends going back to the financial crisis. Since the financial crash of 2008, retail has gone from a period of expansion to one of contraction, with both the number of outlets and employees falling. Between 2008 and 2012 employment fell by approximately 4% from 243,000 to 234,000, before recovering sharply over the next two years and stabilising in 2016-17 at 5% below 2008 levels. Despite the decline in retail employment since 2008, the sector remains a significant part of our labour market.[17]

Turnover & Gross Value Added

In 2019 retail turnover in Scotland stood at £23.1 billion and the sector contributed £6.1 billion in Gross Value Added (GVA), equivalent to around 6.2% of all Scottish GVA. These totals have remained largely unchanged over the last decade[18] so while the economy as a whole has increased in size by around 10%, retail’s share of GVA has decreased. Scottish Government estimates of monthly GDP show output (GDP) growth of 2.3% growth in wholesale, retail & motor trades from November 2020 to November 2021, and a 1.1% increase from October 2021 to November 2021.[19]

| 2008 (£bn) | 2019 (£bn) | Change (£bn) | |

|---|---|---|---|

| GVA Basic Prices (economy-wide) | 90.7 | 99.5 | 8.8 |

| GVA Retail (47) | 6.2 | 6.1 | -0.1 |

| Retail As A Share | 6.8% | 6.2% |

Scottish Annual Business Statistics (June 2020)

Enterprises

| Sector | Number of Registered Businesses | Micro Registered Businesses (0-9 employees) | Small Registered Businesses (10-49 employees) | Medium-Sized Registered Businesses (50-249 employees) | Large Registered Businesses (250+ employees) |

|---|---|---|---|---|---|

| Retail Trade, (Division 47) | 15,535 | 13,715 | 1,280 | 230 | 305 |

| Predominantly Food Retail (Class 47.11 & Group 47.2) | 4,665 | 4,155 | 450 | 35 | 25 |

| Non-Food/ Other Retail | 10,870 | 9,565 | 830 | 195 | 280 |

In March 2020, 13,790 registered enterprises operated in the Scottish retail sector. This is a rise from 13,715 registered enterprises in the prior year but remains below the 2014 number of businesses which stood at 14,675.[20]

Two thirds (66%) of registered businesses in the retail sector were in the non-food/other retail sub-sector while micro enterprises (0-9 employees) accounted for 87% of businesses in the sector. Large enterprises (250+ employees), which comprised around 2.2% of enterprises, accounted for 69.6% of employment and 76.8% of turnover.

Productivity & Pay

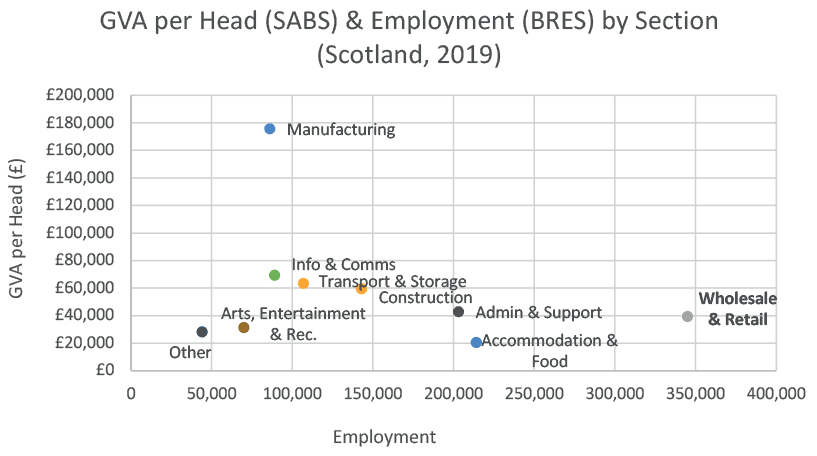

The retail sector is characterised high levels of employment, but also by relatively low productivity and low rates of pay, when compared with other sectors.

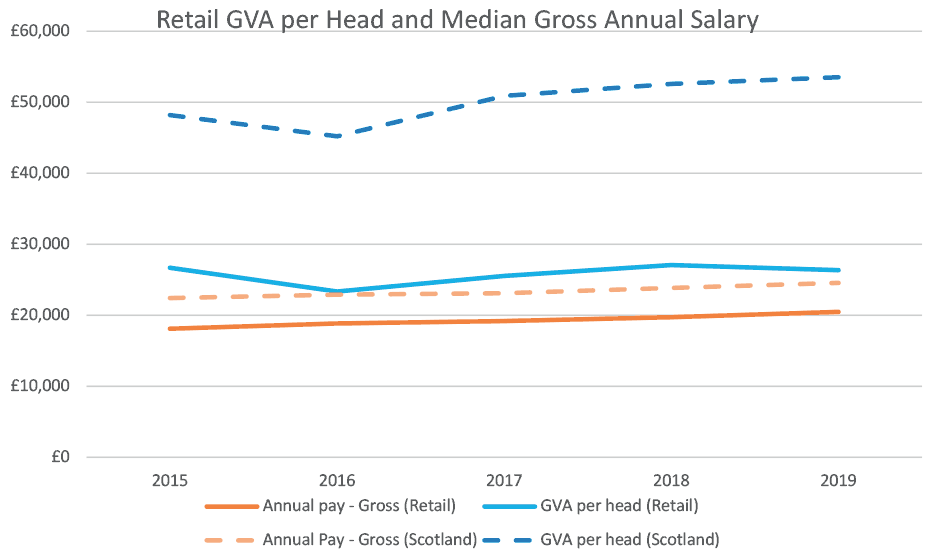

GVA per head (typically used as a proxy for productivity) in the retail sector in 2019 was £26,374, significantly lower than GVA per head across Scotland as a whole (£53,524). GVA per head in wholesale, retail & repair of vehicles as a whole was £39,488 – higher than the retail sector in isolation, but still significantly below the figure across all in industries. Given that the sector is such a significant employer in Scotland, it follows that any improvement to levels of productivity could mean significant benefits.

Productivity is a key driver of wages, and so it follows that pay in the sector is also comparatively low. In 2019, 42.5% of employees aged 18+ in the Wholesale, Retail, Repair of Vehicles industry[21] earned less than the real Living Wage (£9.00), compared with 16.9% of all employees in Scotland.[22] This means that changes in this sector can have a material impact on people who work in retail. Further to this, median wages in the retail sector are well below the average wage in Scotland.

The 2020 report from the Fair Work Convention identified retail as one of the sectors not performing well across multiple dimensions of Fair Work[23] such as employee pay as demonstrated in the chart above. International evidence shows that implementing fair work practices leads to improved outcomes, such as improved mental wellbeing, reduced in-work poverty, increased real wage growth, and increased productivity.[24] This is backed by recent analysis that found that higher employee wellbeing is associated with higher productivity and firm performance, including customer loyalty, profitability and staff turnover.[25]

Research carried out by the Joseph Rowntree Foundation[26] (JRF) found that in order to drive productivity and higher rates of pay, strategies for low-wage sectors such as retail should focus on:

- increasing the proportion of workers in on-the-job training

- improving management practices

- increasing the percentage of workers using ICT

- reducing the share of temporary workers

However, in practice these solutions could be challenging to deliver. Investment in training, development of management skills, or action taken to improve or adopt digital skills/technology can be expensive in the short term. Against the context of a difficult period for businesses during the pandemic, cash reserves could be depleted and firms could be increasingly risk-averse. As of the most recent wave of the BICS (24 January to 6 February) 18.6% of businesses in the wider wholesale, retail and repair of vehicles sector[27] who responded had none or less than three months of cash reserves.

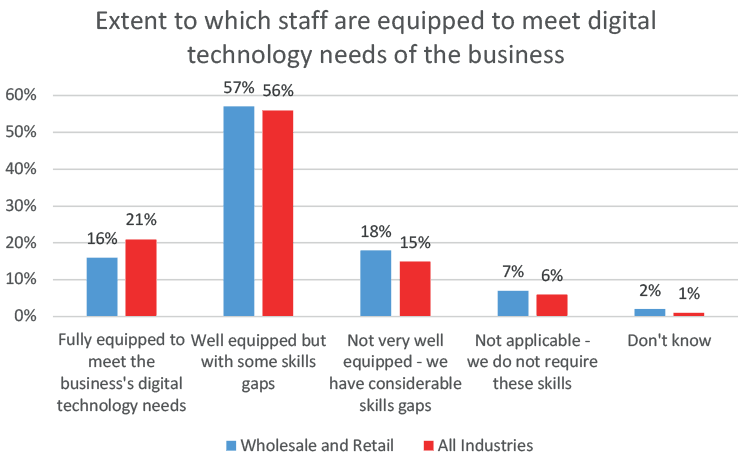

This research also suggests increased use and adoption of technology as a driver of increased productivity. This will be increasingly important given the changing nature of the sector (for example through the rise of e-commerce). The Scottish Government’s recent Digital Economy Business Survey[28] (DEBS) suggests there is scope to improve digital skills in the sector.

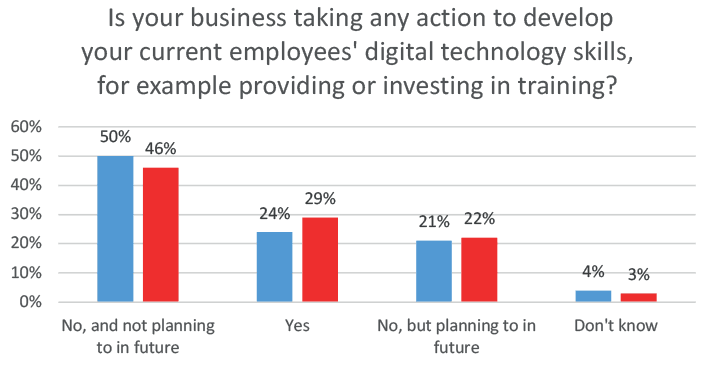

Only 16% of wholesale & retail businesses felt staff were fully equipped to meet the digital technology needs of the business, compared with 21% across all sectors. Meanwhile, 57% of wholesale & retail businesses felt they had some gaps, and 18% felt not well-equipped.

While businesses in the sector identified digital skills gaps, most were not taking any action to address this.

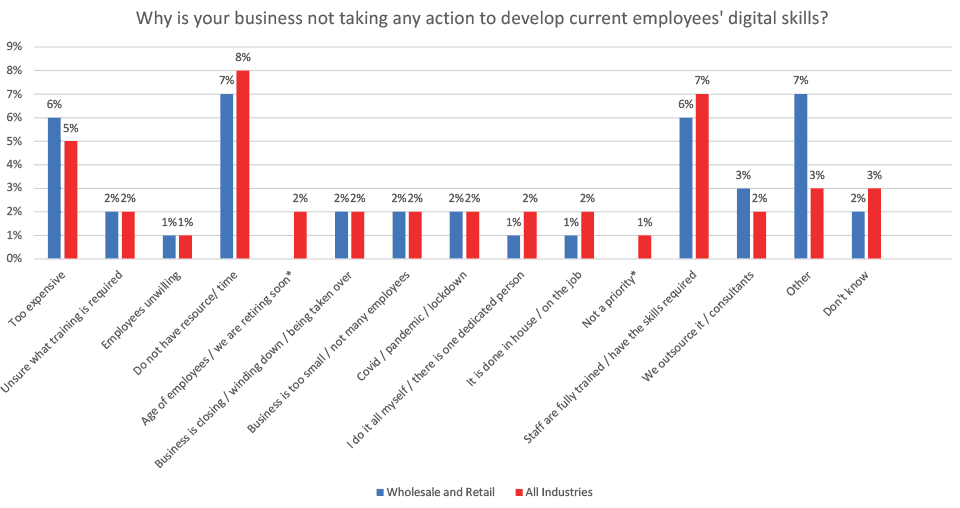

Reasons provided for lack of action to address digital skills gaps were wide-ranging, but most commonly included that it was too expensive (6%), or that businesses cited resource/time constraints (7%).

People

JRF evidence also suggests reducing the share of temporary workers as being a means to drive up productivity and wages in the sector. However, it is important to recognise that temporary employment opportunities offer important flexibility or ‘buffering’ in our economy – absorbing workers between roles, or those in full time education. 28.7% of employees in retail are aged 16-24[29] and for many of these people, retail will be their first employment since leaving school. Furthermore, workers in the sector are more likely to be in full-time education – in the period October 2020 to September 2021, an estimated 10.9% of people aged 16 or more working in the Retail sector were in full time education, compared to 4.2% across all industries in Scotland as a whole.[30]

Retail has been, and remains, a young sector. In 1996 the share of retail’s workforce that was under 30 stood at 40% compared to 28% across the workforce as a whole. That ratio changed little subsequently and in 2018 the ratio was 1.5 (36% vs 24%).

As well as being a younger sector, employees are more likely to be part-time. In 2020, 60% of employees in retail[31] in Scotland worked part-time, and this figure has remained roughly the same over the past three years. Women are more likely than men to work in the retail sector – it was estimated that women made up 60.7% of those in employment aged 16+ in the retail sector in Scotland, up slightly from 60.5% in 2019, The wider retail sector, including Wholesale and Repair of Vehicles,[32] has a higher number of low-skilled workers than most sectors in Scotland, at 12.1% workers with skills level 1.[33]

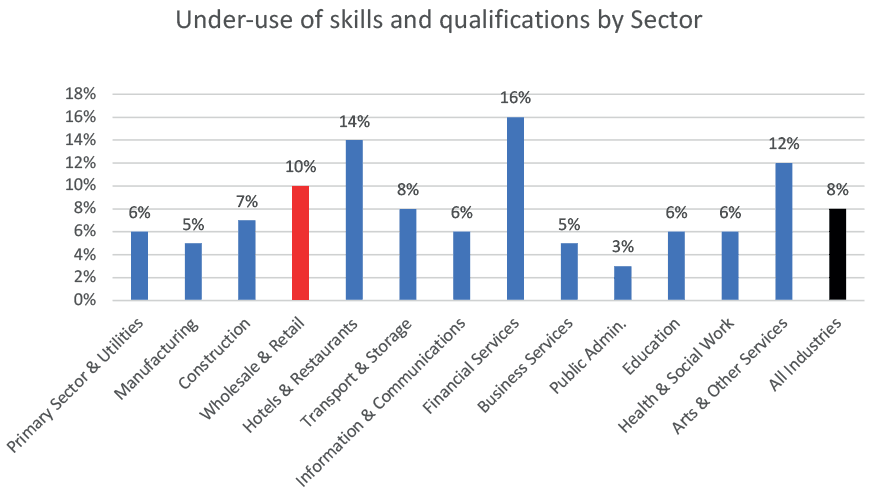

Further to this, under-utilisation of skills and qualifications – where employees that have both qualifications and skills that are more advanced than are required for their current job role – is more common in Wholesale and Retail than across All Industries in Scotland.

Furthermore, historical evidence from the Employer Skills Survey suggests that where staff are working in a role for which they have qualifications and skills more advanced than required, it is more common in the wholesale and retail sector that staff are in the role on a temporary basis, as a stop-gap before starting their desired career.[34]

The retail workforce is constantly changing.[35] Retail has consistently had among the highest employee churn of any industrial sector. In 2018 it had the third-highest rate of new entrants (inflow) and the second-highest rate of employees leaving the sector (outflow). Composite quarterly churn (the sum of inflows and outflows in the quarter as a proportion of total employment) in retail is high at 19%; only the hospitality sector has higher churn (25%). With the outflows there has been a worrying pick-up in retail redundancies and exits to unemployment, relative to trends in other sectors.

So, while evidence suggests reducing the share of temporary workers could be a driver of productivity and higher wages, it is important to recognise that the transient nature of the sector has value. The flexibility of working patterns and potential for short term employment can in some cases mean that the sector plays an important role in accommodating staff with a variety of different circumstances.

Place

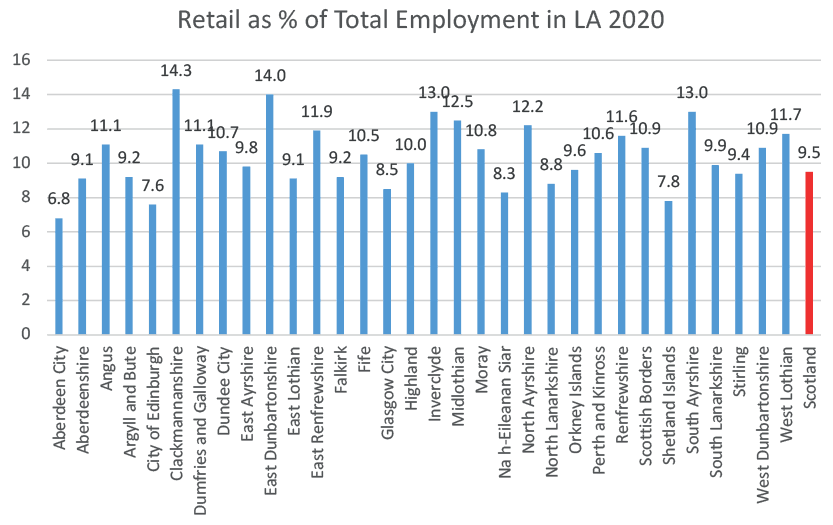

As well as employing a huge number of people across Scotland, the retail sector is a significant employer across every local authority in Scotland.

The Impact of the Pandemic on the Retail Sector

The Covid-19 pandemic that began in early 2020 has had a varied effect on the retail industry. This reflects the effects of the measures taken in response to the pandemic and the subsequent changes in purchasing behaviour.

As a result of these actions impacts differed within the retail sector. While stores deemed non-essential retail (e.g. clothing) were required to close for prolonged periods, retail deemed essential (e.g. food) was able to continue to trade and saw increased sales. Businesses with an established online presence, or were able to rapidly develop one, were able to capture consumer spending that switched online.

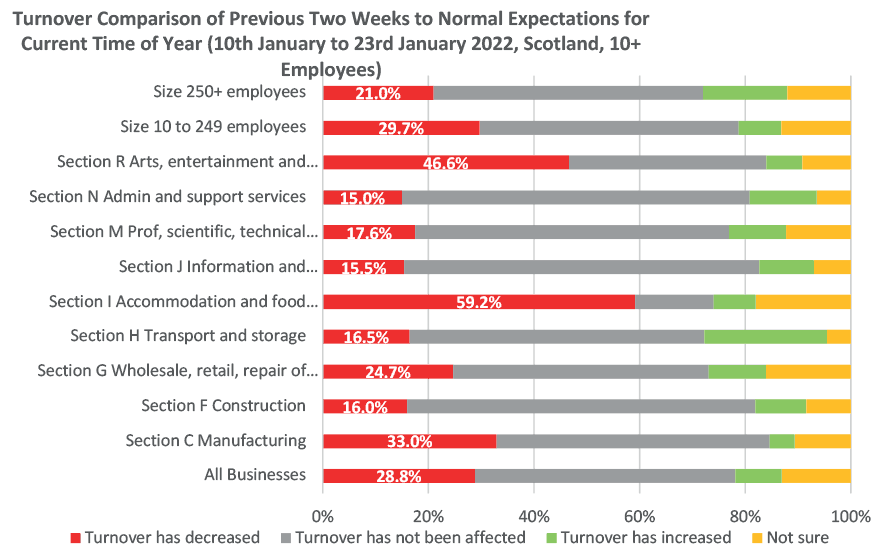

As of the most recent BICS survey data for Scotland (wave 49, 24 January to 6 February) 25.2% of businesses in the wider wholesale, retail and repair of vehicles sector[36] had experienced decreased turnover compared to what would be considered normal for the time of year. 11.6% of businesses in the wider sector reported an increase in turnover, and 50% reported that their turnover had been unaffected.

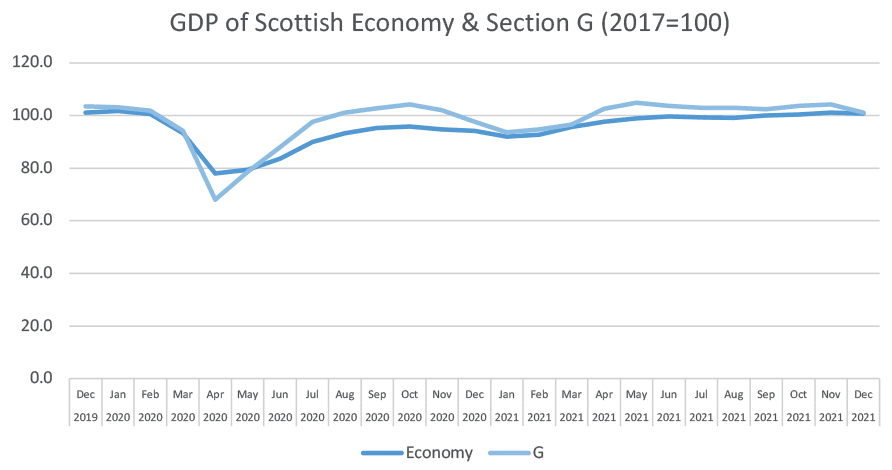

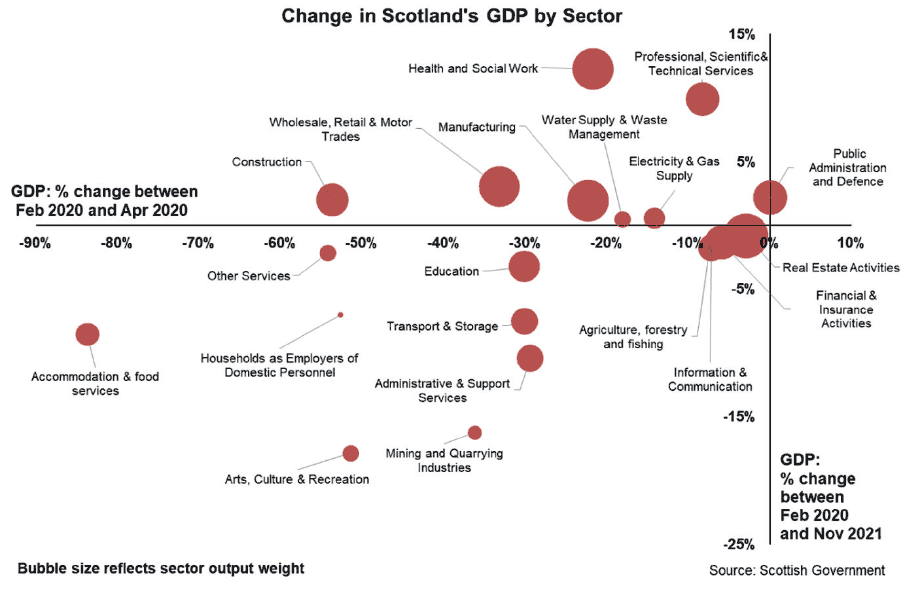

Retail absorbed a larger initial GDP impact from the start of the pandemic than the rest of the Scottish economy, as shown below. However, these figures include food retail (e.g. supermarkets) which evidence suggests were much less affected by Covid restrictions, meaning that the impact on non-food retail will have been even more significant than for the sector as a whole.

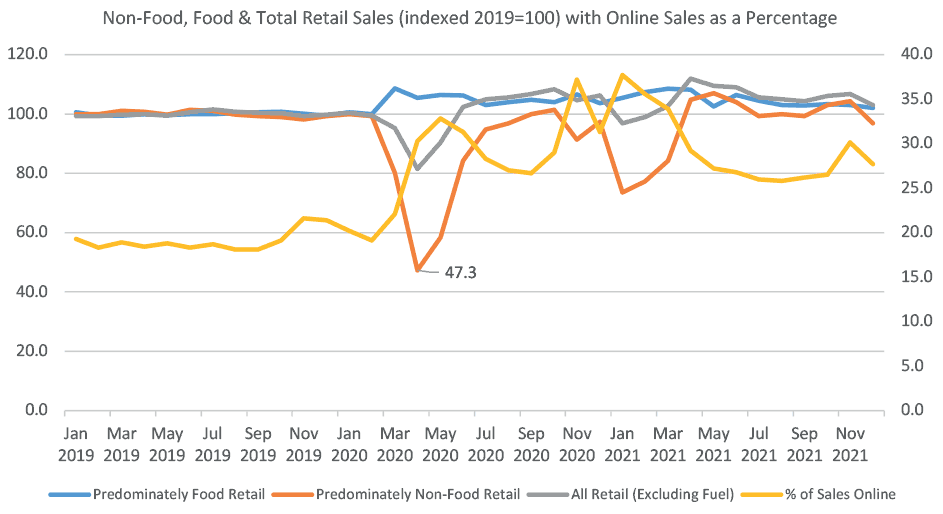

The pandemic had impacts across every sector of Scotland’s economy, including in retail. While food retail (primarily supermarkets) saw an increase in sales from the first lockdown in March 2020, and a spike in sales in each further increase in restrictions – non-food retail experienced significantly reduced sales in each period of tightened restrictions. The proportion of sales carried out online increased significantly in the onset of the pandemic, and remain above pre-pandemic levels.

Spring 2021 saw a re-opening of much of the economy and the total retail volume index moved back above its February 2020 level. By January 2022, retail sales volumes across the UK were 3.6% above their pre-coronavirus (Covid-19) February 2020 levels.[37]

By maintaining its level of sectoral GDP at pre-pandemic levels, Scottish retail has only been outperformed by a few sectors of the economy and this performance exceeds the outcome for the economy as a whole.

The impact of the pandemic continues to be felt across the sector. According to monthly GDP statistics for November 2021, retail GVA is 0.2% lower than November 2020 and 0.1% lower than in October 2021, likely due to the outbreak of the Omicron Covid-19 variant.

Many trends that were evident before the pandemic have accelerated since the onset of Covid-19. For example: online shopping reached record levels during the pandemic (37.7% in January 2021); the increasing role of technology and automation in stores means there are likely to be fewer jobs in future with higher skills requirements; and the need for retail to operate sustainably and contribute to environmental goals must inform economic recovery measures.

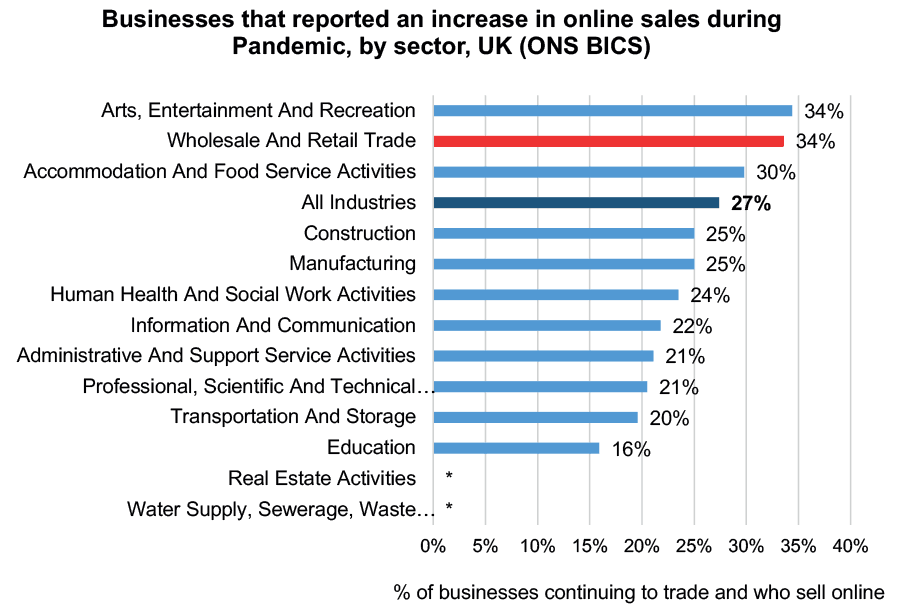

Additionally, many businesses have responded to this increased demand for online shopping by expanding their existing e-commerce capability, or began to sell online for the first time. In the UK, 4% of businesses started selling goods or services online for the first time during the pandemic. The education sector saw the greatest proportion of businesses start to sell online (15%), followed by the Arts, entertainment & recreation (9%), and wholesale and retail trade (8%)[38].

Additionally, 27% of businesses in the UK reported that they have seen an increase in online sales in the two weeks preceding interview (Summer 2020). The arts, entertainment and recreation and wholesale and retail trade sectors experienced the greatest increase in online sales.

Adapting to Changing Consumer Behaviour

Consumer demand and channel choice are key drivers of change in retail. Technological advances mean that the way we buy goods and services is continually shifting as consumers are able to view and purchase through multiple channels (e.g. on apps in addition to websites, via buy now pay later, in checkout-free stores; to name a few).

In 2008, online retail sales began an upward trend in market share, rising to around 5%. By 2019 this share had risen to 19% (£17.3 billion). During the pandemic retail internet sales peaked in January 2021 at 37.6% of total sales (£2.5 billion in that month) while up to and including October 2021 GB internet retail sales accounted for over 29% of retail sales (£22.6 billion).[39]

Over 2019 to 2020, the number of online only retail businesses increased by 67%, while over the entire retail[40] sector, growth was just 2.2%. However, the overall number of strictly online-only retail companies remains around 1% of total retail businesses.

This suggests that entrepreneurs have used the opportunity of online-only retailing to establish businesses that sell exclusively through a web platform, negating the need for physical stores, and presenting a significantly different way in not only how retailers operate but how new businesses are being established in the sector.

Physical shops, high streets and shopping centres have continued to adapt to the rise of internet retailing by offering more experiences and services to customers to compete against online-only retail. Successful physical stores have developed online services that are complimentary to their physical presence. Modifications include offering customers the option to browse goods in the store and then order them online, or pick up goods they have bought online in physical stores.[41]

While the data shows net falls in numbers of physical units in use, recent data continues to show that barbers, beauty salons and nail bars all saw net increases in the number of units in 2019[42], indicative of the type of service that customers value and cannot get from the internet.

Looking Ahead and Opportunities

Retail continues to play a significant part in the Scottish economy and will continue to do so. If it is to flourish in future, meeting consumer needs, the sector will need to continue to adapt to the rapid changes now underway. The physical space now in use is often now just a part of the way that retail sells goods and services to customers. With the rise of e-commerce and home delivery, the skills needed in the sector are changing.

Customers were used to buying goods online pre-pandemic and different delivery pathways had already emerged including, but not limited to, direct delivery to the customer door, click and collect in-store, and pick up from a local drop-off point (such as a convenience store). The most recent model to emerge has been the ‘ten-minute’ delivery of a small range of products from some stores in larger cities.

With much of the service sector working from home for eighteen months their spend online has increased further and become more ingrained into consumer patterns. There also remains much uncertainty around the longer-term trend in relation to working from home or hybrid working seen during the pandemic. This has implications for retailers with outlets in cities as well as for local high streets.

A key concern that is often cited surrounds the impact that aspects of retail – from food production and transportation to so called ‘fast fashion’ – can have on greenhouse gas emissions and climate change. It is therefore important to understand the impact that these sectoral and consumer changes will have on the environment. There are opportunities for retail to show leadership while the growing global demand for more sustainable goods and services.[43] Diversifying products and services, for example repairs, also provides opportunities for retail to develop a distinct in-person offer and higher-skilled jobs.

There is clear evidence that an online presence is an increasingly important part of a successful retail business. With large retail businesses this is often already part of the business model so it is a case of accelerating the process. For other stores it is about developing an online strategy to capture markets outside their immediate locality, including overseas.

With the rise of click-and-collect and direct delivery from warehouse supply chains and logistics, operations will need to adapt and warehouses will need to be able to deal with deliveries to multiple destinations rather than just a few, in addition to dealing with returned goods.

Retailers should use a dynamic approach to ensure that they are primed to tap into rapidly changing and emerging tastes and opportunities. It is therefore critical that people who work in all parts of retail – from the shop floor to the board room – have a comprehensive set of skills to allow them to service new demands. This will involve more training – in skills such as digital, logistics and design, as well as management practices which have been shown to improve business productivity, profitability and survival.[44]

Contact

Email: DEDRetailStrategy@gov.scot

There is a problem

Thanks for your feedback