Scotland's Marine Atlas: Information for The National Marine Plan

Scotland's Marine Atlas is an assessment of the condition of Scotland's seas, based on scientific evidence from data and analysis and supported by expert judgement.

MARITIME TRANSPORT (PORTS AND SHIPPING)

What, why and where?

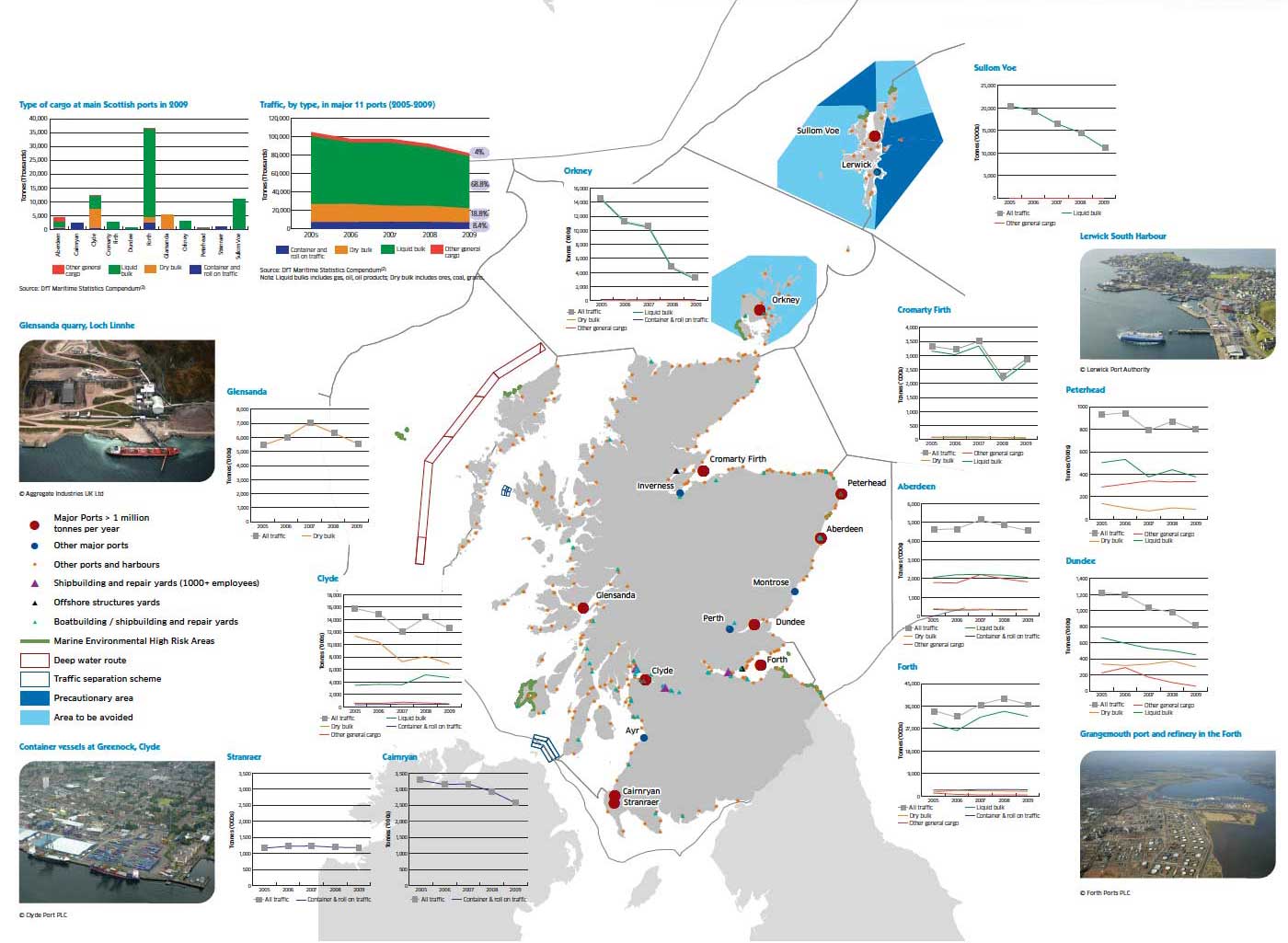

Ports and shipping provide for the transport of freight and passengers. This includes key international and coastal shipping routes including ferry services to the Scottish islands. A few ports specialise in specific cargos, for example, Sullom Voe for oil, and Glensanda for crushed stone. The majority are multi-purpose even if they are well known for one particular commodity, such as Peterhead for fish. Other ports may play an important role for a particular industry such as Aberdeen in supporting North Sea oil and now for the developing offshore renewable energy industry.

Cargo and passenger port traffic figures are published each year in Scottish Transport Statistics (1) and Department for Transport Maritime Statistics Compendium (2). In 2009, 85.5Mt of cargo was handled through all Scottish ports, being reductions of 11.2% since 2008 and 21.4% since 2005. 98.4% of this was handled by the 16 major ports (96.0% by the top 11), with the Forth ports accounting for 43.6%.

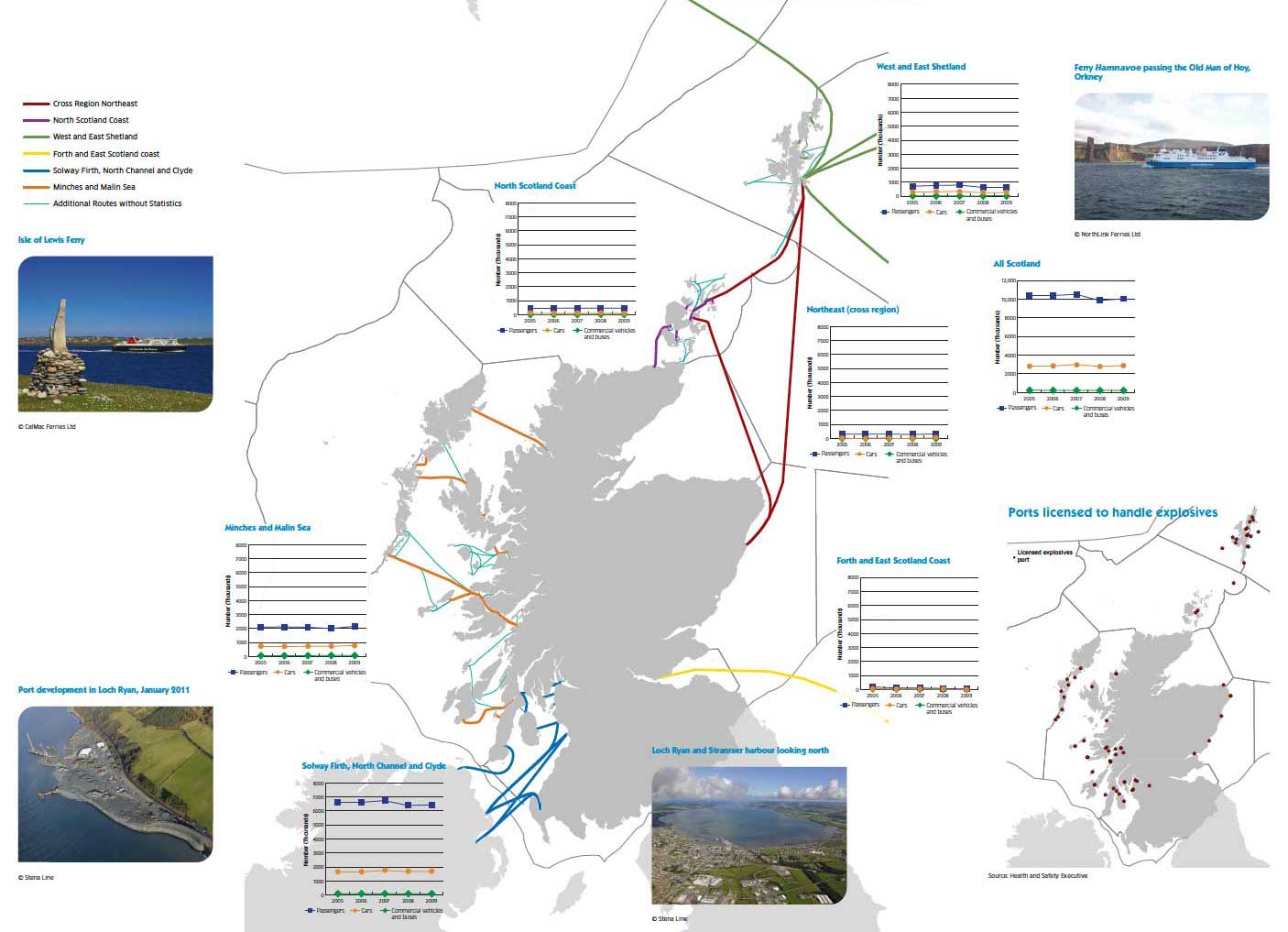

In 2009, 10,048,738 passengers were carried on ferries (3.2% down since 2005), with 2,873,611 cars (1.5% up) and 213,936 commercial vehicles and buses (11.8% down) (1). The busiest sea areas were Clyde and Solway Firth/North Channel (passengers 64% of overall traffic in Scotland, cars 59% and commercial vehicles 39%) followed by the Minches and Malin Sea (22%, 28% and 35%).

The movement of vessels is recorded by the Maritime and Coastguard Agency, Lloyds List Intelligence and others, such as individual ports. Data sets are not always comparable, with a different range of categories being used and certain types of ports or vessels, for example, fishing, recreational, local ferries, not featuring in all types of statistics.

Lloyds' data show that in 2009, there were 15,225 vessel arrivals at the main Scottish ports (excluding Cairnryan, Stranraer and Glensanda), a 3.9% fall since 2005. 82.2% of these were at 3 ports: Aberdeen (45.8%: 1.0% up since 2005), Forth ports (19.3%: 27.6% fall) and Lerwick (17.1%: 52.6% up). The 15,225 vessels represented 128.3Mt of shipping deadweight tonnage (13.6% fall since 2005) with the Forth ports (38.7%: 1.5% fall) and Aberdeen (17.7%:8.5% up) positions reversed due to the different nature of shipping: fewer but much larger vessels in the Forth.

Scotland has three major ship building yards: BAE Systems Surface Ships (Scotstoun/Govan), Babcock Marine Warships (Rosyth), Babcock Marine Clyde (Helensburgh) and a range of smaller yards.

Types and examples of Scottish ports

Source: Marine Scotland (table excludes many small slipways, jetties and harbours).

Note: (i) top 16 ports in Scottish Transport Statistics; top 11 are defined as regularly handling over 1Mt per year.

Ship-to-ship oil transfer operations 2005-2009

Number of transfer operations |

Oil tonnage |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Port and Scottish sea area |

2005 |

2006 |

2007 |

2008 |

2009 |

2005 |

2006 |

2007 |

2008 |

2009 |

Scapa Flow (north Scotland coast) |

17 |

8 |

7 |

10 |

27 |

1,746,715 |

993,75 |

9930,136 |

582,097 |

2,599,461 |

Sullom Voe (west Shetland) |

3 |

1 |

0 |

1 |

5 |

284,702 |

137,948 |

0 |

59,394 |

298,395 |

Nigg (Moray Firth) |

14 |

11 |

16 |

12 |

14 |

1,201,467 |

853,431 |

1,246,146 |

970,459 |

1,015,832 |

Total |

34 |

20 |

23 |

23 |

46 |

3,232,884 |

1,985,138 |

2,176,282 |

1,611,950 |

3,913,688 |

Note - Scapa Flow hosted one LNG transfer of 56,827 tonnes in 2007.

Source: Marine Scotland

Contribution to the economy

All Scotland's ports contribute to their local and regional economies as employers and by providing essential facilities for users such as the fishing industry and ferry operators. In many cases they also contribute to the national economy and economic growth.

From the ABI the GVA (2009 prices) and number of jobs for sea and coastal water transport and supporting activities was £432M and 4,700, and for building and repairing of ships and boats the equivalent GVA was £475M, with the number of jobs at 5,800, all in 2007. These values cannot be disaggregated to individual sea areas.

There are other sources of economic data. Oxford Economics reports for the Chamber of Shipping (3) have estimated that from a turnover of £9.5 billion the shipping industry contributes about £4.7bn GVA to the UK. A further report for the UK Major Ports Group (4) suggests that ports contribute around £7.7bn to UKGDP. Neither report presents a breakdown for Scottish shipping or ports. However, Scottish ports handle about 17% of UK trade by volume.

It was estimated (in 2006) that port activities account for around 18,000 jobs in Scotland (5).

Foreign (imports and exports) and domestic traffic (million tonnes) through major Scottish ports 1998-2009

Source Scottish Transport Statistics (1)

Note: Largest % of exports to Netherlands, USA, Germany, France.

Imports from Norway, Russia.

Shipbuilding

Hull sections of two new aircraft carriers are currently being constructed at five UK sites (including the Clyde and at Rosyth). All vessels will be assembled at Rosyth. All six Daring class Type 45 destroyers are being built on the Clyde (some parts come from outside Scotland).

Source: Scottish Enterprise

International and domestic ferry routes

Pressures and impacts on Scotland's socio-economics

Positive

- Relative environmental benefits of moving goods by sea compared with other forms of transport

- Employment (direct and indirect)

- Providing skilled people for shore-based jobs, shipbuilding and repair

- Wider, societal benefits by enabling the movement of people, goods and services to and from island communities and providing access to education, healthcare and social activities

- Provision of infrastructure for offshore industries

Negative

- Ports use large areas of coastal land and often require hard coastal defences

- There is often competition for sea space e.g. coastal water shipping lanes near ports, where ships are restricted in their ability to move

Source: Based on CP2 PSEG Feeder Report section 3.7.6 (6) and UK Marine Policy Statement (7)

Ship-to-ship oil transfer at Sullom Voe

|

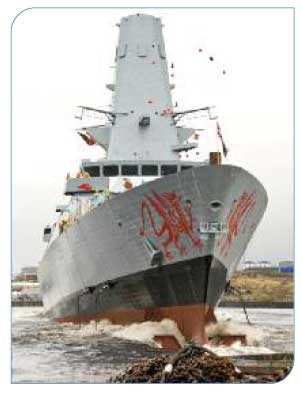

HMSDragon launch on the Clyde

|

Peterhead

|

Invergordon

|

Greenhead base at Lerwick

|

Pressures and impacts on theenvironment

Pressure theme: Pollution and other chemical pressures

Pressure: Release of antifouling substances

Impact: Result in contamination of water and sediments and biological impacts on biota.

Pressure: Introduction of non-synthetic substances and compounds

Impact: Accidental release of oil and other hazardous substances, (either cargo or fuel, discharges from port facilities and shipbuilding/ ship repair yards) may result in contamination of water and sediments and ecological impacts on wildlife, mariculture and tourism (see Chapter 3).

Pressure theme: Other physical pressures

Pressure: Noise Impacts

Impact: Noise from, for example, construction, ship movements, other operations.

Pressure: Noise from dredging

Impact: Potential impacts on noise sensitive species, such as cetaceans and some fish species.

Pressure: Noise impacts

Impact: Noise from construction, ship movements can cause disturbance of behaviour, damage to hearing, worst-case fatality.

Pressure: Litter

Impact: Litter poses a risk of harm/death to marine wildlife through ingestion of, or entanglement.

Pressure: Death or injury by collision

Impact: May kill or injure individuals e.g. cetaceans.

Pressure theme: Habitat changes

Pressure: Smothering by sediment plume

Impact: Results in habitat change and loss. May reduce water quality.

Pressure: Habitat damage, loss and/or abrasion

Impact: Infrastructure, e.g. ports, replaces natural coastline with man-made structures. Navigational dredging can damage marine benthic habitats. Vessel wash can damage habitats.

Pressure: Abrasion from passage of dredge head

Impact: Habitat change and damage.

Pressure: Removal of substratum

Impact: Changes to sediment characteristics. Significance depends upon habitat sensitivity, recovery rates and magnitude of impact.

Pressure: Disturbance of seabed

Impact: Can reduce sediment and water quality and change benthic fauna.

Pressure theme: Biological pressures

Pressure: Introduction or spread of non-native species

Impact: Non-native species may be carried in ballast water and as fouling organisms on hulls. These may cause habitat modification and competition with native species.

Pressure: Microbial pathogens

Impact: Release of sewage introduces pathogens and nutrients into the water, affecting water quality and potentially passing on diseases to humans through contact with contaminated water or consumption of contaminated shellfish.

Source: Based on CP2 PSEG Feeder Report tables 3.53 and 60 (6) and UK Marine Policy Statement (7)

There are environmental benefits. Transport by water is a key part of the transport infrastructure, providing economies of scale and produces less CO 2 than comparable modes of transport per tonne-kilometre/ per passenger-kilometre. Navigational dredging can provide material for beach replenishment schemes. Artificial shoreline infrastructure may provide habitat for colonisation.

Traffic through Pentland Firth (2009)

Type of traffic |

Dead Weight Tonnes |

Dead weight %of all traffic |

No. of vessels passing |

No. of vessels passing % of alltraffic |

Average deadweight per vessel |

|---|---|---|---|---|---|

All traffic |

275,564,241 |

100% |

7,955 |

100% |

34,640 |

Traffic not stopping in UK |

144,721,925 |

53% |

3,888 |

49% |

37,222 |

Traffic stopping at a UK port |

130,842,316 |

47% |

4,067 |

51% |

32,171 |

Traffic starting or finishing at a Scottish port |

74,520,400 |

27% |

2,019 |

25% |

36,909 |

Traffic starting and finishing at a Scottish port (domestic traffic) |

8,300,648 |

3% |

598 |

8% |

13,880 |

Source: Lloyds List Intelligence

Monthly vessel traffic through the Minches in 2009

J |

F |

M |

A |

M |

J |

J |

A |

S |

O |

N |

D |

Total % over year |

Number of vessels |

|

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Northbound (%) |

52.1 |

59.3 |

50.0 |

54.8 |

52.7 |

50.5 |

54.8 |

55.0 |

54.9 |

55.9 |

50.8 |

49.1 |

53.4% |

1,238 |

Southbound (%) |

47.9 |

40.7 |

50.0 |

45.2 |

47.3 |

49.5 |

45.2 |

45.0 |

45.1 |

44.1 |

49.2 |

50.9 |

46.6% |

1,082 |

% per month |

7.0 |

7.6 |

8.7 |

9.1 |

9.5 |

8.4 |

8.6 |

8.1 |

8.9 |

8.8 |

8.0 |

7.4 |

100.0% |

2,320 |

Source: MCA, Stornoway Maritime Rescue and Co-ordination Centre - excludes local ferry traffic and fishing vessels

Traffic through the Minches by type of vessel (2009)

|

Ullapool

|

All traffic for 11 major ports (2005-2009)

Source: DfT Maritime Statistics Compendum (2) |

|

Pentland Firth and the Minchestraffic

Shipping traffic through the Pentland Firth and the Minches is of particular interest since much of this does not stop at Scottish ports. However, not all traffic, for example fishing vessels and recreational craft, are counted.

Forward look

The Scottish Government has devolved responsibilities for ports, and has developed its own ports policy under the Scottish National Transport Strategy. (8) The sector is important to the economy and for economic growth. There are no robust data available on any future expansion, ports' policy follows a market driven approach to port development. 95% of goods moving in and out of the UK go by sea and there is little scope to use alternative means to do this. New ship technology and larger ships will tend to lower the costs per tonne-kilometre but may require ports with new or improved access to deeper water.

Forecasts for the UK have led the Department for Transport to conclude in its draft National Policy Statement for Ports covering England and Wales, that 'there is a compelling need for substantial additional port capacity over the next 20-30 years, to be met by a combination of development already consented, and development for which applications have yet to be received'. (9) There are substantial opportunities for some of this additional capacity to be met in Scotland. The Scottish Government's Second National Planning Framework ( NPF2) (10) identifies development opportunities to accommodate container traffic along the Firth of Forth, Scapa Flow and Hunterston. It also supports improvements to facilities for ferry services at Loch Ryan. Existing and potential facilities at Cromarty Firth and Nigg Fabrication Yard are identified within the Framework as being of strategic importance.

Ports and shipping will continue to play an important role in the movement of goods and people. As well as the environmental benefits of this, for example contributing towards climate change targets, the industry will have a significant role to play in making the most of opportunities offered by offshore renewable energy.

The importance of ports to provide infrastructure that can be adapted to meet the needs of the emerging offshore renewable energy industry is highlighted in the National Renewables Infrastructure Plan (N- RIP). (11) Gathering data on shipping movements and densities is needed for marine planning and offshore renewable energy deployments.

The Scottish Government is undertaking a comprehensive review of ferry provision throughout Scotland. The Review is considering how ferries should be funded and procured, on what basis fares should be set, what kind of services should be supported with public money and who should be responsible for providing these services. The Ferries Review will result in a long-term Plan for ferry services to 2022.

Scotland's ports, cargo tonnages (2005-2009) and identified navigation areas

Shipping traffic: number of vessels in a given area during 1st week January 2010 based on Maritime and Coastguard Agency AIS data