Scottish Local Government Finance Statistics (SLGFS) 2020-21

Annual publication providing a comprehensive overview of financial activity of Scottish local authorities in 2020-21 based on authorities' audited accounts.

This document is part of a collection

5. Debt and Prudential Indicators

5.1 Debt

When a local authority borrows money or uses a credit arrangement to finance capital expenditure a debt liability is created that the local authority has to repay from future revenues. A local authority is required to make loans fund advances in respect of capital expenditure it has determined should be met from borrowing. Loans fund advances are repaid in future years.

Table 5.1 provides a summary of local authorities’ debt at 31 March 2021. Total debt across local authorities at 31 March 2021 was £19,723 million, an increase of 1.8 per cent or £345 million, from 31 March 2020.

| Debt Type | General Fund | HRA | Total |

|---|---|---|---|

| Loans Fund Advances outstanding | 11,794 | 4,173 | 15,967 |

| Credit Arrangements | 3,754 | 2 | 3,756 |

| Total Debt | 15,548 | 4,175 | 19,723 |

Source: LFR CR

Total General Fund debt equated to £2,844 per person, an increase of £45 from £2,799 per person at 31 March 2020. Total HRA debt equated to £13,289 per HRA dwelling, an increase of £203 from £13,086 per HRA dwelling at 31 March 2020.

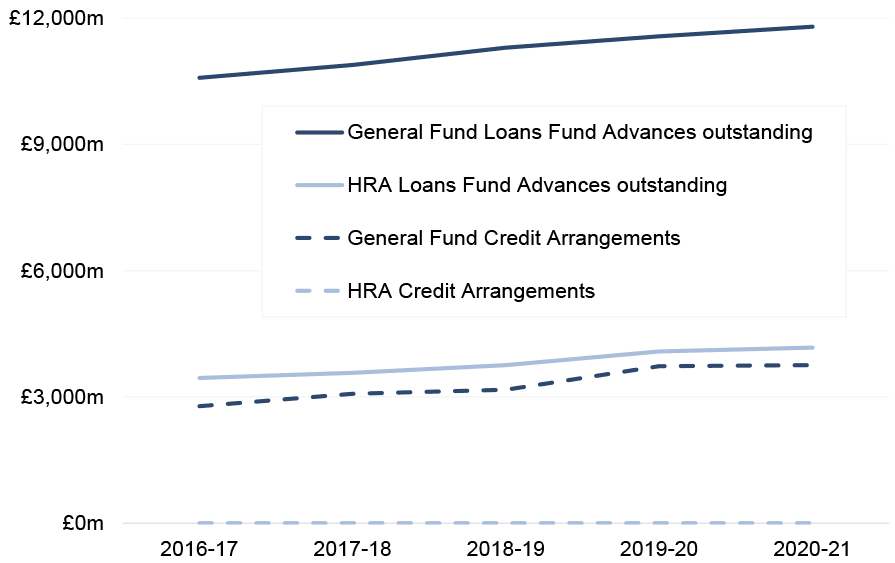

Chart 5.1 shows total debt at 31 March from 2016-17 to 2020-21 by type of debt and split by General Fund and HRA. Total debt has increased by 17.3 per cent, or £2,910 million, over this period. The split of total debt across the four categories shown has remained fairly consistent across this period with General Fund borrowing accounting for around three-fifths of total debt; HRA borrowing accounting for just over one-fifth; and General Fund credit arrangements accounting for just under one-fifth of total debt.

More information on the Loans Fund and credit arrangements, as shown in Table 5.1 and Chart 5.1, are provided in Chapters 5.1.1 and 5.1.2.

Source: LFR CR for 2019-20 and 2020-21, CR Final for all other years

5.1.1 Loans Fund

The Local Authority (Capital Finance and Accounting) (Scotland) Regulations 2016 require a local authority to maintain a Loans Fund. Advances are made from the Loans Fund to record the amount of expenditure a local authority has determined should be met from borrowing, as permitted by legislation. The repayments made to the Loans Fund are the amount to be met in each financial year from a local authorities’ revenue accounts.

The value of a Loans Fund will increase whenever an advance is made for expenditure incurred, or loans made, in any financial year. The value of a Loans Fund will decrease when Loans Fund Advances are repaid by making a charge to the General Fund or HRA. The balance on a Loans Fund at 31 March each year represents the amount of past expenditure a local authority has liability to fund from its future revenue budgets.

A local authority will borrow externally to fund the advances made from the Loans Fund. The balance on the Loans Fund should be similar to the value of external borrowing but there may be legitimate differences between the two values. Local authorities may borrow internally, that is use cash reserves, rather than borrowing externally, or may borrow in advance of incurring the actual expenditure to take advantage of favourable interest rates.

Table 5.2 provides a summary of local authorities’ Loans Funds in 2020-21. The overall value of the Loans Fund across all local authorities at 31 March 2021 was £15,967 million, an increase of 2.0 per cent, or £320 million, from 1 April 2020.

| Movement | General Fund | HRA | Total |

|---|---|---|---|

| Loans Fund Advances outstanding at 1 April | 11,565 | 4,083 | 15,647 |

| Add: New advances from the Loans Fund | 578 | 256 | 834 |

| Less: Repayments made in year | 348 | 166 | 514 |

| Less: Transfer in (+) or out (-) of assets | - | - | - |

| Loans Fund Advances outstanding at 31 March | 11,794 | 4,173 | 15,967 |

Please note that these figures only reflect local authorities own debt and exclude amounts relating to lending to other statutory bodies.

Source: LFR CR

5.1.2 Credit Arrangements

Credit arrangements, such as finance leases, Private Finance Initiatives (PFI) and Public Private Partnerships (PPP) including the Scottish Non Profit Distributing (NPD) model, are not charged to the Loans Fund. However they are a form of borrowing and so are included in the total debt figures.

Table 5.3 provides a summary of local authorities’ credit arrangements in 2020-21. The overall value of credit arrangements outstanding across all local authorities at 31 March 2021 was £3,756 million, a decrease of 0.8 per cent, or £30 million, from 1 April 2020. This decrease reflects that repayments made exceeded the value of new credit arrangements taken up in year.

| Movement | General Fund | HRA | Total |

|---|---|---|---|

| Credit Arrangements brought forward at 1 April | 3,784 | 2 | 3,786 |

| Add: New Credit Arrangements in year | 97 | - | 97 |

| Less: Repayments made in year | 127 | 0 | 127 |

| Credit Arrangements outstanding at 31 March | 3,754 | 2 | 3,756 |

Source: LFR CR

5.2 Prudential Indicators

The Chartered Institute of Public Finance & Accountancy (CIPFA) Prudential Code sets out a framework for a local authority to demonstrate its capital investment plans are affordable, prudent and sustainable. A number of prudential indicators are set and monitored against three year capital expenditure plans. Further, the Local Government in Scotland Act 2003 places a local authority under a statutory duty to set their own maximum capital expenditure limits and they must be set with regard to the Prudential Code. The key prudential indicators are:

- Capital Financing Requirement

- Total External Debt

- Operational Boundary

- Authorised Limit

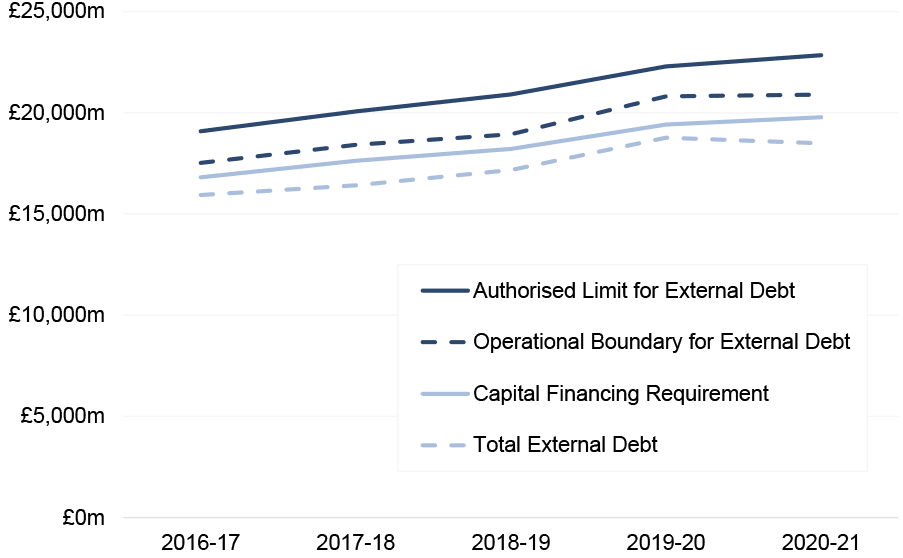

Chart 5.2 shows the change in prudential indicators between 2016-17 and 2020-21. All four indicators have increased at similar rates over this period. More information on the individual indicators is provided in the remainder of this chapter.

Please note that the treatment of loans to other statutory bodies in the CFR and Total External Debt figures may vary between local authorities for years prior to 2020-21, however this relates to comparatively small values and so is not material.

Source: LFR CR for 2019-20 and 2020-21, CR Final for all other years

5.2.1 Capital Financing Requirement (CFR)

The Capital Financing Requirement (CFR) represents the amount of capital expenditure a local authority has determined should be met from borrowing or funded from a credit arrangement, with the repayment of the debt met from future local authority budgets.

The CFR will increase each year by the amount of new capital expenditure to be financed by borrowing or credit arrangements, and will decrease by the amounts repaid. The CFR represents an authority’s underlying need to borrow money.

Table 5.4 shows the CFR calculation for 2020-21. The CFR increased from £19,485 million at 1 April 2020 to £19,775 million at 31 March 2021. This means that local authorities had a higher amount of new capital expenditure to be financed by borrowing than amounts repaid in 2020-21. This increase in CFR was reflected across both the General Fund and HRA.

| Movement | General Fund | HRA | Total |

|---|---|---|---|

| Capital Financing Requirement at 1 April | 15,304 | 4,181 | 19,485 |

| Add: Capital exp. financed by borrowing | 578 | 256 | 834 |

| Add: Capital exp. financed by credit arrangements | 97 | - | 97 |

| Less: Loans Fund repayments | 348 | 166 | 514 |

| Less: Credit Arrangements repayments | 127 | 0 | 127 |

| Capital Financing Requirement at 31 March | 15,503 | 4,272 | 19,775 |

Please note that these figures exclude amounts relating to lending to other statutory bodies.

Source: LFR CR

Chart 5.2 shows that local authorities’ CFR has increased over the last five years which reflects the increase in local authority borrowing over this period.

5.2.2 Total External Debt

Total External Debt reflects local authorities’ gross external borrowing and other long term liabilities. This may be less than the CFR where an authority has chosen to utilise cash reserves rather than borrow externally. Total External Debt may be more than the CFR where a local authority has chosen to borrow in advance of actual capital expenditure; however the Prudential Code limits borrowing in advance to the CFR amount plus up to two years planned capital expenditure to be funded from borrowing.

Table 5.5 shows that total external debt at 31 March 2021 was £18,487 million. Around four-fifths (79.7 per cent) of total external debt related to external borrowing, with the remainder relating to credit arrangements outstanding.

| External Debt Type | Total |

|---|---|

| Actual external borrowing | 14,731 |

| Credit arrangements outstanding | 3,756 |

| Total External Debt | 18,487 |

Please note that these figures reflect actual gross external debt as calculated for comparison to the Capital Financing Requirement as per the Prudential Code.

Source: LFR CR

As shown in Chart 5.2, the CFR continues to remain above total external debt. This means that local authorities continue to be under-borrowed, that is they are utilising internal cash reserves rather than borrowing externally. At 31 March 2021, total external debt was 93.5 per cent of the CFR, which is in line with prior years.

5.2.3 Operational Boundary and Authorised Limit

The Operational Boundary is based on local authorities’ capital spending plans and should reflect the most likely, or prudent, but not worst case scenario for borrowing. In general, it is not significant if an authority breaches the operational boundary for a short period, however a sustained or regular trend above would be significant. At 31 March 2021, the Operational Boundary was £20,894 million across local authorities.

The Authorised Limit represents the maximum amount that the authority may borrow and is set at a level that reflects capital expenditure plans but includes headroom to allow for unusual cash movements, i.e. treasury management. The Authorised Limit across all local authorities was £22,850 million at 31 March 2021.

As shown in Chart 5.2, neither the operational boundary nor the authorised limit have been breached in the last five years. This means that local authorities’ borrowing has consistently remained below these limits.

Contact

Email: lgfstats@gov.scot

There is a problem

Thanks for your feedback