Fairer Council Tax: consultation analysis

Analysis of responses to the Fairer Council Tax consultation.

Analysis - Question 4: When should any increases be introduced if the tax on higher band properties is increased as proposed?

Quantitative analysis

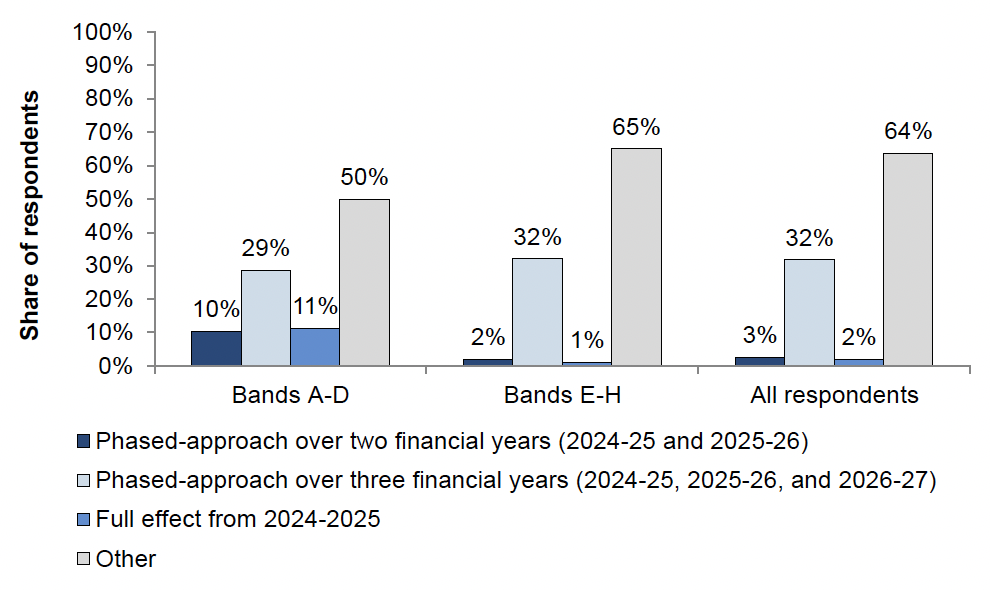

- There were 14,546 responses to this question (1,304 from Bands A-D and 13,242 from Bands E-H).

- Out of all responses, 64% of respondents had other propositions for the timeline of the introduction of the higher tax, 32% supported a phased approach over three financial years, 3% wanted a phased approach over two financial years, and 2% agreed with the increase coming into full effect from 2024-2025.

- 11% of respondents in Bands A-D supported the proposed increase coming into full effect in 2024-25, 10% supported the phased approach over two financial years and 29% supported the phased approach over three financial years. In comparison, 1% of respondents in Bands E-H supported the proposed increase coming into full effect in 2024-25, 2% supported the phased approach over two financial years and 32% supported the phased approach over three financial years.

- 2% of individuals supported the proposed increase coming into full effect in 2024-25, 3% supported the phased approach over two financial years and 31% supported the phased approach over three financial years. In comparison, 13% of organisations supported the proposed increase coming into full effect in 2024-25, 7% supported the phased approach over two financial years and 20% supported the phased approach over three financial years.

- A smaller proportion of respondents in Bands A-D answered “Other” (50%) compared to respondents in Bands E-H (65%). In addition, organisations were less likely to answer “Other” (60%) than individuals (64%).

- Among respondents who opposed a proposed tax increase, 67% answered “Other” and 31% supported a phased approach over three financial years.

- Among respondents who supported a proposed tax increase, 38% supported the proposed increase coming into full effect from 2024-2025, 29% supported a phased approach over two financial years, and 26% supported a phased approach over three financial years.

- Out of 15 councils responding the consultation, 13% (2 councils) agreed with the increase coming into full effect from 2024-2025, 13% (2 councils) wanted a phased approach over two financial years, 7% (1 council) wanted a phased approach over three financial years and 53% (8 councils) responded “Other”. The remaining 13% of councils (2 councils) did not answer the question.

Qualitative analysis

Respondents who selected ‘Other’ were asked to provide reasons for their response. There were 10,700 responses[13] to this question. Around three-quarters of respondents did not directly answer the specific consultation question and instead discussed their general opinion towards the proposed increases. In addition, around 20% of respondents who selected “Phased-approach over two financial years…” or “Phased-approach over three financial years” also expressed their opposition to the proposed Council Tax increase and stated it should not happen at all. Common themes discussed by these respondents included general opposition to any increase in Council Tax (many respondents felt that all three options forced them to “agree” with the increase which they did not), the unfairness of the proposed change and its impact on specific groups, concern around provision of council services and proposed revisions to or replacement of the Council Tax system. This section does not include discussion of these themes, as an in-depth discussion can be found in the analysis to Question 1.

Implementation should be phased over an even longer period

Of the respondents who directly answered the specific consultation question, the majority supported phasing in any proposed increase over as long of a period as possible. Many respondents in this theme mentioned the economic effects of tax increases on households as the main reason behind their view. Those respondents argued that with the current inflation pressures leading to increases in basic expenses such as food and energy bills, a longer implementation period could help ameliorate any negative financial impacts of the tax increase.

“[…] increases must be phased over as long a period as possible. I honestly don’t think the government understands that even with both adults in the house working in ‘decent’ jobs we are struggling with energy bills, food increases and mortgage rate increases [...]” (Individual, Aberdeenshire, no band provided)

Additionally, respondents noted that impacts on household disposable income could be less acute if the increases were spread over a longer period of time.

“Phase in over more years - people may have time to reorder their affairs including moving house to manage and reduce their council tax liability. [...]” (Individual, Highland, Band F)

Finally, some respondents highlighted that many households - such as those whose main income was a pension – were living on fixed incomes, and thus might need more time to make adjustments to be able to pay any increases in Council Tax.

“Many homes in the higher bands will be owned by pensioners who are, consequently, asset-rich, but cash poor. If they have no opportunity to increase their income a sudden increase of these magnitudes could mean they have to sell their home.” (Individual, Midlothian, Band F)

Most respondents who supported phasing over a longer period did not propose a specific timeframe for the increases. Among the small number of respondents who did, the majority suggested a phased rate expansion over a period of 5 years. A smaller number of respondents supported a phased expansion over a period of 10 years.

"The increases should be spread over 5 years pending reforms to bring non-payers into the system. This could be a Council Tax surcharge on properties with three and four or more adults to mirror the discount for single occupant properties or complete abolition, with local authority income coming from a combination of local income tax and local sales tax." (Individual, Fife, Band E)

“[…] the furthest I would be prepared to go is to say that any increases should be very phased over a ten year period, and should only be made in line with any increase in average pay awards and only by that same % amount. To do otherwise is to place an increasing burden of taxation on people, increasing the likelihood of financial hardship and in-work poverty.” (Individual, South Lanarkshire, Band E)

Agreement with phased introduction

For respondents who agreed with one of the proposed phasing options, the most common reason presented (<1% of all respondents) was that an increase over two or three years would allow households to adjust to the new financial circumstances and thus minimise the effects of the tax increase. Among those who specified which of the phased expansion option they preferred, most supported a phased expansion over three years, though respondents generally did not distinguish between a two- or three-year phased introduction (instead expressing their support for a phased over an immediate introduction).

“[…] I think it is critical to give people time to adjust to this new reality should the change come into effect. People may end up selling up and moving to lower Council Tax bands and I do think that is appropriate and normal; people know their own finances. So a phased approach gives time for people to respond.” (Individual, South Ayrshire, Band H)

“While full implementation from 2024/25 would offer most mitigation against reductions in council services, it is acknowledged that there may be practicalities in implementing the changes, which mean that a phased approach over 2 or potentially three years may be the reality. In addition, it is acknowledged a phased approach could help to reduce the financial impact on households.” (Organisation)

“[We believe] that if the proposed increases were to proceed, then they should be phased over 3 years as a minimum. [...] What the consultation is silent on is the fact that budget Council Tax will also be increased by an estimated 3% plus per annum for these three years. [We] would be concerned over the cumulative impact of the proposed increases would have for these households.” (Organisation based in Fife)[14]

“If the increase has to be brought in (rather than looking at a formula based on affordability) then it should be phased in. This would allow people some time to adjust or to downsize.” (Individual, Scottish Borders, Band G)

Agreement with immediate introduction

A small number of respondents supported fully implementing the proposed increase in 2024-25, as they believed this would provide the most benefit to local authorities facing revenue shortfalls due to high inflation rates, loss of EU funding and general cost of living crisis.

“It will make little difference if the policy is phased [instead of] implemented in full. [It] will reduce complexity by introducing [the] measure completely in the first instance. Households in these bands will afford the [Council Tax] increase and [immediate introduction] will ensure that local authorities benefit immediately from the increased revenues as a result.” (Individual, Glasgow City, Band A)

“We believe that these changes are necessary, and overdue, and therefore should be implemented soon to address the historic imbalances in the system. Even with these changes, the annual council tax will still be lower than comparative rates in England and Wales, and in Edinburgh, the maximum increase will only affect 2% of households.” (Organisation based in the City of Edinburgh)

Themes raised by councils

Out of 10 councils which provided reasons for their response, seven agreed with a phased introduction to avoid worsening cost of living pressures (due to current high levels of inflation).

“[…] the first option, ‘full effect from 2024’, may lead to an increase in taxation while inflation remains relatively high, potentially putting a disproportionate pressure on some households’ budget. While a reduction in the rate of inflation does not equate to a fall in prices, phasing the increase in Council Tax rates across the financial years 24/25 and 25/26 would allow for a return to economic stability prior to most of the tax increases, avoiding a situation where a higher council tax rate coincides with a sharp increase in prices, while still providing for an increase in LA finances in a relatively short-term.” (Council)

In addition, one council commented on the time required to update and test the revenue and benefits software used by councils across Scotland to align with the proposed increase.

“As will be the case across Scotland, these proposals would require changes to the Revenues & Benefits ICT System used to administer Council Tax. Changes of this nature usually require a 6 month lead in time by the system’s supplier, to allow the change to be properly developed, tested and implemented with workload balanced across their client councils who will all be competing for the same supplier resource. There are concerns that given the consultation is due to end 20th September, it will take time for regulations to be finalised, and there may be insufficient time to deliver this for 2024/25 Council Tax billing.” (Council)

The remaining three councils responded that the proposed increase should not go ahead (without a full review of the Council Tax system) or that the council did not have sufficient information to provide a response (as it was important to first consider potential unintended consequences such as a decline in collection rates).

“Considering individual proposals to change the Council Tax system in isolation could result in outcomes that are disproportionate and unaffordable for individual households and give rise to unintended consequences without having identified mitigation. For example, there could be a decline in Council Tax collection rates which would impact this important income stream for Councils and therefore Councils’ abilities to deliver local services.” (Council)

Contact

Email: ctconsultation@gov.scot

There is a problem

Thanks for your feedback